Morning Macro 19 September

Yesterday’s 10-year TIPS auction lacking demand. Bid/cover ratio was 2.2 – the lowest since summer 2022. 10-year treasury sold off and the yield is now trading around 4.13%, up from sitting just above 4% pre-FOMC.

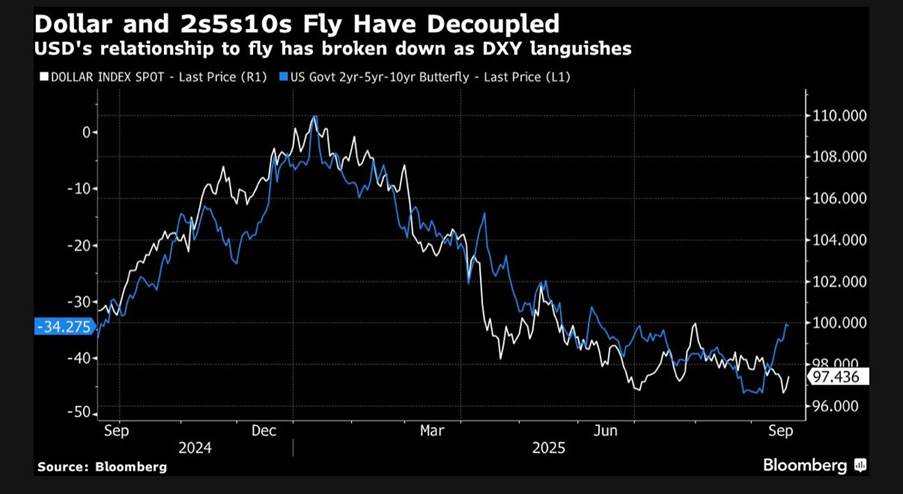

The DXY and 2s5s10s fly correlation breaks down (Figure 1). DXY remains depressed despite bouncing back due to Powell’s slightly more hawkish tone at FOMC on Wednesday.

The S&P 500 hit an intraday record high at 6656 points, now up 37.6% from April low! But for international investors, dollar depreciation had reduced returns; in EUR and GBP terms, it is lower than pre-Liberation Day. (Figure 2)

The Bank of England held rates at 4%, despite two dissents. Governor Bailey hinted towards more upcoming cuts; OIS pricing 36 bps of cuts over next 12 months. Trump and Starmer announce US-UK technology partnership during state visit. Focussing on AI development and nuclear energy, Microsoft will invest $30 billion and Google $6.8 billion into UK technology and research. Total pledged investment by US companies in the UK is $204 billion. This is a Memorandum of Understanding, so is not legally binding and is only a promise to cooperate.

US stake in Intel produces $5 billion profit! Trump announced 10% US stake in Intel at end of August and Nvidia revealed $5 billion investment and chip manufacturing partnership yesterday, sending Intel share price up 30%! (Figure 3)

Japan inflation as expected at 2.7% y/y in August, down from 3.1% in July. Core measure also 2.7%. Government subsidies to electricity prices put significant downward pressure but food prices rose 7.2% y/y. The Bank of Japan held rates at 0.5% at this morning’s decision.

Germany now in serious deflation: August PPI -2.2% y/y, far below expectations for -1.7%. This is the 6th consecutive decline and accelerated from -1.5% in July. Much lower energy costs weighed on the data.

No significant data today.