Morning Macro 11th November

Nasdaq closes +2.2% higher, S&P500 +1.5% higher, gold +2.9% higher, but UK bond yields open the day 5bp lower on another set of weak employment data.

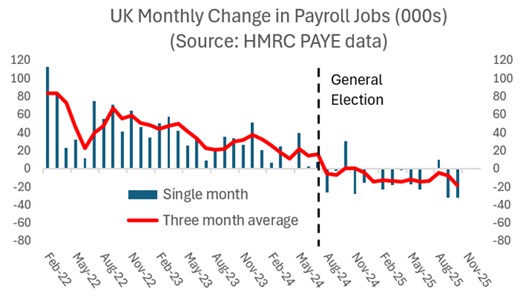

The headline UK unemployment rate has continued to increase steadily since Labour took power, from 4.2% in the three months to June 2024 to 5.0% in the 3m to September 2025 (highest since 2021), and since July 2024, the number of payroll jobs has fallen by 178,000. This is what happens to unemployment if you pay people more not to work, pay people less to work and tax people more for employing other people to work? (Chart 1, @julianHjessop)

FED’S MIRAN said: – 0.50% cut appropriate for December, 0.25% at a minimum….. Meanwhile the OIS prices 16bp cuts for December.

More credit market losses slowly emerging (Chart 2, Bloomberg)

The critical issue of power is gaining traction in the US. Microsoft CEO admitted in an interview on Monday that thousands of GPUs were sitting idle in data centres because there isn’t enough energy to run them. The real constraint isn’t computer capacity, but electricity and space…… Now two state of the art Nvidia data centres stand empty and idle, awaiting electricity availability. (Chart 3, Bloomberg)

10 yr JGB yield closed at highest since June 2008. This is a concern for global bond yields as the debt sustainability story comes back to the forefront (Chart 4, Bloomberg).

The US freight recession is deepening: the US truckloads index has fallen to its lowest level since 2014, as fewer goods are being moved across the country.

Data today – German ZEW, US ADP & NFIB Small Business Index data