Copper Rallies Again, India’s Rate Cuts, Secondary US Employment Data, Oklo Up

Morning Macro 5th December

Copper rallies another +2.3% to new all-time highs as the markets new favourite trade. Silver and Japanese yields continue trending higher too. Global yields starting to grind higher too with the U.S. 2s/10s curve steepening to 58bp. While the dollar finally has a positive day after its 9-day decline – matching the longest slide in 30 years.

US PLANS MORE STAKES IN MINERALS COMPANIES, TRUMP OFFICIAL SAYS

First Google, now Amazon – *AMAZON SAYS NEW CHIPS ARE MORE COST EFFECTIVE THAN NVIDIA’S

UK NOV. CONSTRUCTION PMI FALLS TO 39.4; FORECAST 44.6

India cuts rates to 5.25% as expected as central bank flags ‘weakness in some key economic indicators.

Mixed signals from secondary U.S. employment data:

- U.S. small businesses shed 120,000 jobs in November, the steepest decline since May 2020, per ADP.

- US Layoffs are running at crisis pace. U.S. companies announced 153,074 job cuts in October, nearly TRIPLING from 2024. It was the WORST October in 22 years. YTD, layoffs have reached 1,099,500, up +65% YoY, nearing GREAT FINANCIAL CRISIS levels

- Jobless claims fall to 191k, estimated 220k, much stronger than expected.

- U.S. temporary hiring has re-accelerated, perhaps an early signal we may be coming out of the slowdown. (Chart 1, Steno Research, Macrobond, Bloomberg)

Russell 2000 Index +15% ytd, Profitable Russell: +9.7%, Unprofitable Russell: +45% ….hhmmm!

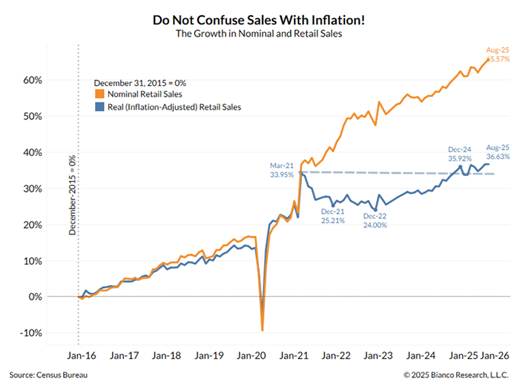

Pay more, get less: “US sales on Black Friday hit $18 billion, up 3% compared with a year earlier…. But US shoppers purchased 2% fewer items at checkout, and with average prices up 7%, shoppers made 1% fewer online orders.” (Chart 2, Census Bureau, Bianco Research)

ANTHROPIC’S CEO WARNS THAT SOME AI GIANTS ARE TAKING RECKLESS, HUNDREDS-OF-BILLIONS SPENDING RISKS ON DATA CENTERS AND CHIPS, SAYING THE INDUSTRY IS GAMBLING ON UNCERTAIN ECONOMIC PAYOFFS.

Oklo, is now up +24% this week after Jensen Huang said the future of AI will be powered by “small nuclear reactors.”

Data today – US PCE deflator (inflation), UniMich consumer confidence

Copper Makes New All-Time High, Job Losses, ISM Services PMI Rises, Australian OIS

Morning Macro 4th December

Copper makes another new all-time high as the dollar trends lower (unable to break the magic 100 level Chart 1, Bloomberg) on news ultra dove, Trump puppet Hassett is the likely new Fed chair and ADP payrolls come in significantly weaker than expected. In Japan 10-year JGB’s rise another 4bp, highest since 2008.

