Morning Macro 10th December

The focus today is firmly on the FED meeting, and more importantly what Chair Powell says after the 25bp cut. Long end yields are on the grind higher again, if the market fears reckless cuts at the front of the curve, then long end yields will continue higher, with equities already taking notice and losing momentum and silver rallying another 5.7% in 2 days. Long end yields are IMHO the biggest risk to financial markets in Q1 2026.

Investment in the Nasdaq 100 has climbed to around $32.5T, up from $12.5T just three years prior. Precious-metals equities have likewise jumped, doubling from $300B to over $600B in only twelve months. When even small amounts of capital begin moving into hard assets, the impact is large. And to put in context gold is a mere 2.8% of investors AUM.

YTD Silver +103%, Gold +59%, Bitcoin -3%!

The National Federation of Independent Businesses survey for prices just posted the biggest one month jump in the history of the survey.

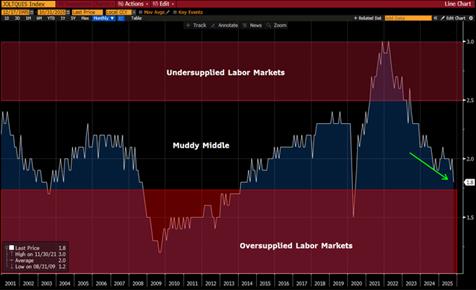

While yesterday’s JOLTS (job openings) rate ticked up the bigger story is the QUITS rate fell sharply, and at 1.8% (lowest since May 2020) this is heading towards oversupplied territory (Chart 1, @lebas_janney, Bloomberg).

Chinese inflation falls back into deflation, CPI -0.1% MoM, +0.7% YoY, PPI -2.2% YoY.

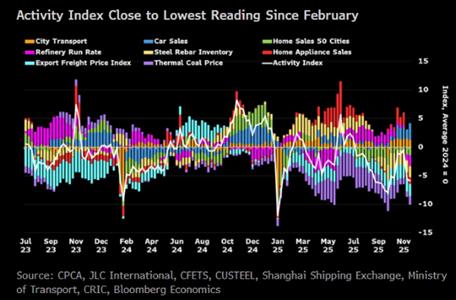

Economic activity in China likely slowed further in November, with the high-frequency index and dashboard showing a sharp drop in the second half of the month. Sales of new homes and home appliances led the deterioration in demand, with new-home sales falling 41% year on year in the four weeks through Nov. 28. (Chart 2, @dlacalle_IA, Bloomberg economics)

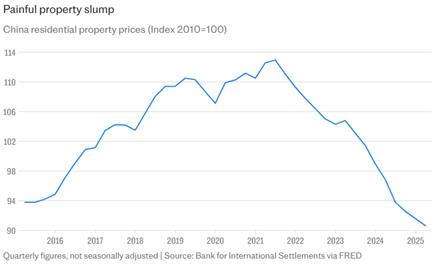

More Chinese data censorship. While China’s property slump continues Beijing had told the two private sector housing data agencies (China Real Estate Information (CREI) & the China Index Academy) to withhold the numbers until further notice. (Chart 3, Telegraph, BIS, FRED)

JPMorgan fell nearly 5% yesterday after the bank told investors that it will spend billions of dollars more in expense.

Bullish investor sentiment is surging, in fact the gap between bullish and bearish readings jumped to 13.5 points, the 2nd-highest this year. (Chart 4, Bloomberg, zerohedge)

Trafigura Chief Economist Saad Rahim on oil in 2026: “Whether it’s a glut or a super glut, it’s kind of hard to get away from that…”

AUDUSD higher in 13 out of the last 14 days. OIS has 31bp hikes priced for the RBA over the next 12 months and 77bp cuts priced by the FED. Interest rate differentials matter.

Data today – Chinese inflation, Fed and BK of Canada rate decisions, Oracle & Broadcom earnings.