Alpha Report: October Review

Another week brings another selection of new trade ideas from Flux Insights. This week, we look at trades in Naphtha and Fuel Oil.

Another week brings another selection of new trade ideas from Flux Insights. This week, we look at trades in Naphtha and Fuel Oil.

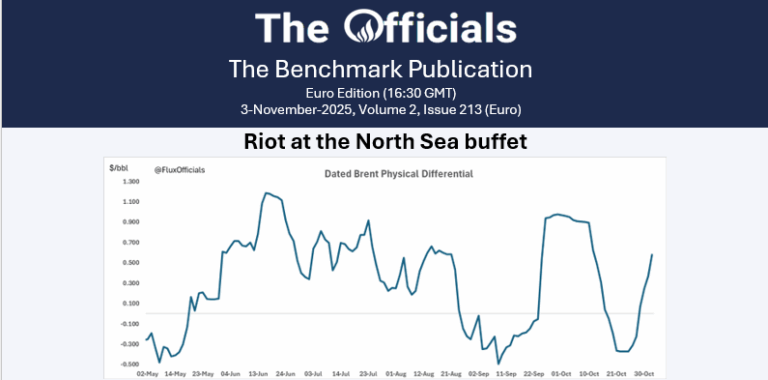

A new month for the market to sink its teeth into and the North Sea started November with a bang! Midland bids and offers were flying around right from the start, with a couple of CIF Ekofisks bids and offers thrown in for good measure, plus some Forties bids too. Phillips, Vitol and Mercuria were all over the window like charging antelopes (bidding or offering).

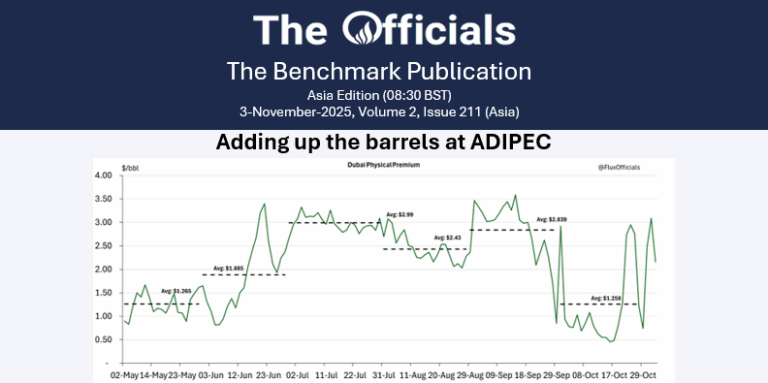

Dear readers, this issue of The Officials is a free taster – attendees at ADIPEC, read on! The loudest noises we’ve detected from the conference so far are that demand remains strong, despite the increasingly noisy super glut narratives being pushed from all angles.

Looking at Flux Insight’s CTA positioning for the week ending 3 Nov, net long positioning in Brent and WTI futures has risen moderately since 28 Oct, reflecting a decline in risk following the exodus of shorts in the week ending 28 Oct. Positioning in Brent and WTI futures remains net short, at -17k lots and -20k lots, respectively, on 3 Nov. Meanwhile, CTA net length in RBOB futures climbed from -25k lots on 28 Oct to a projected -17.7k lots on 3 Nov. Still, the middle distillates complex continues to outperform the remaining futures, with CTA net length in both NYMEX heating oil and ICE gasoil futures sitting at +15.8k lots, up from +10.8k lots and +11.65k lots on 28 Oct, respectively. Nonetheless, this positioning lies at the tail end of historical ranges, which may encourage a mean-reversion of prices in the near-term.

ICE COT data for the week ending 28 Oct shows open interest dropping by over 77mb w/w (marking a 2.5% drop w/w), reflecting that the rally may have been driven by short players stopping out after the sanctions announcement. Open interest sits well above all-time highs at 3mb, hinting at an overcrowded market which may have made it more difficult for these short players to defend their positions following the bullish catalyst in the market.

