Alpha Report: Lightends Land

Another week brings another selection of new trade ideas from Flux Insights. This week, we look at trades in Gasoline and Naphtha…..

Another week brings another selection of new trade ideas from Flux Insights. This week, we look at trades in Gasoline and Naphtha…..

Looking at Flux Insight’s CTA positioning, positioning in Brent futures trended downward from -34k lots on 14 Oct to -51k lots on 21 Oct before reversing to reach -20k lots on 27 Oct. Like Brent, middle distillate positioning also fell before increasing; NYMEX heating oil fell from -10k lots on 14 Oct to -19k lots on 21 Oct before increasing to +6k lots on 27 Oct. ICE gasoil fell from -11k lots to -22k lots and rose to +4k lots during the same time period. RBOB futures followed the same trend, from -37k lots to -42k lots and back up to -23k lots on 27 Oct. From an index perspective, NYMEX heating oil and ICE LS gasoil are moving towards the overbought territory, perhaps signaling an impending reversal.

In the week ending 21 Oct, Brent futures fell from $63.56/bbl on 14 Oct to lows of $60.40/bbl on 17 Oct amid rising US-China trade tensions and concerns of a supply glut pressuring sentiment. Prices met some support at this level, recovering to $61.32/bbl on 21 Oct.

Open interest increased in the week ending 21 Oct, by 129mb (+4% w/w) to reach 3,103mb.

Net long managed-by-money positioning decreased for the fifth consecutive week, down 58mb (-53% w/w), falling to 51mb. This marks the largest percentage decrease since Oct 2024 and sits well below the yearly and 5-year averages of 186mb and 199mb, respectively. Net long positioning has been pressured by speculative players trimming longs and adding 45mb (+30% w/w) to their shorts, marking the most significant percentage increase in speculative shorts since April 2025.

For the second consecutive week, producers/merchants added to both their longs (+89mb, +8%) and shorts (+57mb, +4%) in the week ending 21 Oct. Across-the-board increases to exposure suggest that these players remained risk-on in the week ending 21 Oct, signalling hedging efforts from producers and refiners.

Other reportable players also remained risk-on in the week ending 21 Oct, adding to longs (+16mb, +9%) and shorts (+1mb, +0.31%). This increase in length may reflect these players providing liquidity to the risk-off speculative longs.

Who’d have thought when you sit down and talk you can have a breakthrough! After all the palaver, they managed to find common ground. Markets loved it: S&P 500 futures jumped 0.8% to a record high and Brent opened 40c up. Yet, through the Asian session, Brent fell to $65.48/bbl by the close, despite the prompt spread holding steady at 76c.

The Dec’25 Brent futures contract has fallen this morning, from $66.40/bbl at 06:00 GMT to $65.08/bbl at 09:00 GMT. Prices met some support here, rising to $65.29/bbl at 10:30 GMT (time of writing). In the news, US Treasury Secretary Scott Bessent has said that the US and China have sketched out a preliminary trade deal framework, which would defer China’s rare-earth export controls and avoid 100% tariffs on Chinese goods. The trade deal is subject to approval ahead of the Trump-Xi summit on Thursday. In Iraq, Reuters reported an oil pipeline fire on Sunday at Iraq’s Zubair oilfield (capacity 400kb/d). While five workers suffered injuries, no disruptions to the refinery were reported. This morning, Iranian Oil Minister Hayan Abdel-Ghani has said that Iran’s total oil exports currently sit at 3.6mb/d, undisrupted by the fire. Elsewhere, western pressure on Indian oil imports has the country intensifying oil and gas explorations, according to the Indian energy ministry. In a Bloomberg report, the IEA has suggested that oil prices will ‘moderate’ amidst increasing output in the Americas. Finally, at time of writing, the front-month Dec/Jan’26 and 6-month Dec/Jun’26 spreads are at $0.72/bbl and $1.90/bbl, respectively.

