Morning Macro 24th November

Friday’s markets were driven by the ‘will they – wont they’ focus on the Fed at the 10th Dec meeting. FEDs Williams comment ‘still sees room for a near-term rate cut’ threw the market solidly into a rate cut expectations, with the overnight index swap (OIS) market jumping from 33% to 77% chance they cut. Equities rallied on that news into the weekend and have started this week stronger. Meanwhile US consumer sentiment, has fallen to one of the lowest levels on record. The final November sentiment index dropped to 51 from 53.6 in October, according to the University of Michigan. Views of personal finances were the dimmest since 2009.

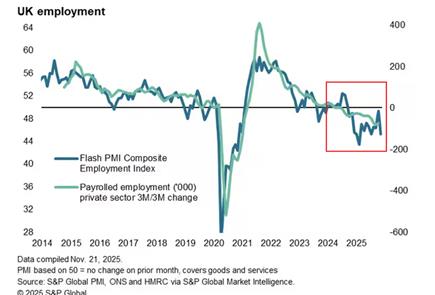

Friday’s flash UK PMI for November signalled a renewed acceleration in job losses in the private sector, largely due to rising labour costs and additional pre-Budget uncertainty (Chart 1, S&P global, ONS, HMRC)

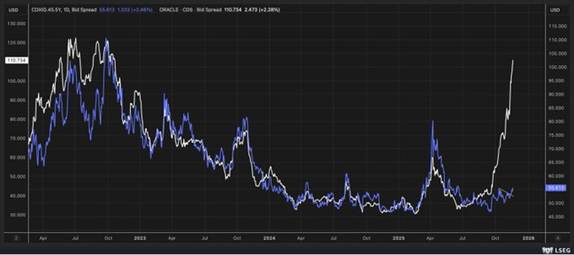

Is Oracle the outlier or the canary in the coalmine? Here is Oracle CDS versus IG spreads (Chart 2, @MichaelMOTTCM)

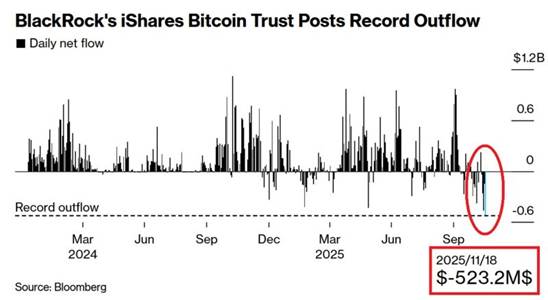

Investors are DUMPING Bitcoin funds at a RECORD pace. Bitcoin ETF $IBIT saw -$523 MILLION in net outflows on Tuesday, the highest EVER. In 5 days, investors withdrew over $1 BILLION from $IBIT. Over the last 3 weeks, crypto funds have seen $3.2 BILLION in net outflows.

Chart 3, Global Markets Investor, Bloomberg, Charles Henry Monchau)

Key data this week

Monday – German IFO business confidence

Tuesday – US PPI, retail sales, ADP employment

Wednesday – UK budget, US jobless claims, PCE inflation, jobless claims, new home sales, Aussies inflation

Thursday – US holiday, UK budget

Friday – Japan CPI, unemployment & retail sales