The Jan’26 Brent futures gapped higher above $65/bbl on Monday morning’s open, seeing highs of $65.30/bbl around 06:40 GMT before sliding towards $64.50/bbl by 09:15 GMT (time of writing). OPEC+ agreed on Sunday to raise output by 137kb/d in December but will pause the output hike in Q1 next year, especially considering the seasonal demand weakness. In other news, Chinese oil refiners (including state-owned giant and smaller private refiners) are buying fewer Russian cargos, which has seen ESPO prices decline, with Rystad estimating around 400kb/d affected by the buyers’ strike. BPCL has switched to Abu Dhabi’s Upper Zakum for December as new US sanctions on Rosneft and Lukoil force Indian refiners to trim Russian intake and turn to Middle Eastern spot barrels. At the ADIPEC energy conference in Abu Dhabi, UAE officials said oil demand is set to rise into 2026, supported by energy needs from data-centres and AI, with OPEC+ pausing planned output increases to avoid oversupply and preserve investment momentum amid sanctions-driven uncertainty around Russian output. Finally, the front (Jan/Feb) and 6-month (Jan/Jul) Brent futures spreads are at $0.54/bbl and $1.16/bbl, respectively.

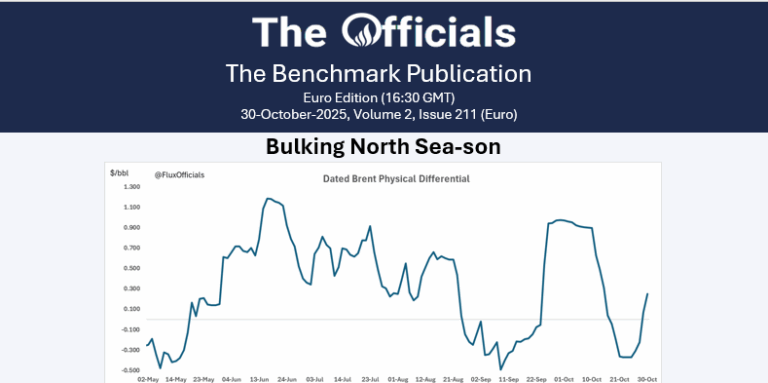

October is at an end! It’s been a hectic month with chopping and changes of market direction and narratives. The super glut narrative is still doing the rounds, though this month it took a new shape: oil on water. Some very wonky-looking data was floating around, suggesting a huge surge in exports but no corresponding surge in imports… Some of the barrel counters and ship trackers are even openly admitting their data should be raising eyebrows!

This report reviews weekly oil inventory data from the US EIA’s Weekly Petroleum Status Report, Global Insights’ ARA Independent Storage and International Enterprise’s Singapore product storage

October is at an end! It’s been a hectic month with chopping and changes of market direction and narratives. The super glut narrative is still doing the rounds, though this month it took a new shape: oil on water. Some very wonky-looking data was floating around, suggesting a huge surge in exports but no corresponding surge in imports…

The Jan’26 Brent futures contract has eased slightly this morning, from $65/bbl at 08:30 GMT to $64.56/bbl at 10:30 GMT (time of writing). In the news, Reuters reported that Indian Oil Corp has purchased five cargoes of Russian oil scheduled to arrive in December, from non-sanctioned entities. According to Reuters sources, the IOC has purchased approximately 3.5mb of ESPO for delivery at an Eastern Indian port, though the sellers were not named. Elsewhere, Saudi Arabia may lower its December crude prices for Asian customers to their lowest levels in several months, due to an abundance of supplies. However, Reuters sources think that the demand to substitute sanctioned Russian energy could restrict the extent of these cuts. According to a Reuters survey, multiple Asia-based refining sources expect the December Arab Light crude price to fall by $1.20-$1.50/bbl, narrowing its premium over Oman/Dubai to 0.70-$1.00/bbl, down from $2.20/bbl. In Budapest, Hungarian PM Viktor Orban has said on state radio that he will need to convince US President Trump that Hungary is exposed to pipeline networks when it comes to energy, in hopes of gaining an exemption from US sanctions on Russian oil; a meeting between the leaders is scheduled for 7 November. In other news, Reuters reports that Russia-backed Nayara Energy in India has increased crude processing at its Vadinar refinery to 90-93% of its 400kb/d capacity after EU sanctions disrupted earlier operations. Finally, at the time of writing, the front-month Jan/Feb’26 and 6-month Jan/Jul’26 spreads are at $0.55/bbl and $0.87/bbl, respectively.

In central banking, following the Fed, the BoJ and the ECB held their policy rates steady at 0.5% and 2%, respectively.

The Euro Area expanded just 0.2% q/q. The third largest economic area is struggling to make meaningful progress! Germany and Italy stagnated, Ireland, Finland and Lithuania contracted, while the growth was led by Spain (0.6%) and, surprisingly France (0.5%) due to a sharp rise in exports. Unemployment held steady at 6.3%, consumer confidence and services sentiment were up, while inflation expectations edged down. Inflation is due to be out today and if the deflation worries continue the ECB will have to cut sooner than expected. The OIS over the next year is pricing below 12 bps – so it shouldn’t come as a surprise if the euro weakens form its current levels (Chart 1, Bloomberg).

