Morning Macro 4th December

Copper makes another new all-time high as the dollar trends lower (unable to break the magic 100 level Chart 1, Bloomberg) on news ultra dove, Trump puppet Hassett is the likely new Fed chair and ADP payrolls come in significantly weaker than expected. In Japan 10-year JGB’s rise another 4bp, highest since 2008.

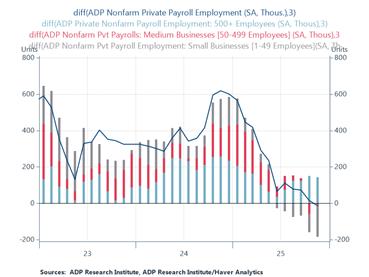

The ADP report for November shows the largest monthly job losses (32,000) since early 2023, undershooting the consensus forecast gain of +10,000 jobs. Notable distribution: Small firms are the ones shedding workers, according to the latest ADP. Over the last three months, small businesses have cut 178,000 off their payroll ranks. By contrast, large firms have added 143,000. (Chart 2, @RenMacLLC)

The ISM Services PMI rose 0.2 points to 52.6, beating expectations by 0.5 points and marking the ninth consecutive month of sector expansion in 2025. The index now sits 0.9 points above its 12-month average of 51.7, indicating steady, modest growth. Business Activity (54.5%) and New Orders (52.9%) remained firmly in expansion territory, while Employment (48.9%) continued to contract for a sixth straight month. The Prices Index eased to 65.4%, down 4.6 points from October, signalling ongoing but moderating inflationary pressure.

TRUMP: “I guess a potential Fed Chair is here too…I don’t know, are we allowed to say that? Thank you, Kevin.” Kevin Hassett has consistently called for lower interest rates to stimulate economic growth and criticized the Federal Reserve for being too slow to ease monetary policy.

The S&P 500’s 5-day historical range is now 1.2%, the lowest level of the year. Markets are quiet after Thanksgiving but plenty of event risk ahead with Fed, BOE and BOJ rate meetings all pricing moves (cut, cut, hike) plus a resumption of key US payroll data, and the expected Santa Claus rally. All in low volume.

$IBM CEO says that at today’s costs it takes about $80B to build & fill a 1 GW AI data centre, so the ~100 GW of announced capacity implies roughly $8T of capex & “no way you’re going to get a return on that,” since you’d need “about $800B of profit just to pay for the interest” (Charles-Henry Monchau)

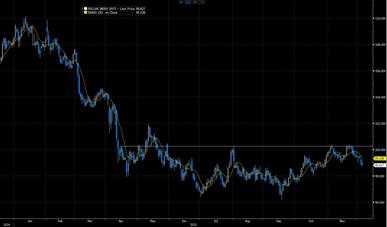

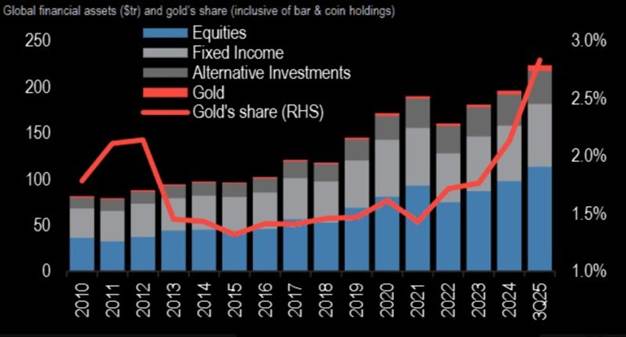

Gold is a mere 2.8% of investors AUM (Chart 3, The Market Ear, Charles-Henry Manchau)

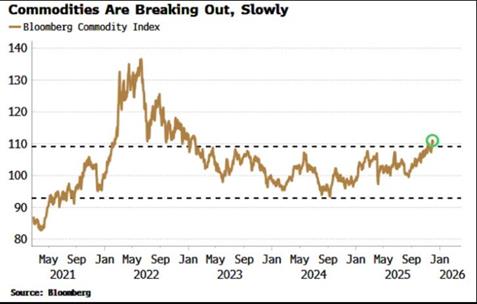

Commodities are breaking out slowly (Chart 4, Bloomberg)

The Australian OIS is pricing one full HIKE over the next 12 months. AUDUSD up 2.5% over the last 2 weeks.

Here’s the cumulative real GDP growth for Europe’s four biggest economies since Q1 2020: 9%, 7.5%, 6.2%, 2.1%…. trending!

Another shocking stat of the day: Interest costs on US debt are now equal to 24% of every $1 in government tax revenue. The interest expense as % of collected taxes has nearly DOUBLED over the last 4 years.

Data today – EZ retail sales, US weekly jobless claims