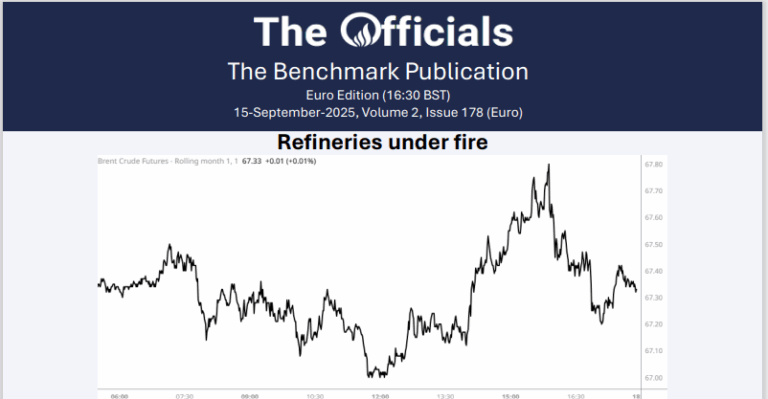

Overnight & Singapore Window: Brent support at $67.00/bbl

This morning, the Nov’25 Brent Futures contract softened from around $67.50/bbl, overnight, to reach $67.00/bbl at 10.08 BST, inching back up to $67.30/bbl at the time of writing at 11.24 BST. Progress on the India-US trade deal front largely hinges on Washington rolling back the Russian oil-linked additional 25% duty on India, and no breakthrough is likely without it, India-based trade-focused think tank Global Trade Research Initiative (GTRI) has argued, as talks between the countries start today. The Ksi Lisims LNG project has won provincial and federal environmental approval, with strict conditions to protect ecosystems. Backed by the Nisga’a Nation, it plans a floating facility producing 12 million mt of LNG annually, focusing on Asian markets. If built, it would be Canada’s second LNG project in a decade, alongside the Canada LNG expansion at Kitimat, expected to double capacity to 14 million mt and generate $44 Bn. South Africa has granted BP, Vitol, and other oil traders 25-year leases at Durban’s Island View Precinct, ending years of disputes over short-term deals that threatened investment and fuel security. The hub handles about 70% of the country’s fuel imports. Questions remain over the future of the Sapref refinery under the Central Energy Fund. Dragon Oil, owned by Enoc, has signed a $30 million agreement with Egypt’s EGPC to boost exploration and production in the Gulf of Suez, including drilling at least two new wells in East El-Hamd. It follows Egypt’s recent signing of three oil and gas exploration deals worth over $121 million with Parenco, Dragon Oil, and Apache across the Western Desert, Gulf of Suez, and North Sinai. Finally, the front-month Nov/Dec and the 6-month Nov/May spreads are at $0.36/bbl and $1.16/bbl, respectively.