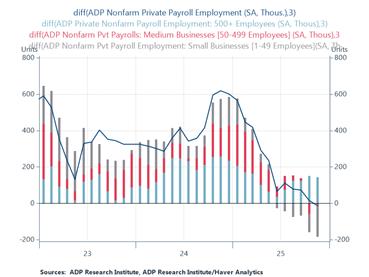

The ADP report for November shows the largest monthly job losses (32,000) since early 2023, undershooting the consensus forecast gain of +10,000 jobs. Notable distribution: Small firms are the ones shedding workers, according to the latest ADP. Over the last three months, small businesses have cut 178,000 off their payroll ranks. By contrast, large firms have added 143,000. (Chart 2, @RenMacLLC)

The ISM Services PMI rose 0.2 points to 52.6, beating expectations by 0.5 points and marking the ninth consecutive month of sector expansion in 2025. The index now sits 0.9 points above its 12-month average of 51.7, indicating steady, modest growth. Business Activity (54.5%) and New Orders (52.9%) remained firmly in expansion territory, while Employment (48.9%) continued to contract for a sixth straight month. The Prices Index eased to 65.4%, down 4.6 points from October, signalling ongoing but moderating inflationary pressure.

TRUMP: “I guess a potential Fed Chair is here too…I don’t know, are we allowed to say that? Thank you, Kevin.” Kevin Hassett has consistently called for lower interest rates to stimulate economic growth and criticized the Federal Reserve for being too slow to ease monetary policy.

The S&P 500’s 5-day historical range is now 1.2%, the lowest level of the year. Markets are quiet after Thanksgiving but plenty of event risk ahead with Fed, BOE and BOJ rate meetings all pricing moves (cut, cut, hike) plus a resumption of key US payroll data, and the expected Santa Claus rally. All in low volume.

$IBM CEO says that at today’s costs it takes about $80B to build & fill a 1 GW AI data centre, so the ~100 GW of announced capacity implies roughly $8T of capex & “no way you’re going to get a return on that,” since you’d need “about $800B of profit just to pay for the interest” (Charles-Henry Monchau)

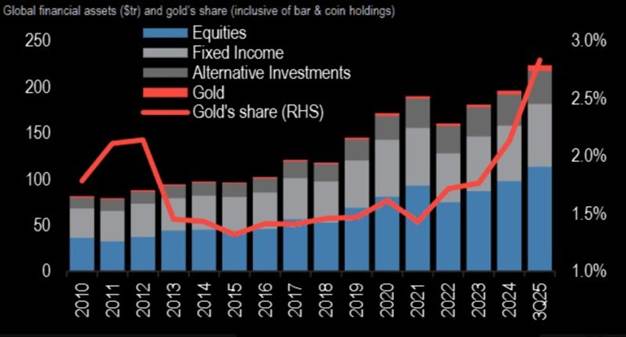

Gold is a mere 2.8% of investors AUM (Chart 3, The Market Ear, Charles-Henry Manchau)

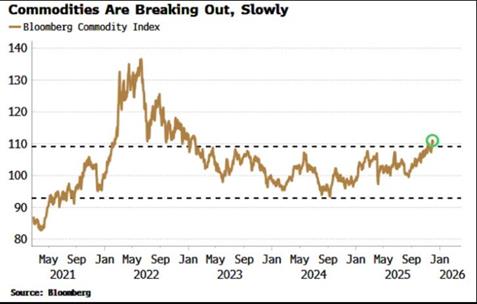

Commodities are breaking out slowly (Chart 4, Bloomberg)

The Australian OIS is pricing one full HIKE over the next 12 months. AUDUSD up 2.5% over the last 2 weeks.

Here’s the cumulative real GDP growth for Europe’s four biggest economies since Q1 2020: 9%, 7.5%, 6.2%, 2.1%…. trending!

Another shocking stat of the day: Interest costs on US debt are now equal to 24% of every $1 in government tax revenue. The interest expense as % of collected taxes has nearly DOUBLED over the last 4 years.

Data today – EZ retail sales, US weekly jobless claims

Copper & Silver Trend Higher, US Yield Curve Steepens, Bitcoin Falls, US Foreclosures Up 20%

Morning Macro 3rd December

Copper & Silver continue their trend higher, making new all-time closing highs, While UK 2-year yields break support and close in on new cycle lows based on concerns around the economy, with the OIS pricing 65bp cuts over the next 12 months.

While silver surged, gold pulled back on news of Russian central bank selling, its reserves falling 57%, a clear sign of financial stress within the economy due to the war. Meanwhile …. PUTIN: IF EUROPE WANTS TO FIGHT WAR, WE ARE READY NOW

The US yield curve is starting to steepen, 2’s/10’s now at 57bp, no doubt being led by the huge move in Japanese long end yields, with the Japanese 30-year grinding up another 3bp today.