Equities began the week on a constructive note following productive US-China trade talks over the weekend. The discussions covered a broad range of topics, including export controls, shipping, fentanyl, and agriculture. China may resume “substantial” soybean purchases and defer its rare earths export controls for a year, while the extra 100% tariffs on Chinese goods threatened by Trump are likely off the table. The upbeat tone has raised hopes of an extended trade truce, creating a positive framework ahead of Thursday’s high-stakes summit between Trump and Xi. The sanguine tone weighed on gold as prices extended its decline, retreating by 1% on Monday morning (Chart 1, Bloomberg)

Argentine President Javier Milei’s libertarian party won a landslide victory in Sunday’s midterm elections. His gains will help him accelerate structural reforms, including deregulation and reducing spending. Before the vote, the US had pledged up to $40bn of support for Argentina, including a $20bn central bank swap line and plans for a $20bn loan facility to purchase Argentine debt, which was contingent on the election outcome. Following this, Argentine assets are expected to recover, led by dollar bonds, and the peso, which saw increasing volatility and weakness ahead of the vote (Chart 2, Bloomberg).

US inflation has hit 3% for the first time since January last month; however, this was less than the expected 3.1%. The inflation figures resulted in a ‘dovish cut’ tone, driving the S&P 500, Nasdaq, and Dow Jones to new all-time highs. A 25bps cut is all but priced in for this week’s Fed meeting, to bring the rates down to a 3.75% to 4% range (Chart 3, Bloomberg). The odds of a December rate cut have been raised from 91% to 98.5%, according to the CME FedWatch tool. Nonetheless, the US 2-year and 10-year Treasury yields remained sticky at the 3.5% and 4% levels, respectively. A University of Michigan survey showed consumer sentiment cooled in October at 53.6, the lowest reading in five months.

Data today: German IFO business conditions, US Durable Goods Orders, South Korea GDP.

Big week for earnings – Microsoft, Google, Meta, Apple, Amazon. Oil majors: Exxon, Chevron, Shell.

This report reviews weekly oil inventory data from the US EIA’s Weekly Petroleum Status Report, Global Insights’ ARA Independent Storage and International Enterprise’s Singapore product storage

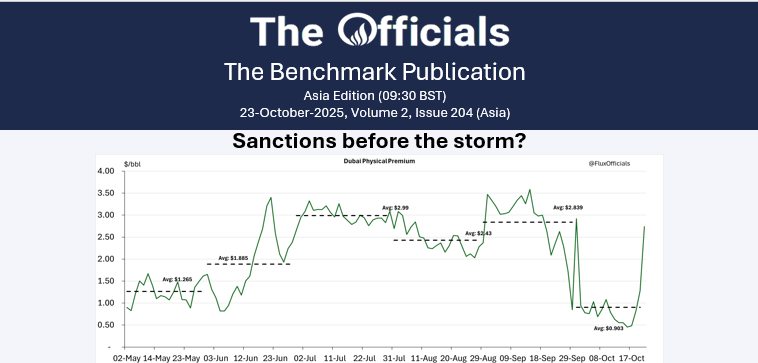

There are sanctions, countersanctions and workarounds. Anybody thinking the consumers do not like the Russian black stuff, better get a job writing comics or at a Swiss cheese factory. The alternatives always bore through; it just takes a bit of time. Hungary is already looking for workarounds – and admitting it publicly! It took literally a day. The oil will leak out eventually one way or another. That being said, the Europeans are still set on plugging as many gaps as they can – with a few conveniently placed loopholes. Meanwhile, Starmer said, with a straight face, “We are choking off funding for Russia’s war machine.”

The mania has eased and we are back in the $65-70 range, or at least at the bottom of it. Markets are like wild animals and they like to get out of the pen, but they get lassoed and pulled back to where they belong. The market is not long anyway, and we recognise credible data is so hard to come by. And one of the few points we still kind of trust is the US inventory data. Please use your grey matter and tell us why the market is long. Swimming in oil and inventories are really at the bottom end of a multi-year cycle. We are willing to listen, but really, where is the surplus?

