Morning Macro Wednesday 13th October 2025

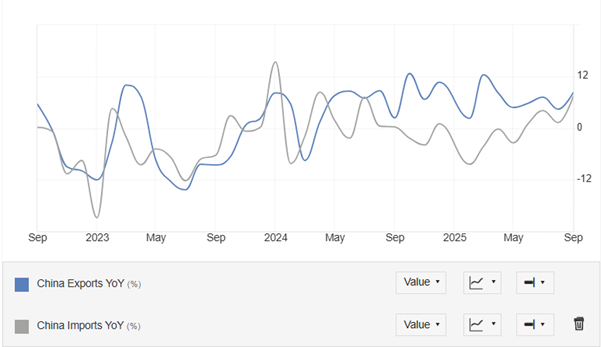

China’s September trade data surprised sharply to the upside. Exports surged 8.3% y/y to $328.6bn, well above the 6.6% consensus, while imports rose 7.4% y/y, beating expectations for 1.8% and reversing August’s soft patch (Figure 1, TradingEconomics). The strength points to resilient global demand and aggressive front-loading ahead of possible tariff escalations. Still, beneath the headline, the geographic breakdown tells the real story: exports to the US collapsed 27% y/y, extending August’s 33% plunge, while shipments to the EU jumped 14.2% and those to Southeast Asia 15.6%, underscoring how China is rerouting supply chains around American tariffs.

The rare earths trade – the latest flashpoint in the US-China standoff – fell 31% m/m in September, nearly halving from June’s record. Beijing’s grip on these critical minerals has clearly rattled Washington; the Pentagon has reportedly moved to stockpile up to $1bn of key metals used in defence manufacturing. Meanwhile, China’s iron ore imports hit 116m tonnes in September, up 10.5% m/m, marking the strongest inflow in four months as steel demand stabilised.

Markets reacted violently on Friday as trade war rhetoric peaked. Beijing had launched an antitrust probe into Qualcomm, imposed new port fees on US-owned vessels, and restricted exports of certain battery components – And Trump reacted in usual fashion by threatening another 100% tariff.

10-year US Treasury yields sank, gold hit fresh records, and equities sold off hard. But weekend comments from both sides struck a de-escalatory tone – TACO time. Trump said on Truth Social “Highly respected President Xi just had a bad moment. He doesn’t want Depression for his country, and neither do I.” That tone was enough to lift S&P mini futures +1.3%, reversing part of Friday’s 2.7% slump, which was itself the steepest drop since April (Figure 2, Bloomberg).

Still, Asia opened bruised. With Japan closed, China set the tone: the CSI 300 slid another 1.7%, adding to Friday’s 1.9% fall – the worst two-day stretch since April’s trade war flare-up. The Hang Seng tumbled 3.3%, slicing through the 20- and 50-day EMAs and now flirting with the 100-day level.

Gold briefly dipped early in APAC hours on Trump’s softer rhetoric but snapped back above last week’s record to $4,060/oz. Silver surged 2.3% to $51.47, clearing its all-time high on tight liquidity in London and renewed safe-haven buying (Figure 3, Bloomberg). Bitcoin also clawed back ground, trading around $115,000, after tumbling below $105,000 post-tariff threat.

Data today: India inflation