Equities and precious metals both fell again (S&P500 -0.5%, Nasdaq -0.9%) as subprime bankruptcies emerge, banks warn about private credit risks, US imposes new sanctions on Russia and Trump threatens new export restrictions on China. I’m trying not to get too bearish but I’m struggling to find any good news, S&P500 and Nasdaq could be forming double tops here, but bonds are clearly telling a bearish market story, the OIS prices 116bp of cuts over the next year.

Gold and silver are now in a short term down trend, don’t listen to me, look at the charts and short-term moving averages. Leveraged positions have taken heavy losses over the last 2 days. ‘When a speculative bubble pops. The really bad losses are taken in the next two months as those who missed it buy the dip’ (Andy Constan @dampedspring)

A growing number of states are struggling, some already in recession, others right on the edge. Together, they account for nearly a third of U.S. GDP. The national economy isn’t there yet, but it’s clearly losing steam. (Chart 1, Mark Zandi, Moody’s Analytics)

Volatility in the AI Revolution is heating up. Quantum stock fell 20% on news of Google’s Willow Chip solving problems 13,000x faster than the best supercomputer using a new algorithm called Quantum Echoes. Then the quantum stocks rallied back 20% after hours on news that the Trump Administration is preparing equity stakes in quantum stocks. It would be unprofessional of me to suggest that they may be trying to prop up another corner of the equity market for another week…… *IONQ, RIGETTI, D-WAVE IN TALKS FOR GOVT. TAKING STAKES: WSJ …. NOTE: These companies trade at 200–900× forward sales — far above dot-com bubble levels. Analysts warn the sector is “disconnected from fundamentals.”

17 years after the financial crisis another subprime lender has gone under. PrimaLend Capital Partners filed for bankruptcy after months of negotiations with creditors, a sign of stress in a sector catering to low-income consumers

