Alpha Report: Bullish Undertones

Another week brings another selection of new trade ideas from Flux Insights. This week, we look at trades in Gasoline and Crude.

Another week brings another selection of new trade ideas from Flux Insights. This week, we look at trades in Gasoline and Crude.

ICE COT data for the week ending 04 Nov shows open interest falling for the second week, by over 75.8mb w/w (marking a 2.2% drop w/w). This suggests the market is still adjusting to the news from last week, with prod/merc players removing both long and short positions, which suggests they anticipate risk. This risk-off attitude was mirrored by swap players. Money managers saw a small net drop of 6.27mb (-2.09% w/w) in overall length. Short positions continued to see more substantial w/w changes, with a 14.86mb (+11.85%) addition to their length after seeing a significant 65.26mb (+23.4%) increase in the week prior. The past three weeks have seen short position changes of +31%, -34% and +12%, compared to far smaller weekly changes from long positions. This suggests that short positions were overextended and are now trending back to being normalised, after dropping to extremely low levels with a fund net positioning of just +52mb in the week to 21 Oct.

Shutdown is close to an end, but the wave of the polar freeze is with us now. Meanwhile, China waived the port fees for a year! Read for more at The Officials!

The Jan’26 Brent futures contract traded relatively flat this morning, from $64.22/bbl at 06:00 GMT to $64.04/bbl at 10:30 GMT (time of writing). In the news, Reuters has reported that Indian state refiners HPCL and MRPL have purchased 5mb of US WTI crude and Abu Dhabi’s Murban crude for January delivery. Elsewhere, the US Senate has passed a funding agreement that could potentially end the federal government shutdown. The package comprises three long-term spending bills and ensures that Democrats will have a vote on prolonging health insurance tax credits. In other news, China’s PetroChina will shut its entire Yunnan petrochemical plant (capacity 92mb/y) for maintenance from 15 November to 15 January, per a company statement. In Russia, local task forces have reported that four Ukrainian drone boats have been destroyed near the Black Sea port of Tuapse. According to Reuters, ship-tracking data shows that the port has suspended fuel exports; Russian railways has said that it will extend cargo delivery restrictions towards the port until 13 November. Finally, at time of writing, the front-month Jan/Feb’26 and 6-month Jan/Jul’26 spreads are at $0.24/bbl and $0.41/bbl, respectively.

A breakthrough as progress is made towards ending the government shutdown, while Trump proposes US $2,000 ‘tariff dividend’ for up to 85% of the population. A reopening would resume key data releases and return focus to the deteriorating US fiscal outlook, with rising spending increasingly funded by additional borrowing. With last week’s dismal election performance and his disastrous ratings the $2,000 dividend would clearly help Trump’s ratings temporarily and the weakening economy but $400 billion in stimulus payments will also support inflation, support equities, support gold, weaken long end bonds on debt concerns and reduce expected Fed cuts.

Unsurprisingly gold is up 2% today, Nasdaq +1.2%, US 30-year yields up 5basis points and the dollar lower. Chart 1, Gold resumes its uptrend, Bloomberg). Paul Tudor Jones “all roads lead to inflation”.

Chart 2, US National debt, US Tsy Dept, @Kobeissi Letter, WolfStreet.com))

Borrowing for AI data centre building (Chart 3, BofAGlobal research) and we wonder how OpenAI will fund its $1.4 trillion spending commitments. Hartnett: The AI Bubble “Watch Out” Metric Just Snapped

Financial Times “US companies’ earnings are growing at the fastest pace in four years…

Median earnings growth year-on-year across the Russell 3000 index — a benchmark for the entire US stock market — hit 11 per cent in the third quarter, up from 6 per cent in the previous three months, according to Morgan Stanley. That is the fastest growth rate since the third quarter of 2021.”

US layoffs are spiking. US-based employers announced 153,074 job cuts in October, the highest for any October since 2003. This even exceeds the pace seen during the Financial Crisis. Year to date, over 1 MILLION layoffs have been announced. (Chart 4, Challenger, Gray & Christmas)

US consumer sentiment fell to 50.3 points in October, the 2nd-lowest EVER. It’s now ~10 points BELOW the Great Financial Crisis low and below all recessions. (Chart 5, Uni of Michigan Consumer Sentiment, @GlobalMktObserv)

COMMERCIAL MORTGAGE-BACKED SECURITIES JUST HIT THE HIGHEST DELINQUENCY RATE IN HISTORY.