The 31st day of the US government shutdown! Earlier estimates had shown that every week could shave off 0.1% from the GDP, so now we are talking about at least 0.4% less for Q4 2025. Speaking of GDP, yesterday’s Q3 GDP wasn’t released, something that makes the job for the Fed even harder.

In Japan unemployment rate picked up to 2.6% and the labour force participation continued declining! Inflation came really hot at 2.8% – above expectations – the markets are slowly ramping up their bets for another hike by the BoJ. Expect the gap on Chart 2, Bloomberg to tighten as the interest rate differential (white line) remains well below historical levels, while the USD/JPY should weaken with monetary tightening. But housing starts and construction orders in Japan remain an issue!

Meanwhile, Chinese PMIs surprised to the downside – with the manufacturing sector contracting (49), while non-manufacturing edged up to 50.1.

Gold demand hit a record 1,313 t in Q3 (+3% y/y), worth $146 bn (+44%), as investors added 222t and central banks holdings were up 28% q/q, while jewellery slumped. Supply also hit records, with mine output up 2%, as gold averaged $3,456/oz (Chart 3, World Gold Council).

The Fed cut rates by 25 bps, but the front end didn’t get the memo – the SOFR rate fixed at 4.27%. Heavy T-bill settlements ($83B this week), month-end balance sheet constraints, and Canada’s fiscal year-end squeezed liquidity. Interest on Reserve Balances – the rate at which banks deposit at the Fed – was at 3.9%, when the spread between the IORB and SOFR is that wide, it screams cash demand is high!

France’s CAC 40 fell 1% as markets soured over a provisional 33% tax on share buybacks passed in a parliamentary vote – a move investors fear will hammer large French firms. SocGen dropped over 5% as traders cut buyback expectations. If the tax is upheld in the final budget, it could undermine Paris as a financial hub and push companies to list abroad. The proposal effectively kills the appeal of buybacks, wiping out a key shareholder-return tool.

Data today – Euro Area inflation, Canada GDP, Fed Governors speeches

$65 is back! Briefly at least, before markets fell back again, slipping just by a cent $64.99/bbl by the close. The prompt spread recovered somewhat again, reaching the European close at 64c. However, the Brent structure is struggling further down the curve again, dipping into contango in the May/Jun’26 spread.

The broader market was waiting for the outcome of the Trump and Xi negotiations as the impact is far and wide. The meeting was a 12 out 10 said Trump, but the details said it was a 3. The two nations essentially agreed to play sort of nice for another year and see then how things are going. Trump said the Chinese agreed to buy anything American but the price of soya beans fell by about 1.5%. If it was s such a good meeting why would the American farmers be so disappointed, we wondered. Regardless, even a fake agreement is better than actual shooting, so we are happy.

The Jan’26 Brent futures contract has dipped this morning, from $64.90/bbl at 04:00 GMT to $64.49/bbl at 10:00 GMT (time of writing). In the news, Reuters has reported that Russia’s Lukoil has agreed to sell Lukoil International GmbH, its international unit overseeing the company’s overseas assets, to Gunvor Trading House. Gunvor has since confirmed it was in discussions with Lukoil regarding the potential purchase of Lukoil foreign assets. In India, state-run refiner Indian Oil is seeking 24mb of oil from the Americas for Q1 2026, per a company document reviewed by Reuters. The tender is seeking both low- and high-sulphur crude grades and is set to close on Friday. Elsewhere, South Korean Chief Policy Advisor Kim Yong-beom has released some details of the UK-SK meeting. Although not yet confirmed by Washington, the statement includes a claim of a 10% reduction in Korean import tariffs, lowering them to 15%. In other news, US President Trump has stated via Truth Social that China has agreed to begin the process of purchasing US energy. Trump alluded to purchases from Alaska, though details are unclear. In his post, Trump mentioned that “the Energy teams will be meeting to see if such an Energy Deal can be worked out.” Finally, at the time of writing, the front-month Jan/Feb’26 and 6-month Jan/Jul’26 spreads are at $0.49/bbl and $0.77/bbl, respectively.

This week, in all three contracts, money managers are anticipated to increase length while trimming shorts. Producers/merchants, in contrast, are expected to be risk-off across the three contracts, trimming both longs and shorts.

Further detailed information on other categories and contracts can be found in the report.