The Dec’25 Brent futures contract rose this morning, from $65.58/bbl at 05:00 BST to $66.28/bbl at 09:30 BST before easing to $65.93/bbl at 11:00 BST (time of writing). In the news, Reuters has reported that US sanctions on Russia-owned NIS have blocked the Serbian oil company from receiving a crude shipment. According to Reuters sources, NIS faces closure in November without new supplies. However, Serbian President Aleksandar Vucic has said that existing stocks are sufficient until the end of this year and reassured the public that crude shortages were not on the horizon. In Singapore, Indonesia’s Chandra Asri Pacific has said that it will procure nearly 60 Esso-branded petrol stations from ExxonMobil by the end of this year. Chandra will continue using the Esso brand, purchase fuel supply from Exxon, and take on Exxon staff who run the business. In other news, according to Vortexa, freight rates have surged across segments as transited oil reaches its highest level in five years. The data suggests that total crude and condensate in transit reached 1.3mb/d in October, driven by delays on sanctioned oil cargoes destined for China and India. In addition, VLCC rates have bounced to $82-85k. In the US, the Trump administration has announced the full restoration of the 1.5mn-acre Coastal Plain in Alaska for oil and gas drilling, as well as reinstating previously cancelled leases held by the Alaska Industrial Development and Export Authority. In other news, President Trump has terminated all trade negotiations with Canada following an ill-received Canadian government advertisement. The advert, featuring remarks of former US President Ronald Reagan and criticisms of US tariffs, was deemed ‘fake’ by President Trump in an X post. Finally, at time of writing, the front-month Dec/Jan’26 and 6-month Dec/Jun’26 spreads are at $0.73/bbl and $2.24/bbl, respectively.

Equities and precious metals both fell again (S&P500 -0.5%, Nasdaq -0.9%) as subprime bankruptcies emerge, banks warn about private credit risks, US imposes new sanctions on Russia and Trump threatens new export restrictions on China. I’m trying not to get too bearish but I’m struggling to find any good news, S&P500 and Nasdaq could be forming double tops here, but bonds are clearly telling a bearish market story, the OIS prices 116bp of cuts over the next year.

Gold and silver are now in a short term down trend, don’t listen to me, look at the charts and short-term moving averages. Leveraged positions have taken heavy losses over the last 2 days. ‘When a speculative bubble pops. The really bad losses are taken in the next two months as those who missed it buy the dip’ (Andy Constan @dampedspring)

A growing number of states are struggling, some already in recession, others right on the edge. Together, they account for nearly a third of U.S. GDP. The national economy isn’t there yet, but it’s clearly losing steam. (Chart 1, Mark Zandi, Moody’s Analytics)

Volatility in the AI Revolution is heating up. Quantum stock fell 20% on news of Google’s Willow Chip solving problems 13,000x faster than the best supercomputer using a new algorithm called Quantum Echoes. Then the quantum stocks rallied back 20% after hours on news that the Trump Administration is preparing equity stakes in quantum stocks. It would be unprofessional of me to suggest that they may be trying to prop up another corner of the equity market for another week…… *IONQ, RIGETTI, D-WAVE IN TALKS FOR GOVT. TAKING STAKES: WSJ …. NOTE: These companies trade at 200–900× forward sales — far above dot-com bubble levels. Analysts warn the sector is “disconnected from fundamentals.”

17 years after the financial crisis another subprime lender has gone under. PrimaLend Capital Partners filed for bankruptcy after months of negotiations with creditors, a sign of stress in a sector catering to low-income consumers

IT’S `PARTY LIKE IT’S 1999′ IN CREDIT MARKETS: JIM CHANOS

*US TARGETS ROSNEFT, LUKOIL IN LATEST ROUND OF RUSSIA SANCTIONS

*OIL JUMPS AS MUCH AS 2.5% AT OPEN AS US SANCTIONS RUSSIAN FIRMS

TRUMP ADMINISTRATION CONSIDERING PLAN TO RESTRICT GLOBALLY PRODUCED EXPORTS TO CHINA MADE WITH OR CONTAINING U.S. SOFTWARE; NEW EXPORTS CONTROLS COULD CURB EXPORTS ON WIDE RANGE OF GOODS TO CHINA

*CHINA’S HE LIFENG, BESSENT TO MEET IN MALAYSIA OCT. 24-27

Beyond Meat erased a 112% gain yesterday to close down -1%, after a week where its price spiked 1300%. Previously some 64% of the shares available for trading had been sold short as of the end of last month, then on Monday, Roundhill Investments said it added Beyond Meat to its Roundhill Meme Stock ETF, a big sign that meme-stocks had returned. Matt Maley, chief market strategist at Miller Tabak, said it all shows ‘froth in the market is still extremely high’. Retail traders are still pumping meme stocks, oblivious to the growing risks.

