Morning Macro 1st December

Last week saw one of the strongest weekly cross asset rallies of the year, but this week has started more abruptly to the downside. The catalyst is the surge in Japanese yields 2yr up 5.5bp (that’s 5.5%, a huge rates move) and above 1% for the first time since 2008. Also, the 10-yr yield rose +7bp (4% move), Nikkei is off 2%, Nasdaq futures -0.9%, and Bitcoin -4.4%.

The impact of tariffs can be seen in the Black Friday data, according to Salesforce. Average selling prices were up 7% y/y, while order volumes were down 1% y/y.

Japan’s Finance Minister says it is “clear” the yen swings aren’t “moving based on fundamentals” Bloomberg.

Silver breaks to new all-time highs. YTD Silver +97%, Bitcoin -6.5%.

French PPI -0.8% YoY (prior +0.1%)

German unemployment 6.3% (prior 6.3%)

Intel jumps 10% on Friday on NO new news. Rumour has it Google will produce its TPU’s in US in partnership with Intel. (a huge blow to Nvidia).

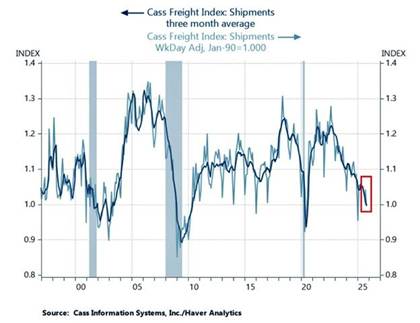

October 2025: The Cass Freight Shipments Index falls 7.8% year over year. The lowest October reading since the depths of the 2009 financial crisis.

Data this week

Monday – EZ, UK, US mfg PMI,

Tuesday – EZ CPI & unemployment

Wednesday – EZ, UK, US services PMI, US ADP, Aussie GDP

Thursday – EZ Retail sales, US jobless claims

Friday – EZ GDP< Canada employment, US PCE deflator and UMich sentiment