The Jul’25 Brent crude futures concluded bullishly last week, fuelled by positive developments in US trade talks and further sanctions on Iranian oil. As of Monday morning, prices have recouped previous losses and surpassed $65/bbl, a two-week high. This week, we expect the bullish momentum in crude oil to continue, with Brent closing between $66-69/bbl. The key factors influencing crude oil sentiment this week are the following:

- Breakthrough in US-China trade talks

- Key US Economic Data

- Market Positioning

In a significant de-escalation of the trade war, the US and China have agreed to slash tariffs on each other for 90 days while discussions continue. This agreement comes after the high-level meetings between the sides in Geneva over the weekend. The US would reduce its tariffs from 145% to 30%, while China would lower them from 125% to 10%. In a marked contrast to the previously hostile rhetoric and tone, both sides signalled optimism, agreeing to work constructively together and maintain continuous communication. Risk assets, including oil, reacted positively to these developments because the tariff concessions were larger than anticipated. Whilst overall uncertainty persists and specific details in the agreement still need to be ironed out, positive engagement between both sides is conducive to risk-on sentiment in the short term.

Key US economic data this week will give early indicators of the early impact of US tariffs on inflation. US CPI data comes out on Tuesday, PPI and retail sales on Thursday, and the University of Michigan Consumer Sentiment on Friday. According to a Bloomberg survey of economists, m/m inflation is expected to rise by 0.3% in April, up from 0.1% in March. Meanwhile, little change is expected in April retail sales, following a 1.5% rise in March, as front-loaded demand for motor vehicles cooled, and perhaps also a reflection of increasing consumer caution around inflation. Finally, PPI data will provide insight into shifting wholesale costs and the impact of rising input costs on supply-side inflation pressures. The extent of the inflationary pressure reflected in upcoming economic data will shape the Fed’s approach to future rate adjustments, and by extension, oil prices through its impact on demand and the dollar.

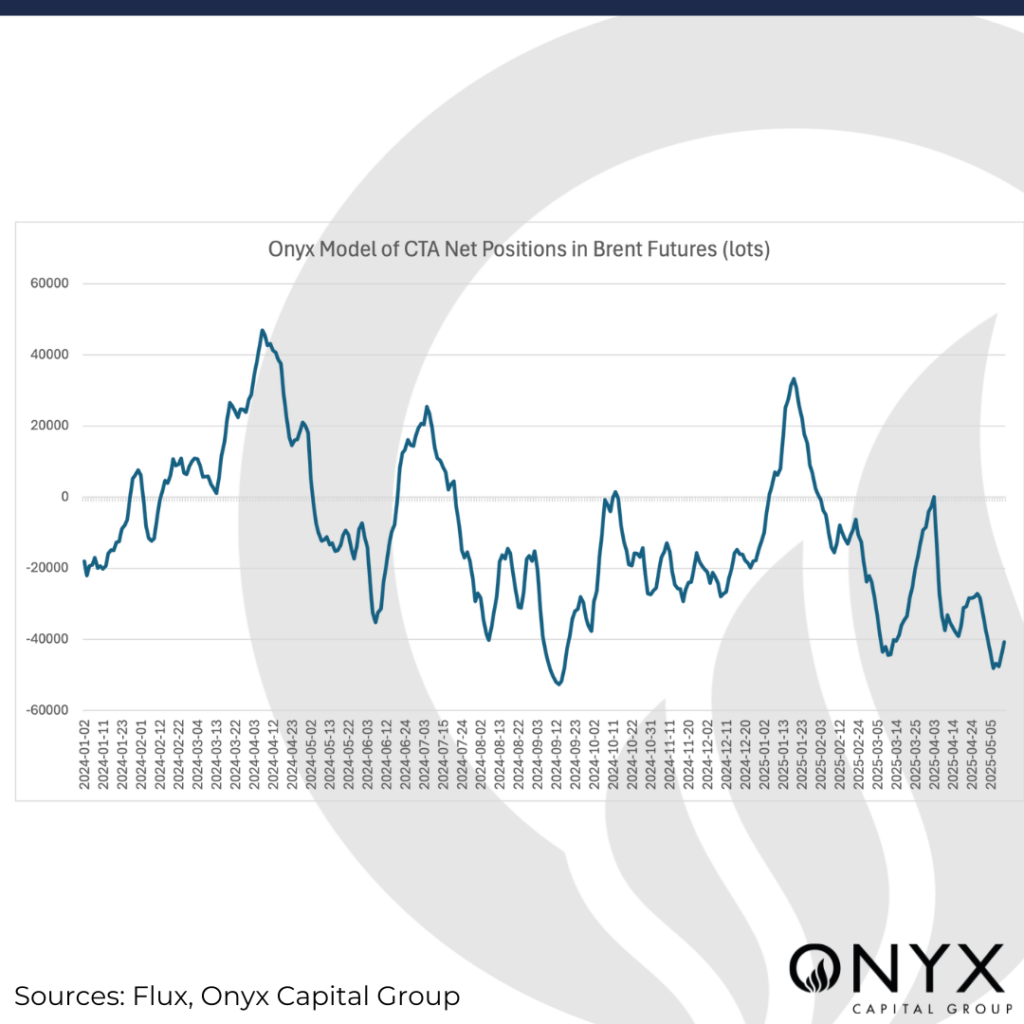

Finally, market positioning could play an outsized role in driving prices higher. CTA positions are climbing from a baseline of near-maximum shorts of -48k lots in Brent, and there remains substantial room for further buying if momentum builds. Meanwhile, ICE COT data for the week ending 6 May indicates that net length in Brent futures fell to the lowest level since October. This suggests both room to rebuild length and the potential for further rallies, in the event of bullish catalysts, driven by the unwinding of stretched short positioning.