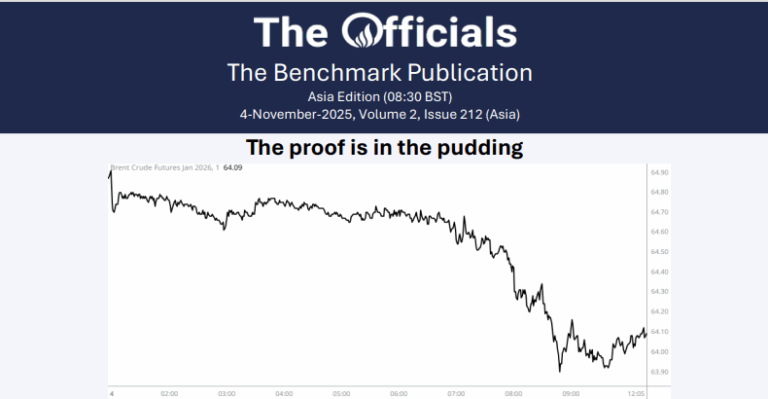

Longest US Shutdown Hits 6 Weeks as Flight Cuts Loom; Global Stocks at Record Highs

Morning Macro 6th November:

We are officially in the longest US shutdown in history – consensus estimates are that shutdown would cost the economy around $15 billion each week; we have now entered the 6th week of the shutdown! Meanwhile, the US Department of Transportation announces mandatory flight cuts at major airports from Friday. The US may cut air traffic by 10% if no deal is reached to end the shutdown.

The US Supreme Court heard arguments this week on the legality of Trump’s sweeping tariffs, and many justices looked sceptical. Polymarket is now pricing only a 30% chance of the Court ruling in favour of Trump! If the tariffs are ruled out, this would cost the US around $30 billion per month in lost revenue!

But elsewhere the party is still going – the question is how long until the music stops? Globally the proportion of stock indexes at an all-time high is the highest since 1999! (Graph 1, Macrobond)

Now with lacking data in the US, everyone’s attention was on the ADP employment data, which showed that in October, private sector employment rose by 42k, marking the first monthly gain since July and surpassing expectations of 25k. Despite the positive data, US treasury yields didn’t even flinch, showing the little importance ADP data have in the market.

In the Eurozone, PMI data were positive for Spain (56) and Italy (53.1), recording their strongest expansions in over a year, driven by resilient services, new orders, and easing cost pressures. Germany (53.9) showed its fastest growth since mid-2023, supported by a rebound in services despite softer sentiment. Meanwhile France (47.7) remained mired in contraction, reflecting weak domestic demand. Overall, Europe’s private sector recovery is being powered by services strength amid lingering manufacturing weakness. Outside continental Europe, the UK (52.2) also regained momentum, but the expansion was driven by the services sector as the manufacturing side remains in contraction!

And the US showed steady growth on the PMI front too; the S&P Composite PMI rose to 54.6, driven by solid gains in both manufacturing and services activity. New business strengthened and employment edged higher, though confidence slipped to a six-month low. Inflation pressures continued to ease, with costs and prices rising at their slowest pace since April. Meanwhile, the ISM Services PMI climbed to 52.4, signalling the strongest expansion since February. Business activity and new orders rebounded sharply, though employment remained weak amid uncertainty linked to the shutdown.

Data today – Bank of England interest rate decision