View: Neutral-to-Bearish

Target Price: $63-65/bbl

The M1 Brent futures contract has been fairly uninspired this week, hovering just below the $65/bbl handle. Price volatility remains tepid and it seems players are done digesting the sanctions on Russian majors and is now choosing to ignore last week’s US crude draw and OPEC+ pausing its supply hikes in Q1 2026. The threat of a supply glut continues to loom over prices in true Damoclean fashion, while newfound uncertainty stems from reports of a possible US war with Venezuela, which President Trump has said he doubts will happen. Hence, we expect players to reassess their positioning amid this surge of uncertainty, with prices anticipated to sit between $63/bbl and $65/bbl this week. Still, such declines in volatility often leave prices primed for a break-out in the medium term, and we thus recommend monitoring critical short-term support at $62/bbl and resistance above $65/bbl, as we await news on ADP jobs data (amid a government shutdown) and further developments in US crude oil inventories on Wednesday.

Key drivers of prices this week:

- Positioning hits a reset button

- Weaker demand signals from Asia

- Oil supply remains high

Positioning hits a reset button

CFTC data for the week ending 28 Oct reported a decline of over 77mb in Brent futures open interest, confirming that the post-sanctions rally was driven by an exodus of shorts, spurring expectations that we may now see a near-term equilibrium as players assess their next step. Flux Insight’s CTA positioning model reflects this decline in risk appetite, with net length in Brent inching up from -18.9k lots on 28 Oct to a projected -17.1k lots on 3 Nov. A technical view cements this, with the RSI trailing sideways from 49 this week and the MACD histogram, though positive, now narrowing d/d. With open interest sitting above 3mb, well above the 5-year maximum, price remains vulnerable to further stop outs in either direction, though it appears players are presently awaiting further direction.

Weaker demand signals from Asia

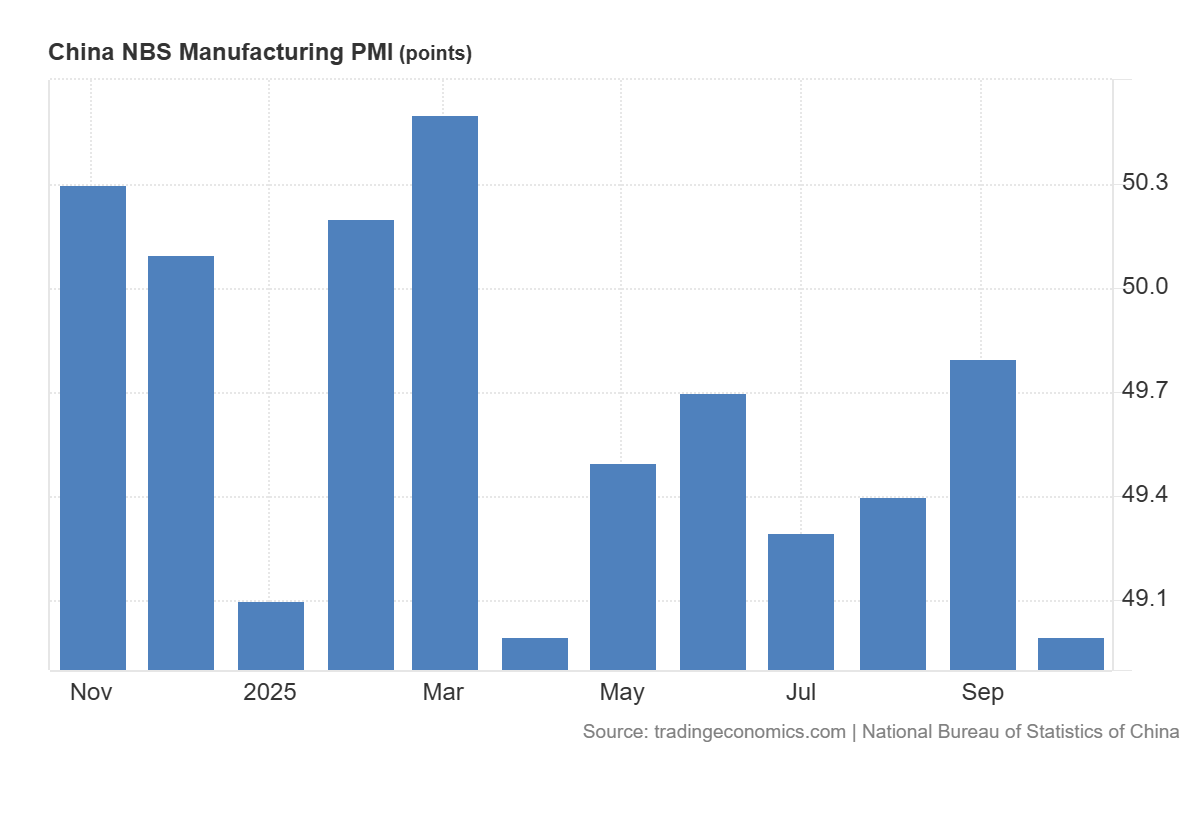

Further uncertainty likely stems from a mixed demand-side picture from Asia. While India’s manufacturing activity climbed to a higher-than-expected 59.2 in October amid higher demand around Diwali, new export orders increased at their slowest rate in 10 months. China’s official manufacturing PMI slid to 49.0 in Oct 2025 (prev: 49.8). The RatingDog General Manufacturing PMI, which covers smaller, export-oriented firms, also eased below expectations, with export sales declining at their fastest pace since May. South Korea’s manufacturing PMI fell into contraction territory after briefly expanding in September. Although recent trade deals with Washington may stymie further declines in factory activity in East Asia, uncertainty looms large.

Oil supply remains high

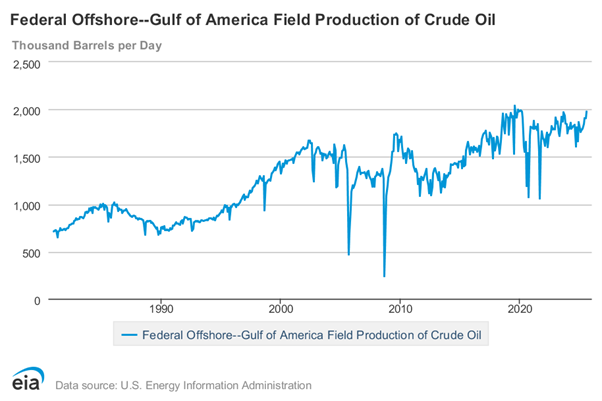

Although OPEC+ has announced a pause to supply hikes in Q1 2026 alongside compensation plans from overproducing countries, the market has largely chosen to ignore this, with the Jan/Feb’26 spread easing from above $0.60/bbl to $0.50/bbl at the time of writing on 3 Nov. Moreover, though overall US crude inventories sit just below the y/y average, crude oil production from federal waters in the Gulf of America (formerly the Gulf of Mexico) climbed to an average of 1.98mb/d in Aug 2025, its highest level since 2019. Elsewhere, the Indian Oil Company has stated it will continue to buy Russian crude, stressing that the crude itself is not sanctioned if complied with sanctions placed on individual entities and the price cap. Should more refiners follow suit, we could see an unwinding of some of the geopolitical risk premia that has recently supported prices.