Data this week

Tuesday – UK BRC retail sales and employment data, German ZEW, US ADP & NFIB Small Business Index data

Wednesday – German inflation, OPEC Monthly Report

Thursday – UK GDP & IP, Aussie employment, Federal Budget Balance data

Friday – French inflation, US PPI

9 Fed Speaker Events This Week

An end to the paralysis? Or just sticking a band aid over an amputation? US Senate Majority Leader Thune is apparently ready to ‘adjust’ the expiration date on the already passed funding bill. Just resurrect a failed compromise to kick the can down the road…

This report reviews weekly oil inventory data from the US EIA’s Weekly Petroleum Status Report, Global Insights’ ARA Independent Storage and International Enterprise’s Singapore product storage

Going against the tide was never going to be easy… Gunvor charged like a bear, eager to gobble up Lukoil’s foreign assets, seeming quite the cup. Bears get very hungry prior to winter. But the US isn’t happy! No food for you, they said. The US Treasury called Gunvor “the Kremlin’s puppet” and won’t back its purchase. Suitably chastised, Gunvor abandoned its bid, though denied being controlled by strings from afar.

The Jan’26 Brent Futures rallied from $63.82/bbl at 08:30 GMT to $64.37 at 10:17 GMT. Prices then fell to $64.13/bbl at 10:33 GMT (time of writing). In the news, Gunvor has withdrawn its $22 Bn bid for Lukoil’s international business after the US Treasury labelled the trader a Russian “puppet” and signalled it would not grant a license, citing the need to end the war immediately. CEO Torbjorn Tornqvist has denied any buyback clause for Lukoil and warned that without timely regulatory approval, US sanctions taking effect on November 21 could disrupt fuel supply in Central and Eastern Europe. In other news, Japan plans to purchase LNG monthly for its emergency reserves starting January, shifting from buying only during peak demand periods to better guard against supply shocks. The Ministry of Economy, Trade and Industry (METI) will ensure at least one LNG cargo, about 70 kt, is secured each month, increasing the annual reserve to 840 kt from roughly 210 kt in recent years. This move responds to calls for an expanded strategic buffer to mitigate disruptions from conflicts or nuclear outages. EOG Resources exceeded Reuters estimates in Q3 due to higher production despite a 13% drop in Brent crude prices y/y. Production rose to 1.3 mb/d, supported by expansion in the Utica and Marcellus regions after its $5.6 Bn Encino Acquisition Partners deal. The company expects Q4 production between 1.35 and 1.39 mb/d. EOG posted an adjusted profit of $2.71 per share, beating the $2.43 average forecast. Finally, the front-month Jan/Feb’26 spread is at $0.34/bbl and the 6-month Jan/Jul’26 spread is at $0.71/bbl.

Breaking: The US is set to ban Nvidia’s scaled-down AI chips from being sold to China! Washington’s move targets B30A chips – used to train large language models when efficiently arranged in large clusters – designed to bypass earlier sanctions. But this would create a big opportunity for China to build its own chips domestically, as Nvidia CEO Jensen Huang warned: “China is going to win the AI race.”

Equities are having a rough time. The S&P 500 dropped more than 1.1% and Nasdaq 1.7% yesterday, with futures consolidating this morning. Big tech stocks suffered with Amazon down 2.8%, Nvidia down 3.6% , Microsoft down 2%, Palantir tumbled 6.8%! Meta is now down over 22% from its August high!

China’s exports unexpectedly fell 1.1% y/y in October, the first drop in eight months, as a sharp 25% slump in shipments to the US outweighed gains elsewhere. The decline, driven by weakening global demand and fading export resilience, signals mounting pressure on China’s slowing economy amid weak consumption and a prolonged property slump – a triple whammy to growth. Meanwhile, modest tariff relief from the US may offer only limited support. Exports still exceeded $3 trillion year-to-date, though momentum is fading.

The Bank of England held rates stable at 4% – as expected – before the Nov 26 budget announcement; however the committee was split 5-4. The OIS market is now pricing over 70% chance for a cut in the December meeting, while its fully expecting a cut in the Early February meeting.

