Morning Macro September 12th

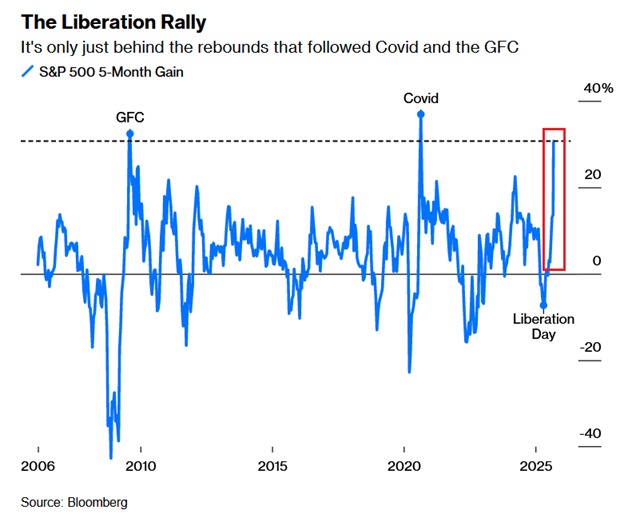

The S&P 500 closed at a new all-time high and is now up +36% since the April 2025 bottom. That’s +$15 TRILLION in market cap in 5 months. This is the most since the COVID recovery and 1% point less than the Great Financial Crisis recovery. (Chart 1, Bloomberg)

Yesterday’s CPI data from the US showed inflation broadly in line with forecasts: headline CPI rose 2.9% y/y and the core measure held at 3.1%. On a m/m basis, inflation rose 0.4% as shelter, food and gasoline prices were up m/m. Although the yearly measure showed steady core inflation, the monthly counterpart picked up, boosted by increased airline fares and used car prices.

And the initial jobless claims for the week ending 5 September jumped to 263k, the highest in four years and well above consensus at 235k. The four-week moving average surged by almost 10k to 240.5k, the steepest increase since December 2020! Meanwhile, unemployment claims came lower than expected at 1.932 million in the last week of August. Rising layoffs, fewer new jobs, yet fewer people claiming benefits – that points to a contracting labour force!

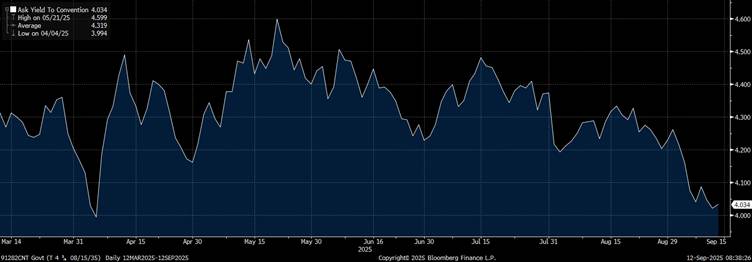

Treasuries welcomed the weakness, with the 10-year yield sliding to 4%, its lowest in 5 months (Graph 2, Bloomberg). The OIS market raised the stakes, now expecting a cut at each of the next two Fed meetings and over an 87% probability of a third cut by year end! While the DXY fell from above 98 to 97.50 this morning.

Economic activity in New Jersey, Illinois, Virginia, Georgia, Washington, Iowa, and Oregon is contracting, this comes as goods-producing sectors like agriculture, manufacturing, and construction are already in recession. But California, Texas, and New York are expanding and together make up for nearly one-third of US GDP, as healthcare real estate and technology are booming. And now tech stocks reflect a record 37% of the total US stock market, exceeding the 2000 Dot-Com Bubble peak by 4 percentage points!

In the UK, things aren’t progressing as the economy stalled in July after June’s 0.4% growth, as gains in services (+0.1%) and construction (+0.2%) were offset by a sharp 0.9% fall in production. Manufacturing slumped 1.3%, led by steep drops in electronics and pharmaceuticals. Over the three months to July, GDP rose 0.2%, while annual growth held at 1.4% – slightly missing the forecasts.

Following the ECB’s decision to leave the main refinancing rate at 2.15%, French inflation eased to 0.9% in August from 1% in July, as services price growth slowed and manufactured goods prices fell further, alongside energy prices. On a monthly basis, CPI rose 0.4%, driven by a rebound in clothing and footwear after summer sales. While Spain’s inflation held at a five-month high of 2.7% in August, transport costs accelerated but were offset by softer food inflation. Core inflation edged up to 2.4%, its highest in four months.

Data today – Michigan consumer data, India inflation rate, Chinese loan growth