Bitcoin fell 4.5% on Monday and has since rallied 7.8%. Anyone who trades this is braver than me, I don’t see any clear fundamentals and price action is clearly manipulated by the whales. Good luck!

Manufacturing PMI’s (Purchasing Managers Index) continue to show contraction, with the U.S. falling the most in 4 months to 48.2 (last 48.7) with employment a woeful 44 and new orders 47.4. (Chart 1, Bloomberg)

U.S. foreclosures have risen 20% as more homeowners fall behind on their mortgage payments, according to ATTOM.

TRUMP: WE ARE GOING TO GIVE REFUNDS OUT OF THE TARIFFS. I BELIEVE IN THE NEAR FUTURE YOU WON’T HAVE INCOME TAX TO PAY. (Chart 2, Eliant Capital)

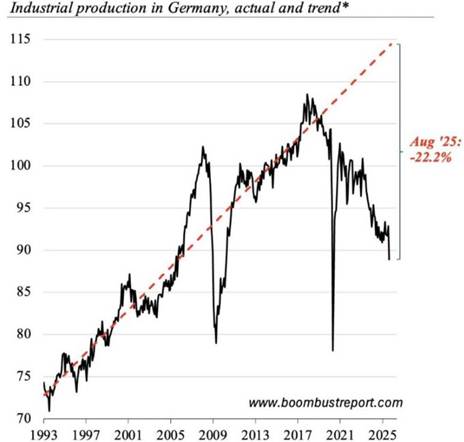

Germany, what went wrong? The Left and the Green party. Industrial production collapses. (Chart 3, TheBoomBustReport)

Switzerland November CPI 0.0% vs +0.1% y/y expected

Data today – Global services PMIs, US ADP employment

Sell-off in Treasuries, JGB 10-yr Auction, US Manufacturing, Precious Metals Pull Back

Morning Macro 2nd December

Post-Thanksgiving trading saw selloff in Treasuries, with long end up most. 10-year yield rose to 4.1% this morning, up from 3.99% at the close before the holiday. Japanese bonds are also continuing to sell off, as 10-year yield hit its highest since 2008.

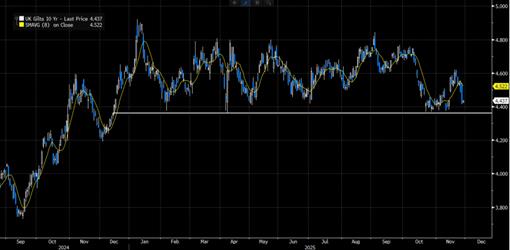

Today’s JGB 10-year auction brought some relief to the market after jitters regarding Japan mounting debt concerns. The auction saw a bid-to-cover ratio of 3.59, higher than the previous offering in November, as elevated yields lured buyers despite rising expectations for a near-term BOJ rate hike. The yield on the 10-year JGB is now trading to its highest in 17 years! USD/JPY and interest rate differentials remain stubbornly deanchored (Figure 1).

In the UK, OBR chair Richard Hughes quit after the “inadvertent” leak of November 26 Budget forecasts. London struck a deal with Washington to keep US pharma tariffs at 0% for three years, though the UK will pay more for medicines via the NHS. Shop-price inflation cooled to 0.6% YoY in November (from 1%) thanks to early Black Friday discounting. Starmer says the UK will be more pro-business toward China but won’t trade security for market access.

Europe remains Ukraine-focused: the EU says Belgium’s concerns over the €140bn Ukraine loan can be managed, while Zelensky reiterated that sovereignty and security guarantees are non-negotiable and territorial concessions off the table. Macron says a peace deal is still “far off”. The EU may also delay its review of the 2035 combustion-engine ban.

US manufacturing is stuck in contraction, with ISM warning trade uncertainty “kills us”, while Washington approved up to $150mn subsidy for chip start-up xLight. Canada is set to join the EU’s €150bn defence procurement fund.

China’s Vanke rattled markets again with fresh debt-delay details, while the PBOC drained CNY145.8bn net via OMO and fixed the yuan at 7.0794. China’s onshore yuan reaches its strongest close since 11 October.

