Morning Macro 27th October

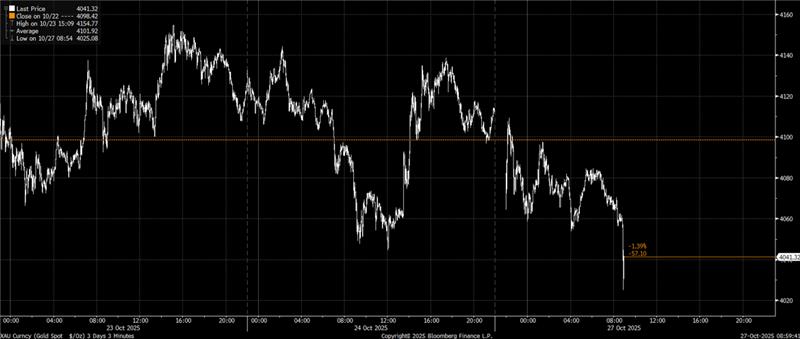

Equities began the week on a constructive note following productive US-China trade talks over the weekend. The discussions covered a broad range of topics, including export controls, shipping, fentanyl, and agriculture. China may resume “substantial” soybean purchases and defer its rare earths export controls for a year, while the extra 100% tariffs on Chinese goods threatened by Trump are likely off the table. The upbeat tone has raised hopes of an extended trade truce, creating a positive framework ahead of Thursday’s high-stakes summit between Trump and Xi. The sanguine tone weighed on gold as prices extended its decline, retreating by 1% on Monday morning (Chart 1, Bloomberg)

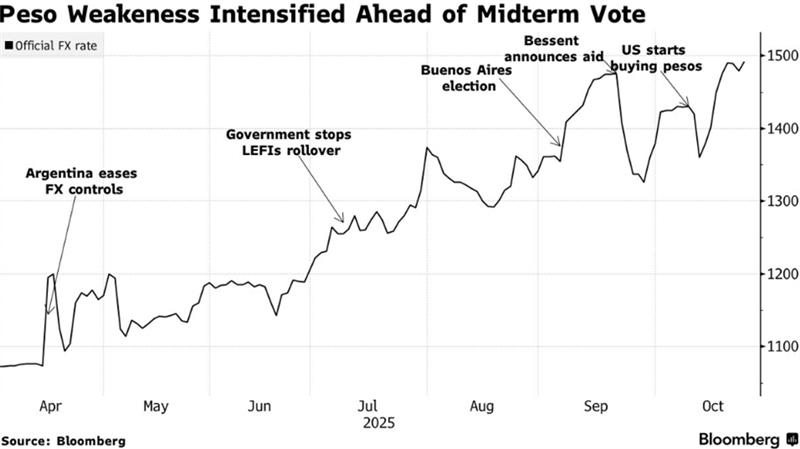

Argentine President Javier Milei’s libertarian party won a landslide victory in Sunday’s midterm elections. His gains will help him accelerate structural reforms, including deregulation and reducing spending. Before the vote, the US had pledged up to $40bn of support for Argentina, including a $20bn central bank swap line and plans for a $20bn loan facility to purchase Argentine debt, which was contingent on the election outcome. Following this, Argentine assets are expected to recover, led by dollar bonds, and the peso, which saw increasing volatility and weakness ahead of the vote (Chart 2, Bloomberg).

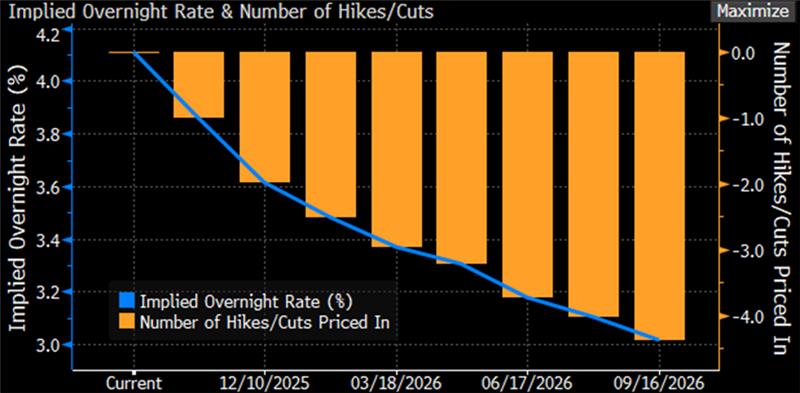

US inflation has hit 3% for the first time since January last month; however, this was less than the expected 3.1%. The inflation figures resulted in a ‘dovish cut’ tone, driving the S&P 500, Nasdaq, and Dow Jones to new all-time highs. A 25bps cut is all but priced in for this week’s Fed meeting, to bring the rates down to a 3.75% to 4% range (Chart 3, Bloomberg). The odds of a December rate cut have been raised from 91% to 98.5%, according to the CME FedWatch tool. Nonetheless, the US 2-year and 10-year Treasury yields remained sticky at the 3.5% and 4% levels, respectively.

A University of Michigan survey showed consumer sentiment cooled in October at 53.6, the lowest reading in five months.

Data today: German IFO business conditions, US Durable Goods Orders, South Korea GDP.

Big week for earnings – Microsoft, Google, Meta, Apple, Amazon. Oil majors: Exxon, Chevron, Shell.