US travel stocks are in focus after upbeat updates from Expedia and Airbnb. Expedia lifted its full-year outlook on resilient holiday demand, with shares up 18%, while Airbnb forecast strong Q4 bookings, rising 5.5%. UK-listed IAG reported Q3 revenue and profit slightly below estimates but noted solid travel demand and strong Q4 bookings despite some North American softness.

European peers didn’t face the same fate with Air France down almost 15% on the day, even despite good earnings!

Japanese household spending rose 1.8% y/y in September, missing expectations of 2.5% and slowing from August’s 2.3%. The data point to a steady yet fragile recovery in consumer demand, with weaker spending on essentials like food, housing, and utilities offset by gains in medical care and household items. On a monthly basis, personal spending fell by 0.7% – marking the first fall since June.

Data today – US Michigan Consumer Expectations, Canada Employment

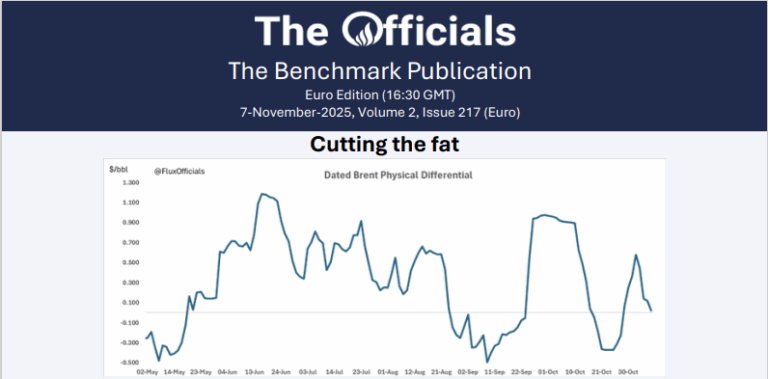

The North Sea is flipping and flopping between being driven by buyers and sellers in a pattern as decipherable as Trump’s moods. It leapt in late September, flattened for a while, dumped hard in mid-October and rebounded in the late month sessions.

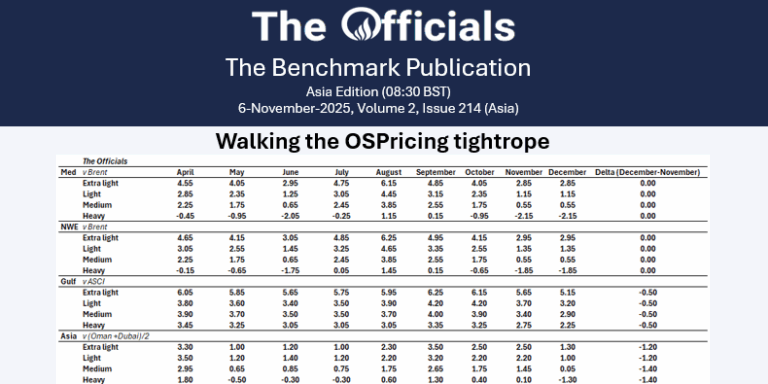

The Saudis cut the highly anticipated OSPs for Asia by $1.20 for Extra Light and Light grades, and for Medium and Heavy by $1.40. They held OSPs to Europe (both NWE and Med) unchanged but cut across the board by 50c for the US Gulf.

The Jan’26 Brent Futures contract rallied this morning to $64.33 at 09:30 GMT before softening to $63.88/bbl ay 10:30 GMT (time of writing). In the news, India’s Reliance Industries is attempting to re-sell some Middle Eastern crude oil it recently purchased to replace Russian supplies affected by new US sanctions, according to trade sources. The firm, which has a long-term agreement with Rosneft for 500 kb/d, said it would comply with Western sanctions while maintaining relationships with other oil partners. While Reliance is estimated to have bought as much as 16 mb of spot crude in total, it has begun offering part of these volumes for re-sale, including 1 mb of Basrah Medium sold to a Greek refiner at a profit. In other news, ExxonMobil has signed an agreement with Energean and Helleniq Energy to explore for natural gas offshore western Greece. The project covers Block 2 and could see first gas production in the early 2030s if exploration and testing prove successful. The investment is expected to range between $50 – 100 million. ExxonMobil will hold a 60% stake and assume the role of operator should test drilling confirm viable gas reserves. A fire at the Naftan oil refinery in northern Belarus was extinguished without injuries, the emergency ministry said. The state Belta news agency reported it was caused by an incident involving diesel fuel at a technological unit. The Novopolotsk refinery processes over 200kb/d. Finally, the front-month Jan/Feb and 6-month Jan/Jul spreads are at $0.23/bbl and $0.33/bbl respectively.