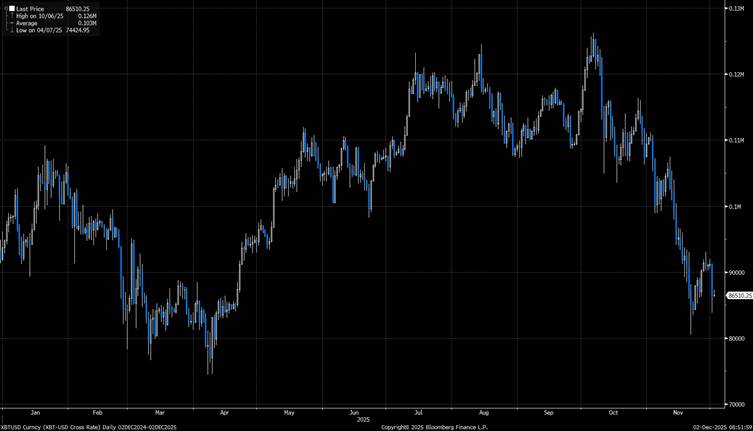

Precious metals pull back from their highs, with silver down 1.5% this morning, now below $58/oz. Gold down less, trading just above $4.2k/oz. Crypto keeps crashing, as Bitcoin dropped to under $84k yesterday (figure 2) and Ethereum is now below $3k. As a whole, the crypto market saw nearly $1bn in leveraged longs liquidated on Monday, Korea CPI stayed at 2.4% YoY, and Japanese markets priced an 80% chance of a December BoJ hike.

Data today: Euro inflation

Japanese Yields Up, Tariffs Impact on Black Friday, Silver Breaks to New Highs

Morning Macro 1st December

Last week saw one of the strongest weekly cross asset rallies of the year, but this week has started more abruptly to the downside. The catalyst is the surge in Japanese yields 2yr up 5.5bp (that’s 5.5%, a huge rates move) and above 1% for the first time since 2008. Also, the 10-yr yield rose +7bp (4% move), Nikkei is off 2%, Nasdaq futures -0.9%, and Bitcoin -4.4%.

The impact of tariffs can be seen in the Black Friday data, according to Salesforce. Average selling prices were up 7% y/y, while order volumes were down 1% y/y.

Japan’s Finance Minister says it is “clear” the yen swings aren’t “moving based on fundamentals” Bloomberg.

Silver breaks to new all-time highs. YTD Silver +97%, Bitcoin -6.5%.

French PPI -0.8% YoY (prior +0.1%)

German unemployment 6.3% (prior 6.3%)

Intel jumps 10% on Friday on NO new news. Rumour has it Google will produce its TPU’s in US in partnership with Intel. (a huge blow to Nvidia).

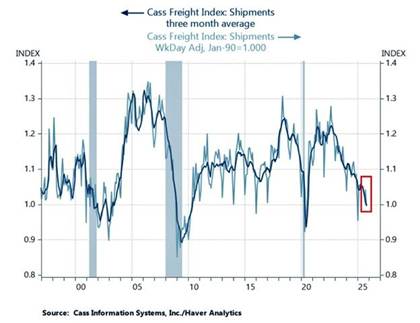

October 2025: The Cass Freight Shipments Index falls 7.8% year over year. The lowest October reading since the depths of the 2009 financial crisis.

Data this week

Monday – EZ, UK, US mfg PMI,

Tuesday – EZ CPI & unemployment

Wednesday – EZ, UK, US services PMI, US ADP, Aussie GDP

Thursday – EZ Retail sales, US jobless claims

Friday – EZ GDP< Canada employment, US PCE deflator and UMich sentiment

Market Reacts to UK Budget, Chicago PMI Falls, Precious Metals, US Margin Debt

Morning Macro 27th November

No key global news sees risk rally on positive flows, S&P500 now just 1.5% below all-time highs, Bitcoin at $91.4 has rallied 13% from the lows, bonds rally both sides of the Atlantic, most shorted stocks rise (Beyond Meat +19% on the day), precious metals rally with silver close to ATH 54.46., and nicely correlated, margin debt makes new record highs!

