Morning Macro 29 September

Poland scrambled jets and briefly shut airspace on Sunday after a Russian strike on Ukraine that Kyiv said dragged on for more than 12 hours. In Washington, congressional leaders meet Trump today with the clock ticking toward Wednesday’s shutdown deadline. Democrats want healthcare subsidies extended, Republicans want talks delayed – brinkmanship that risks rattling markets further. Trump has also ordered the National Guard into Portland for two months, triggering a lawsuit from Oregon calling the move unlawful.

The dollar is on the back foot, with Morgan Stanley warning investors are underestimating risks in USD/JPY. The bank advises hedging with options into a busy week that features jobs data, potential US shutdown and Japan’s ruling party leadership race. The yen is leading G10 this morning, up 0.5% at 148.67, after BOJ’s Noguchi sounded more hawkish than expected, stoking further speculation of an October hike. (Figure 1)

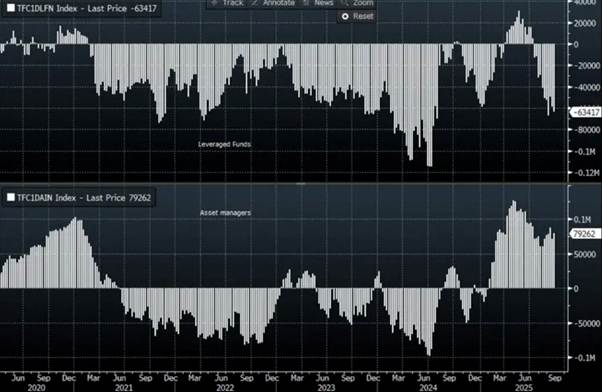

Positioning in yen is split: asset managers lifted JPY longs to +79k, while leveraged funds expanded shorts to -63k. (Figure 2)

Safe-haven flows are also powering metals. Gold hit a new record at $3,819/oz this morning. Prices are 1% higher today after last week’s 2% gain, with support from heavy ETF demand (Figure 3), a weaker dollar, lower 2-year yields and market pricing for almost two Fed cuts by end-2025. Silver extended Friday’s 2% rally with another 2.1% jump to $47.04, supported by tight physical supply and solar demand, though breaks above $47 have proved short-lived. Silvers back outperforming, sending the gold/silver ratio 81.53.

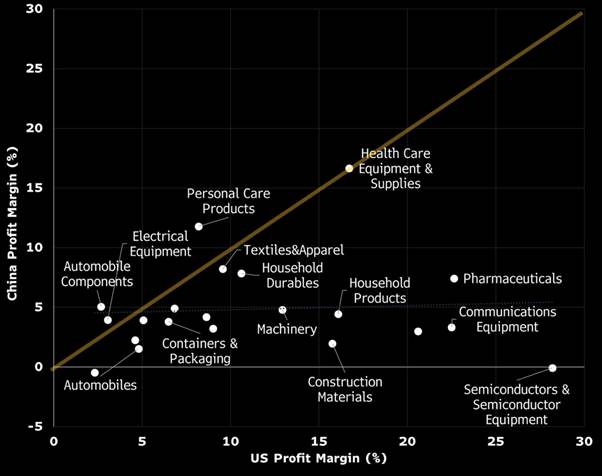

Corporate profitability data highlights the yawning gap between US and Chinese firms. Tradable-goods companies in the US posted average margins of 12.4% in 2024, versus 4.9% in China according to Bloomberg data. High-tech leads the spread: US communications equipment at 22.5% vs China 3.3%, hardware at 20.6% vs 3.0%, and pharma at 22.6% vs 7.4%. Construction and household products also show double-digit gaps, mostly reflecting weak Chinese demand. Margins in consumer goods like textiles (9.6% vs 8.2%) and leisure equipment (4.6% vs 2.2%) are much closer. (Figure 4)

Top heaviness of US stocks continues to spiral, as the top 10% of stocks account for 78% of total US market cap – a record! S&P 500 recovers from its 3-day decline, looks to be consolidating near all-time highs. After Turkish Airlines’ commitment to buy over 200 Boeing planes, Boeing share price jumped to over $220 again, up more than 3.6% in Friday trading.

Data today: Spain inflation, EA economic sentiment, India industrial production, US pending home sales.