Morning Macro 7th November

Breaking: The US is set to ban Nvidia’s scaled-down AI chips from being sold to China! Washington’s move targets B30A chips – used to train large language models when efficiently arranged in large clusters – designed to bypass earlier sanctions. But this would create a big opportunity for China to build its own chips domestically, as Nvidia CEO Jensen Huang warned: “China is going to win the AI race.”

Equities are having a rough time. The S&P 500 dropped more than 1.1% and Nasdaq 1.7% yesterday, with futures consolidating this morning. Big tech stocks suffered with Amazon down 2.8%, Nvidia down 3.6% (Chart 1, Bloomberg), Microsoft down 2%, Palantir tumbled 6.8%! Meta is now down over 22% from its August high!

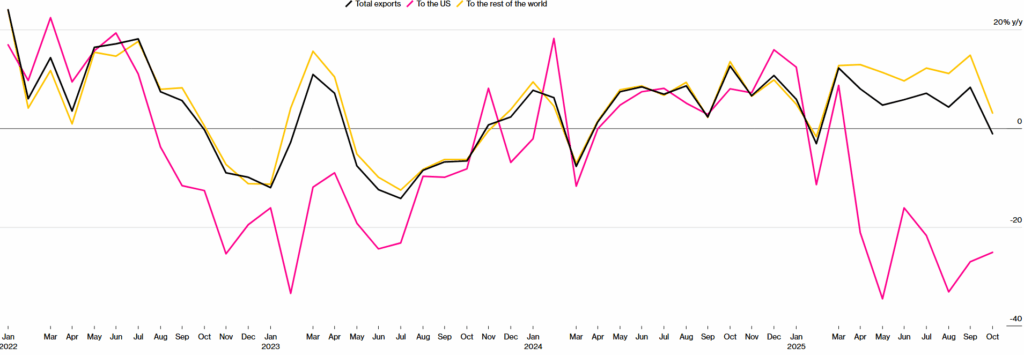

China’s exports unexpectedly fell 1.1% y/y in October, the first drop in eight months, as a sharp 25% slump in shipments to the US outweighed gains elsewhere. The decline, driven by weakening global demand and fading export resilience, signals mounting pressure on China’s slowing economy amid weak consumption and a prolonged property slump – a triple whammy to growth. Meanwhile, modest tariff relief from the US may offer only limited support. Exports still exceeded $3 trillion year-to-date, though momentum is fading. (Chart 2, Bloomberg)

The Bank of England held rates stable at 4% – as expected – before the Nov 26 budget announcement; however the committee was split 5-4. The OIS market is now pricing over 70% chance for a cut in the December meeting, while its fully expecting a cut in the Early February meeting.

US travel stocks are in focus after upbeat updates from Expedia and Airbnb. Expedia lifted its full-year outlook on resilient holiday demand, with shares up 18%, while Airbnb forecast strong Q4 bookings, rising 5.5%. UK-listed IAG reported Q3 revenue and profit slightly below estimates but noted solid travel demand and strong Q4 bookings despite some North American softness.

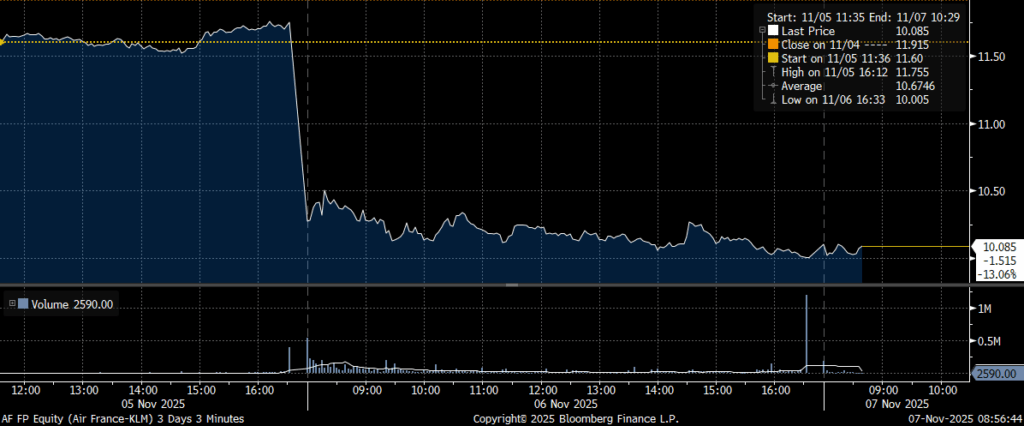

European peers didn’t face the same fate with Air France down almost 15% on the day, even despite good earnings! (Chart 3, Bloomberg)

Japanese household spending rose 1.8% y/y in September, missing expectations of 2.5% and slowing from August’s 2.3%. The data point to a steady yet fragile recovery in consumer demand, with weaker spending on essentials like food, housing, and utilities offset by gains in medical care and household items. On a monthly basis, personal spending fell by 0.7% – marking the first fall since June.

Data today – US Michigan Consumer Expectations, Canada Employment