Weekly Oil Inventories Report

This report reviews weekly oil inventory data from the US EIA’s Weekly Petroleum Status Report, Global Insights’ ARA Independent Storage and International Enterprise’s Singapore product storage

This report reviews weekly oil inventory data from the US EIA’s Weekly Petroleum Status Report, Global Insights’ ARA Independent Storage and International Enterprise’s Singapore product storage

Morning Macro Friday 26th September

Trump announces 100% pharma tariffs from 1 October, except for companies building their manufacturing plant in the US. Pharma shares like Astrazeneca and GSK fall around 1%. Trump also revealed tariffs on some very… niche… goods: 50% on kitchen cabinets, bathroom vanities and associated products, 30% on upholstered furniture and 25% on heavy trucks. Bloomberg says these new tariffs could raise average tariff rates by 3.3%.

US economic data revised higher. GDP expanded at a 3.8% annualised pace in Q2, above 3.3% in the previous estimate, to the fastest in nearly two years. This was powered by 2.5% consumer spending and a blistering 7.3% jump in business investment, led by record outlays on intellectual property and data centres – the backbone of the AI boom.

After a tariff-driven contraction in Q1, the economy has snapped back with force. Business spending is surging, households are still buying, and layoffs remain rare. Markets were less impressed – stocks fell and yields eased – but the picture is clear: America’s growth engine is still very much switched on.

Bets on US recession have dropped from a high of over 60% early this year to 6% now on Polymarket. (Figure 1)

Fresh labour market data revealed jobless claims fell to their lowest since mid-July and unemployment claims slipped by 14k to 218k, far below expectations. Most firms are clinging to workers despite slower hiring, keeping the labour market cooler but intact. Markets now pricing less Fed cutting after strong macro prints in the US, with OIS now pricing under 40 bps. They also expect the Fed’s neutral rate – where policy is neither boosting nor slowing growth – to settle near 3%, higher than before.

The repricing briefly lifted 10-year yields to a three-week high near 4.1%. Positioning data shows investors hedging both more aggressive and less aggressive Fed outcomes, with heavy activity in SOFR options targeting small cuts. (Figure 2)

S&P 500 begins to rollover, dropping for 3 straight sessions for the first time since late August. In the week to 17 Sep, equity funds absorbed $68.4bn, the biggest weekly inflow of 2025, with a single S&P 500 ETF taking $30bn. Bond funds added $14.3bn (YTD >$600bn), alternatives gained $8.2bn (crypto $3.8bn), and EM equities drew $7.6bn.

But markets remain confident as investment grade credit spreads are near 27-year lows. (Figure 3) Is default risk low or is the market becoming complacent?

Japanese inflation came in cooler than expected, with Tokyo core CPI came at 2.5% y/y in September, below consensus of 2.8%. The headline figure was steady at 2.5% too, after a downward revision for August.

Data today: PCE, Canada GDP, Christine Lagarde speech

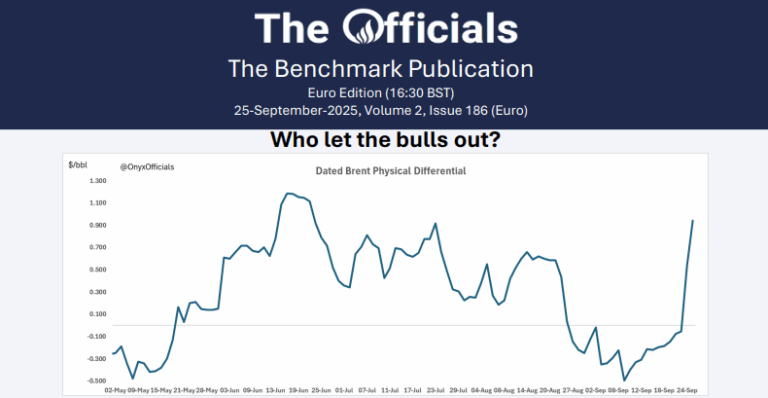

If you thought yesterday was chaos in the North Sea, today’s bonanza shoot the physical to the moon!

From Raging Bull yesterday to Sitting Bull today, as Brent cooled its heels and found support just over $69. It was against Dubai that Brent really showed off, as the October Brent/Dubai swap went on an adventure this morning, surging from -$1.70 in the early trading hours to -$1.41 by the Asian close, and peaking at -$1.30 shortly after! Brent was doing the heavy lifting while Dubai was chilling.