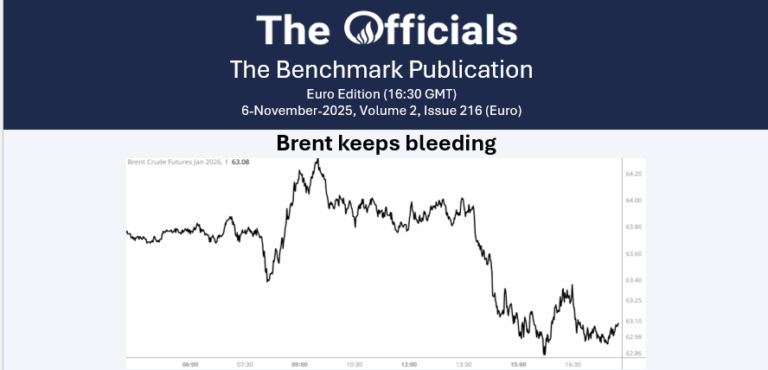

In the week ending 4 Nov, the M1 Brent futures contract traded relatively rangebound between lows of $64.05/bbl (29 Oct) and highs of $65.30/bbl (4 Nov). Over the weekend, OPEC+ announced a modest output increase of 137kb, along with a pause in output increases for Q1’26, contributing to directionless prices this week. The LS gasoil swap crack also saw inconsistency, falling from $31.40/bbl on 28 Oct to $28.55/bbl on 29 Oct. Prices then met support here, recovering to the $31/bbl handle on 30 Oct before reversing and falling to $28.25/bbl on 04 Nov. RBOB prices saw consistent strength this week, rising from $12.80/bbl on 28 Oct to $14.55/bbl on 03 Nov.

This week money managers are anticipated to be risk off in Brent and RBOB, trimming longs in the former and adding to shorts in the latter. In contrast, these players are expected to be risk on in gasoil by adding to their longs.

Further detailed information on other categories and contracts can be found in the report.

Morning Macro 6th November:

We are officially in the longest US shutdown in history – consensus estimates are that shutdown would cost the economy around $15 billion each week; we have now entered the 6th week of the shutdown! Meanwhile, the US Department of Transportation announces mandatory flight cuts at major airports from Friday. The US may cut air traffic by 10% if no deal is reached to end the shutdown.

The US Supreme Court heard arguments this week on the legality of Trump’s sweeping tariffs, and many justices looked sceptical. Polymarket is now pricing only a 30% chance of the Court ruling in favour of Trump! If the tariffs are ruled out, this would cost the US around $30 billion per month in lost revenue!

But elsewhere the party is still going – the question is how long until the music stops? Globally the proportion of stock indexes at an all-time high is the highest since 1999! (Graph 1, Macrobond)

Now with lacking data in the US, everyone’s attention was on the ADP employment data, which showed that in October, private sector employment rose by 42k, marking the first monthly gain since July and surpassing expectations of 25k. Despite the positive data, US treasury yields didn’t even flinch, showing the little importance ADP data have in the market.

In the Eurozone, PMI data were positive for Spain (56) and Italy (53.1), recording their strongest expansions in over a year, driven by resilient services, new orders, and easing cost pressures. Germany (53.9) showed its fastest growth since mid-2023, supported by a rebound in services despite softer sentiment. Meanwhile France (47.7) remained mired in contraction, reflecting weak domestic demand. Overall, Europe’s private sector recovery is being powered by services strength amid lingering manufacturing weakness. Outside continental Europe, the UK (52.2) also regained momentum, but the expansion was driven by the services sector as the manufacturing side remains in contraction!

And the US showed steady growth on the PMI front too; the S&P Composite PMI rose to 54.6, driven by solid gains in both manufacturing and services activity. New business strengthened and employment edged higher, though confidence slipped to a six-month low. Inflation pressures continued to ease, with costs and prices rising at their slowest pace since April. Meanwhile, the ISM Services PMI climbed to 52.4, signalling the strongest expansion since February. Business activity and new orders rebounded sharply, though employment remained weak amid uncertainty linked to the shutdown.

Data today – Bank of England interest rate decision