Morning Macro 31st October

In central banking, following the Fed, the BoJ and the ECB held their policy rates steady at 0.5% and 2%, respectively.

The Euro Area expanded just 0.2% q/q. The third largest economic area is struggling to make meaningful progress! Germany and Italy stagnated, Ireland, Finland and Lithuania contracted, while the growth was led by Spain (0.6%) and, surprisingly France (0.5%) due to a sharp rise in exports. Unemployment held steady at 6.3%, consumer confidence and services sentiment were up, while inflation expectations edged down. Inflation is due to be out today and if the deflation worries continue the ECB will have to cut sooner than expected. The OIS over the next year is pricing below 12 bps – so it shouldn’t come as a surprise if the euro weakens form its current levels (Chart 1, Bloomberg).

The 31st day of the US government shutdown! Earlier estimates had shown that every week could shave off 0.1% from the GDP, so now we are talking about at least 0.4% less for Q4 2025. Speaking of GDP, yesterday’s Q3 GDP wasn’t released, something that makes the job for the Fed even harder.

In Japan unemployment rate picked up to 2.6% and the labour force participation continued declining! Inflation came really hot at 2.8% – above expectations – the markets are slowly ramping up their bets for another hike by the BoJ. Expect the gap on Chart 2, Bloomberg to tighten as the interest rate differential (white line) remains well below historical levels, while the USD/JPY should weaken with monetary tightening. But housing starts and construction orders in Japan remain an issue!

Meanwhile, Chinese PMIs surprised to the downside – with the manufacturing sector contracting (49), while non-manufacturing edged up to 50.1.

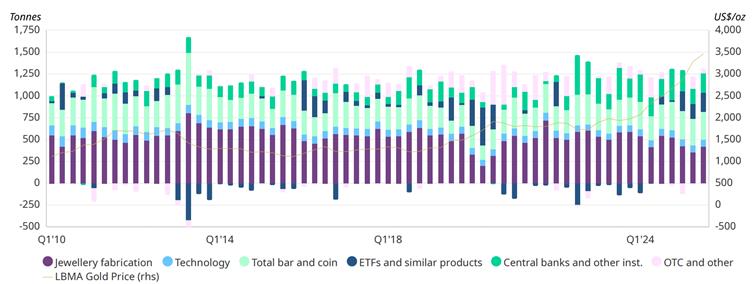

Gold demand hit a record 1,313 t in Q3 (+3% y/y), worth $146 bn (+44%), as investors added 222t and central banks holdings were up 28% q/q, while jewellery slumped. Supply also hit records, with mine output up 2%, as gold averaged $3,456/oz (Chart 3, World Gold Council).

The Fed cut rates by 25 bps, but the front end didn’t get the memo – the SOFR rate fixed at 4.27%. Heavy T-bill settlements ($83B this week), month-end balance sheet constraints, and Canada’s fiscal year-end squeezed liquidity. Interest on Reserve Balances – the rate at which banks deposit at the Fed – was at 3.9%, when the spread between the IORB and SOFR is that wide, it screams cash demand is high!

France’s CAC 40 fell 1% as markets soured over a provisional 33% tax on share buybacks passed in a parliamentary vote – a move investors fear will hammer large French firms. SocGen dropped over 5% as traders cut buyback expectations. If the tax is upheld in the final budget, it could undermine Paris as a financial hub and push companies to list abroad. The proposal effectively kills the appeal of buybacks, wiping out a key shareholder-return tool.

Data today – Euro Area inflation, Canada GDP, Fed Governors speeches