IT’S `PARTY LIKE IT’S 1999′ IN CREDIT MARKETS: JIM CHANOS

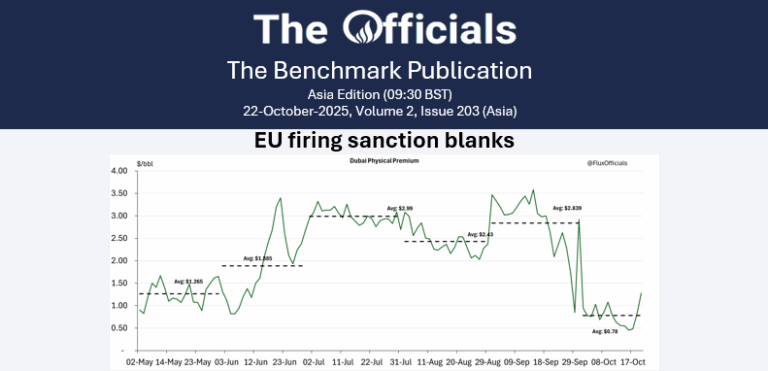

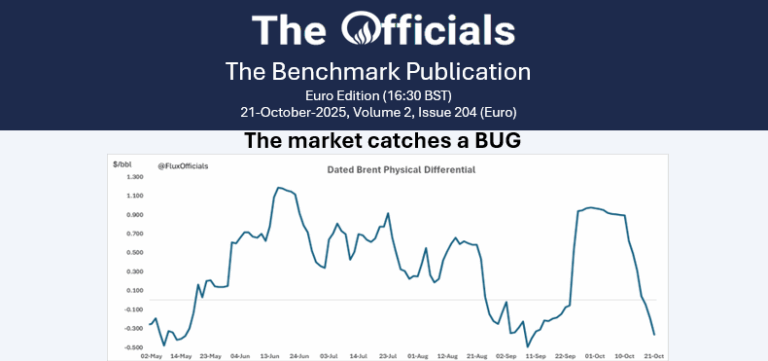

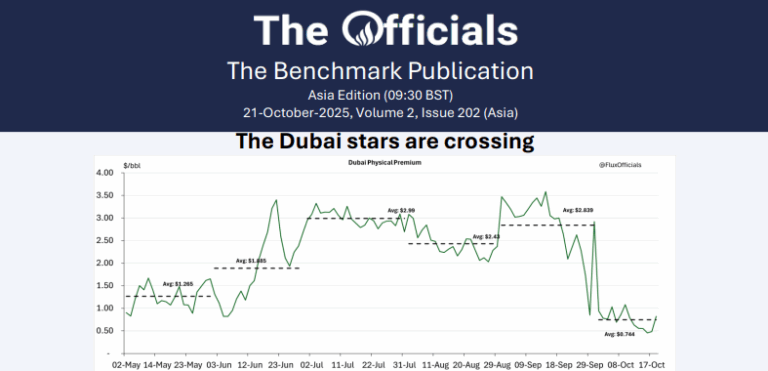

*US TARGETS ROSNEFT, LUKOIL IN LATEST ROUND OF RUSSIA SANCTIONS

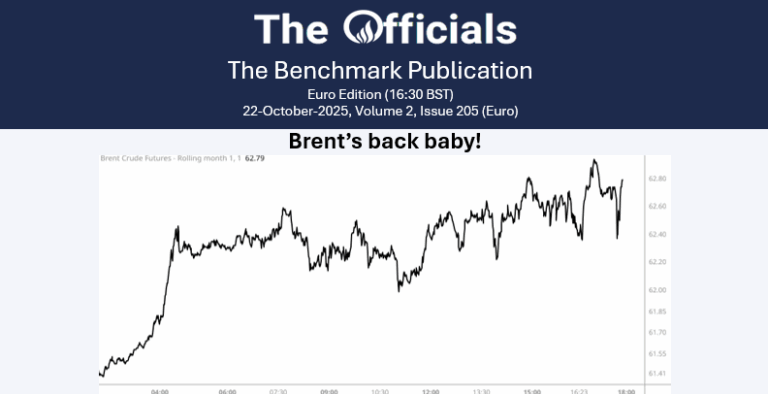

*OIL JUMPS AS MUCH AS 2.5% AT OPEN AS US SANCTIONS RUSSIAN FIRMS

TRUMP ADMINISTRATION CONSIDERING PLAN TO RESTRICT GLOBALLY PRODUCED EXPORTS TO CHINA MADE WITH OR CONTAINING U.S. SOFTWARE; NEW EXPORTS CONTROLS COULD CURB EXPORTS ON WIDE RANGE OF GOODS TO CHINA

*CHINA’S HE LIFENG, BESSENT TO MEET IN MALAYSIA OCT. 24-27

Beyond Meat erased a 112% gain yesterday to close down -1%, after a week where its price spiked 1300%. Previously some 64% of the shares available for trading had been sold short as of the end of last month, then on Monday, Roundhill Investments said it added Beyond Meat to its Roundhill Meme Stock ETF, a big sign that meme-stocks had returned. Matt Maley, chief market strategist at Miller Tabak, said it all shows ‘froth in the market is still extremely high’. Retail traders are still pumping meme stocks, oblivious to the growing risks.

*BESSENT: MIGHT SEE CPI COMING DOWN NEXT MONTH, MONTH AFTER

If you are a believer in seasonality, then today is historically the best day to own $SPX for the next 3-months! (@RenMacLLC)………….. however Bank of America Securities said clients resumed selling U.S. stocks last week after briefly “buying the dip,” led by institutional and hedge fund outflows.

Banks warning about private credit quality while funding its growth….

Bank of America warns of forced stocks selling if credit problems persist

WELLS FARGO CEO CHARLIE SCHARF: CREDIT WILL DETERIORATE

*WAL 3Q PROVISION FOR CREDIT LOSSES $80.0M, EST. $42.4M (Chart 2, Bloomberg)

Despite mortgage rates being the lowest level in over a year, mortgage purchase applications FELL to the lowest level since the beginning of August.

OpenAI is now the world’s most valuable private company, valued at $500 billion. This is 3.5 times higher than Spotify’s, market value of $144 billion, and almost equal to Netflix’s.

Bonds continue to tell us risks are rising (Chart 3, @PPGMacro).

Current Drawdowns Bitcoin: -14.3% Gold: -8.4%

Largest Drawdowns Last 10 Years Bitcoin: -84%, -71% and -75% Gold: -21% (Bloomberg data).

Hhhmmmmm….. (Chart 4, LSEG Datastream, Nasdaq, MSCI, S&P, Schroders)

No key data today