The Nov’25 Brent Futures contract fell from $69.24/bbl at 07:53 BST to $68.60/bbl at 09:56 BST. Prices have since rallied back up to $69.09/bbl at 11:20 BST (time of writing). In the news, seven indigenous communities in Ecuador’s Amazon are opposing the government’s plan to open 49 oil and gas blocks, citing violations of constitutional rights and lack of prior consent. The $47 Bn initiative aims to modernise the oil sector and attract foreign investment, but critics argue it threatens ancestral lands and breaches legal protections. Ecuador, heavily reliant on oil exports, is seeking to reverse declining output, around 464 kb/d in 2024, amid frequent pipeline disruptions. In other news, eight oil companies operating in Iraq’s Kurdistan region have reached a preliminary agreement with the federal and regional governments to restart crude exports, which have been suspended since early 2023 due to a dispute with Turkey. The deal, covering 90% of the region’s production, could resume flows “in the coming days,” though two companies, Norway’s DNO and Britain’s Genel Energy, have withheld signatures, demanding payment guarantees for $1 Bn in unpaid royalties. Exports are expected to resume at a reduced rate of 230 kb/d, down from the previous 400 kb/d. Russia plans to begin natural gas production at the Sakhalin-3 project in 2028, aiming to supply both China and domestic markets, according to Sakhalin’s governor. Gazprom and local authorities are also planning a new refinery in southern Sakhalin to process gas condensate into jet fuel, diesel, and naphtha. The move is part of Russia’s broader shift toward Asian energy markets amid ongoing tensions with the West. Finally, the front-month Nov/Dec spread is at $0.83/bbl and the 6-month Nov/May spread is at $2.23/bbl.

This week, we anticipate money managers to trim their length in Brent and gasoil futures. In contrast, we expect speculative length to increase in RBOB futures, as a reflection of supply tightness concerns in the Atlantic Basin. We expect a risk-on week for physical players in Brent and gasoil, but a risk-off week in RBOB.

Morning Macro 25th September

Overnight we saw US equities and gold take a breather as US yields and the US dollar still edge higher from last weeks ‘less dovish’ Fed meeting and stronger housing data with August New Home Sales surging 20.50% to the highest level since Jan 2022, amid lower mortgage rates and builder incentives. The standout price move is copper, jumping 3.8% this morning. Freeport has declared force majeure at its Grasberg mine in Indonesia one of the largest mines on earth, producing ~1.7bn pounds of copper (nearly 3% of global supply)

U.S. AUGUST NEW HOME SALES SOAR 20.5% M/M TO 800,000; EST. 650,000; PREV. 664,000

Even with that There were 35% more home sellers than buyers in the US in August, the second-largest reading on record after 36% in June. The estimated number of sellers reached 1,943,957 in August, one of the largest readings since 2020. (Chart 1, Redfin, MLS)

Gold hits most overbought level on the monthly chart in 45 years. But beware, its simply trending higher, an asset can stay overbought during a long period of times in a bull run, and it’s currently trending higher with retail and trend following algos happily buying. But also note, of course central banks are buying, and they will simply add on pull backs (not stop out) and the market isn’t speculating; it’s rationally repricing the metal for a new era of fiscal dominance, negative real yields, and de-dollarization.

Meanwhile in equity space five U.S. companies now make up 20% of the world’s total stock market value, and recent action has been wild: “non-profitable tech” up 8% in five days, “Most-shorted” stocks up 6.7%, and a quantum-computing theme fund up 30%. And The S&P 500 has gone 107 sessions without a drop of 2% or more, the longest streak in more than a year. Profit less tech has performed particularly well over the last 2 months (Chart 2, Bloomberg, @HayekAndKeynes)

Foreign investors now have a record allocation to U.S. equities (Chart 3, @NDR_research)

German IFO services expectations remain in contraction and trending lower. (Chart 3, Macrobond & Nordea)

Seasonal retail hiring to fall to lowest level since 2009, signaling trouble for holidays, report says – CNBC

BESSENT: POWELL SHOULD HAVE SIGNALLED 100-150 BPS CUT…… shrug!

Data today – weekly jobless claims

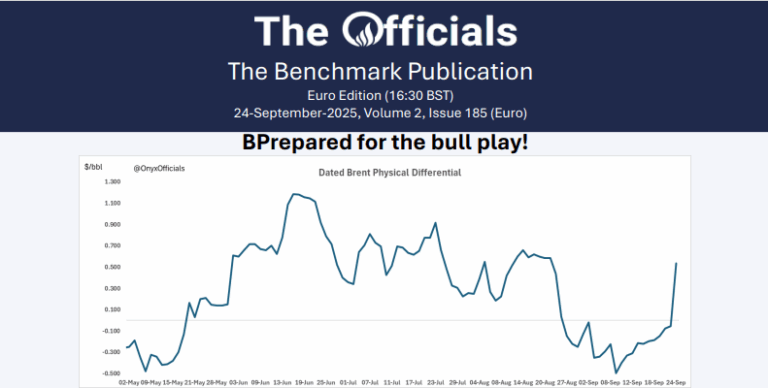

Wow, what a crazy session in the North Sea, the title gives some of the juice away!