The market reacts favourably to the UK budget, ‘better than expected’! Bonds and the Pound rallied. A mix of 88 different fiscal policies. GDP growth forecast down, inflation forecast up, tax burden the highest on record, and only a marginal rise in the fiscal buffer. From a macroeconomic standpoint, the government and the Office for Budget Responsibility (OBR) forecast that the new measures — combined with public spending discipline will bring debt down as a share of GDP by 2030–31, aiming to restore long-term fiscal stability. The pound rallied 0.5% against the dollar, with the 10-year bond yield falling 10bp, a big sigh of relief. The market now focuses back on employment with 10 yr yield creeping down towards key 4.38% support (Chart 1, Bloomberg), with a Dec 18th BOE 25bp cut fully priced and 66 bp of cuts priced over the next 12 months.

JP Morgan Chairman & CEO Jamie Dimon backs Rachel Reeves after the budget with an announcement to build a new HQ in London: “The UK government’s priority of economic growth has been a critical factor in helping us make this decision.”

Chicago PMI falls to 36.3 (est. 45.5), deepening what is now a two-year contraction in Midwest business activity. It starkly illustrates the continued dominance of services growth over a struggling manufacturing sector, and it points to the growing importance of AI-related spending in driving economic activity. Positive news was a fall in weekly jobless claims to 216k (est 225k)…… U.S. 10-year falls to below 4.00%.

YoY % Change in Home Prices in U.S. (via Zillow)… Miami: -3.1% Jacksonville: -4.4% Orlando: -4.5% Port Saint Lucie: -4.7% Tampa: -5.1% Fort Lauderdale: -5.3% West Palm Beach: -5.9% Key West: -6.9% Naples: -7.8% Sarasota: -9.7% St Petersburg: -9.9% Cape Coral: -10.4% Fort Myers: -12.1%…… this directly hits consumer confidence and retail spending.

Precious metals continue their rally. Silver targets 54.46 breakout level. (Chart 2, Bloomberg)

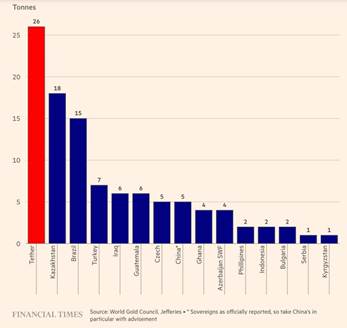

The stable coin Tether bought more gold than every central bank last quarter (Chart 3, FT, World Gold Council)

Berkshire Hathaway’s cash position is now almost 30% of their total assets, highest on record.

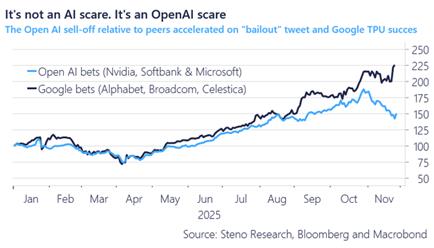

It’s not an AI scare. It’s an OpenAI scare. (Chart 4, Steno Research, Bloomberg, Macrobond)

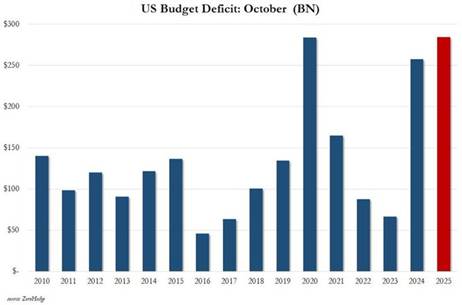

The US Treasury posted a $284.4 billion deficit in October, the worst opening month to any fiscal year in history.(Chart 5, ZeroHedge)

US margin debt jumped +$57.2 billion in October, to a record $1.2 trillion. This marks the 6th consecutive monthly increase. Margin debt for trading has risen +$285 billion, or +32%, year-to-date. Over the last 6 months, margin debt has surged +39%, the biggest jump since 2000. This has been an even larger increase than during the 2021 meme stock mania…. What could possibly go wrong? (Chart 6, FINRA)

U.S. Thanksgiving holiday today.