Morning Macro 8th September

With Friday’s weak payrolls data, the narrative has now changed. The Fed isn’t cutting into strength anymore; it’s cutting into weakness. The OIS/futures market is pricing a chance the Fed cut by 50bp on 17th September, market currently pricing 28.5bp. Gold made new all-time highs while equities which had jumped at the open, then sold down after the data.

The US Job Report for August was the weakest since the 2020 crisis. The US economy added only 22K jobs last month. June was revised down by 27K to -13,000, the first negative print since 2020. The 3-month average fell to 29K, the lowest in 5 YEARS………

Also to make matters worse, all jobs’ gains were part time. Full-time jobs: -357K Part-time jobs: +597K……..

Also, fewer than half of the industries in the Bureau of Labor Statistics’ payroll employment survey have added to payrolls over the past 6 months. As is evident in the graph below (Chart 1, BLS, Moody’s Analytics) this only happens when the economy is in recession.

Over the weekend China released data showing that its central bank has increased its gold holdings for the tenth consecutive month. Coinciding with a new all-time high on Friday, and another today.

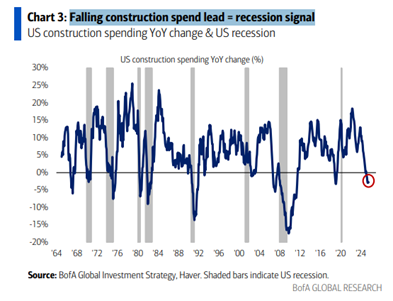

Hartnett BofA: Falling construction spend lead = recession signal (Chart 2, BofA Global Research)

Japanese PM Ishiba announces his resignation with the LDP party announcing leadership elections on Oct 4th. Yen takes a hit down -0.5%.

Japan’s Q2 GDP revised higher to 2.2%, fifth straight quarter of growth – recap

BLOOMBERG: US ALCOHOL CONSUMPTION DROPS TO RECORD LOW, RAISING DEMAND RISKS FOR SPIRITS & BEER COMPANIES

Nvidia is no longer the only choice, meet Broadcom…… the market mourns the loss of a monopoly (Chart 2, Bloomberg, @HayekAndKeynes)

This week’s data –

Tuesday – UK BRC retail sales, Australian consumer confidence

Wednesday – Chinese inflation data, US PPI & mortgage applications

Thursday – Japanese tankan & PPI, ECB interest rate decision (expected unchanged), US CPI

Friday – Chinese M2 money supply, US Michigan consumer expectations