Morning Macro 8th December

Key trends continue, copper rises another 0.5%, AUDUSD rallies for its 12th consecutive day, and Japanese yield continue their uptrend, dragging global long end yield with them.

Three notable data points from the US on Friday:

- Consumer Confidence: While current conditions fell to the lowest levels since 1930’s, sentiment rose for the first time in nearly six months, climbing from 51 to 53.3 (above the consensus estimate of 52).

- Inflation Expectations: Consumers now expect inflation at 4.1% over the next year and 3.2% over the next 5–10 years.

- September Core PCE: The Fed’s preferred inflation gauge eased to 2.8% from 2.9%, coming in slightly cooler than expected. The headline PCE measure ticked up from 2.7% to 2.8%, matching consensus.

September PCE Price Index +2.8% y/y vs. +2.8% est. & +2.7% prior … core +2.8% vs. +2.8% est. & +2.9% prior (Chart 1, Bloomberg)

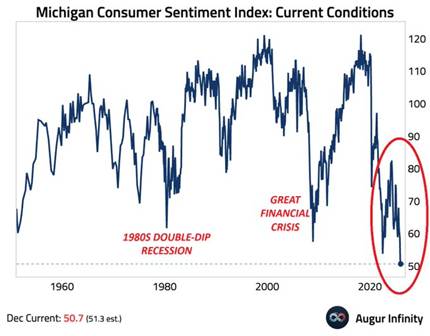

December Uni Mich Consumer Sentiment Index up to 53.3 vs. 51 prior; Current Conditions down to 50.7 vs. 51.1 prior (Chart 2, Augur Infinity) an all-time low and worst perception of the US economy since the 1930s Great Depression.

Meanwhile, Expectations up to 55 vs. 51 prior and short- and long-run inflation expectations fall to 11-month lows

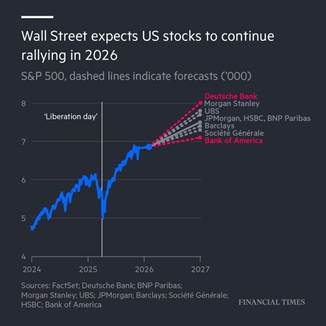

Wall Street banks expect US stocks to post another year of double-digit gains in 2026.(Chart 3, FT)

Soon all commodity charts will look like gold – BofA’s Harnett

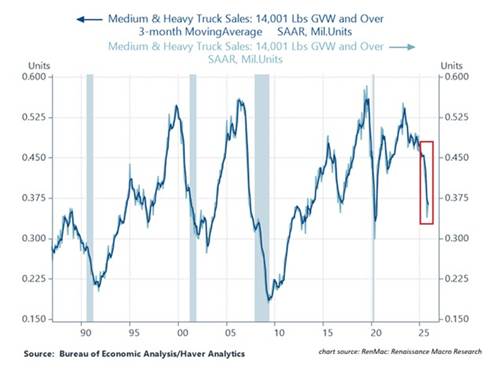

US heavy truck sales have plunged -47% over the last 3 months compared to the prior 3 months, to an annualized rate of 363,000, the lowest since the 2020 pandemic. Truck sales have now declined in 4 out of the last 5 months. (Chart 4, RenMac ,Haver Analytics, Bureau of Economic Analysis)

On appositive note, another surprise surge in Canadian employment for a third month in a row Canada added 53,600 jobs in November compared to estimated loss of 2,500 jobs The unemployment down CAME DOWN to 6.5% from 6.9%

Data this week:

Monday – US consumer inflation expectations

Tuesday – UK retail sales, RBA rate decision, US ADP, retail sales.

Wednesday – China inflation, FOMC rate decision

Thursday – SNB rate decision

Friday – UK GDP & IP