This report reviews the key data from the US EIA’s Weekly Petroleum Status Report

What a wacky window! Or wacky players…buyers were avoiding certain sellers like the plague. And sellers avoiding buyers. Somebody please bring some order to the nonsense! Unless our eyes and ears deceive us, NPI was happily bidding at $69.89, but the sellers Mercuria and Reliance gave them the cold shoulder, entering their own offers below that and hitting lower bids from the likes of Vitol. A study in careful avoidance. Market crosses or wide bid/offers are the death of markets. But hey, the liquidity in Dubai is enormous, with players telling us that the Oct/Nov Dubai spread had a record yesterday.

The front-month (Nov’25) Brent futures contract saw more support this morning and tested the $68/bbl handle thrice this morning, finally succeeding after 10:50 BST and reaching $68.30/bbl at 11:33 BST (time of writing).

Morning Macro 24th September

Equities finally fell from all-time highs as the Fed Chair Powell raised concerns about the U.S. employment situation, inflation and equity market levels.

Powell: job creation has dropped very sharply

Powell: tariff increases will likely show up as somewhat higher inflation over several quarters

Powell: recent price increases largely reflect tariffs

Powell says the stock market is “fairly highly valued.”

Developed countries PMIs mostly softened in August consistent with moderate economic growth. Europe was flat but Australia, Japan, the UK and the US all slowed. Input prices rose but output prices fell slightly.

Goldman Sachs and Deutsche Bank add to the growing Nvidia bubble call….

Goldman’s head of Delta One slams Nvidia’s increasingly grotesque vendor financing circle jerk “… definitely not old enough to have been around trading during the tech bubble and let’s level set, multiples are now where near that point in time. That said, vendor financing was a feature of that era and when the telecom equipment makers (Cisco, Lucent, Nortel, etc.) extended loans, equity investments, or credit guarantees to their customers who then used the cash/credit to buy back the equipment…well suffice it to say, it did not end well for anyone.” – Rich Privorotsky “It may not be an exaggeration to write that NVIDIA – the key supplier of capital goods for the AI investment cycle – is currently carrying the weight of US economic growth.” -DB’s George Saravelos

Boiling frog syndrome, EURUSD mind the gap! (Chart 2, @PPGMacro)

Lithium Americas stock, surges +90% on reports that the U.S. government is seeking to buy up to a 10% equity stake in the company. I wonder who got to front run that trade!

Platinum also jumped 5.7% overnight

With Argentinian Peso -20% in three months US Treasury Secretary Scott Bessent’s pledged on Monday to provide ‘all options for stabilisation’ to Argentina is such a significant move to bring the crisis-prone economy back from a dangerous volatility spiral.

Data today – US new home sales, German IFO

In this podcast, our Onyx Commodities Head of Trading Desks discuss the latest trends and developments in the oil, gas, power and carbon markets in which Onyx Commodities trades. This episode was recorded on Tuesday, 17 September 2025, at 11:30 a.m. London time. Please listen to the end of this podcast for important disclaimers.

This communication is for informational purposes only and based on the information available at the time the podcast was recorded. This is not an offer to buy or sell, nor a solicitation, and no recommendations are implied. It does not consider your financial circumstances or objectives and may not be suitable for you. Copyright 2025, Onyx Capital Group – all rights reserved.

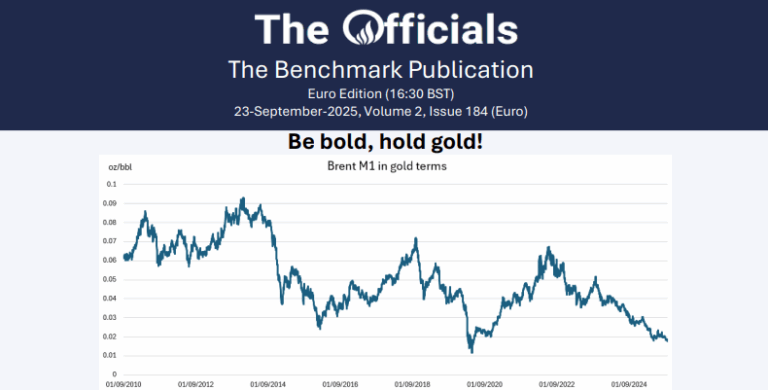

Dollar debasement is the name of the game, seemingly, for this administration. Self-sabotaging policy has driven markets into deep disillusion with the global reserve currency, seeing an increasing rotation to gold. Spot gold is up over 42% to almost $3.8k/oz today! In dollar terms, oil is down from around $80/bbl at the start of 2015 to the upper $60s range today. But, in gold terms, the fall has been dizzying…

This report aims to provide a position index for energy futures between -50 and 50, with 0 as the neutral position. The full methodology is at the back of the report. When the position index is at the extremes, above 40 or below -40, the market is overstretched relative to its average position in the previous 3-year rolling window. As such, it is ripe for mean reversion. Consequently, when the index is high, deleveraging will follow, having a negative impact on price, while when the index is low, we expect accumulation that will push the price higher.