*BESSENT: MIGHT SEE CPI COMING DOWN NEXT MONTH, MONTH AFTER

If you are a believer in seasonality, then today is historically the best day to own $SPX for the next 3-months! (@RenMacLLC)………….. however Bank of America Securities said clients resumed selling U.S. stocks last week after briefly “buying the dip,” led by institutional and hedge fund outflows.

Banks warning about private credit quality while funding its growth….

Bank of America warns of forced stocks selling if credit problems persist

WELLS FARGO CEO CHARLIE SCHARF: CREDIT WILL DETERIORATE

*WAL 3Q PROVISION FOR CREDIT LOSSES $80.0M, EST. $42.4M (Chart 2, Bloomberg)

Despite mortgage rates being the lowest level in over a year, mortgage purchase applications FELL to the lowest level since the beginning of August.

OpenAI is now the world’s most valuable private company, valued at $500 billion. This is 3.5 times higher than Spotify’s, market value of $144 billion, and almost equal to Netflix’s.

Bonds continue to tell us risks are rising (Chart 3, @PPGMacro).

Current Drawdowns Bitcoin: -14.3% Gold: -8.4%

Largest Drawdowns Last 10 Years Bitcoin: -84%, -71% and -75% Gold: -21% (Bloomberg data).

Hhhmmmmm….. (Chart 4, LSEG Datastream, Nasdaq, MSCI, S&P, Schroders)

No key data today

Onto flat price action, Brent futures have bounded up on today’s news, throughout the session, hitting fresh highs and trading above $66 post-window. We have now broken this imaginary ceiling that was haunting us since 9 October! Meanwhile, spreads are in happy land too: the prompt Brent spread reached 65c by the close and it has now reached a new high of 75c! In terms of the curve, we’re in backwardation almost throughout the 2026 spreads!

This report reviews the key data from the US EIA’s Weekly Petroleum Status Report

Shall we be worried? The Russia/Ukraine + war is getting worse with more nations being forced to take sides. The scope of Western sanctions keeps on growing and the line seems to be pointing to a wider war. Russian nuclear drills, Tomahawk missiles of mystery origin, wide-reaching sanctions… it feels like things are coming down to the endgame. Lukoil and Rosneft were hit by OFAC last night, as Trump raged about an immediate ceasefire – we wonder which of Trump or Putin would have felt their time was most wasted by a meeting. A dejected Russian source commented “I think all of this is terrible. We are 10 minutes before the Big War ☹”. Even Medvedev said Trump “is now firmly on the warpath against Russia.” We don’t like this road and want to get out of the car before there’s a big smash!

The Dec’25 Brent futures contract gapped up from yesterday’s close of $63.50/bbl to $64.12/bbl at today’s open. Prices have continued rallying, reaching $65.82/bbl at 12:00 BST (time of writing). In the news, US President Trump announced new sanctions on Russian oil giants Lukoil and Rosneft in efforts to tighten Moscow’s revenue for funding its war in Ukraine. The US Treasury has given firms until 21 November to unwind transactions with the Russian producers. According to Reuters, the sanctions followed a Russian nuclear arms training drill and are a deviation from more conciliatory approaches to Ukrainian peacekeeping. Following the sanctions, Reuters has reported that Indian refiners are now poised to cut Russian oil, with privately-owned Reliance Industries planning to halt its imports. Indian state refiners are also reportedly re-examining their trade flows to ensure that no imports will come from Lukoil or Rosneft. In Europe, the EU has formally adopted its 19th package of Russian sanctions, including bans on Russian LNG imports. In an X post, EU foreign policy chief Kaja Kallas said that sanctions also target Russian banks and the movement of Russian diplomats in the EU. Following EU sanctions, suppliers have reportedly cancelled sales to China’s Yulong Petrochemical (capacity 400kb/d), as per a Reuters report; among those suspending sales is BP, TotalEnergies, and Saudi Aramco. This move is likely to increase Chinese purchasing of Russian crude. Finally, at time of writing, the front-month Dec/Jan’26 and 6-month Dec/Jun’26 spreads are at $0.67/bbl and $1.88/bbl, respectively.