View: Bearish

Target Price: $61-63/bb

Critical Resistance Ahead

The M1 Brent futures contract remains rangebound between $62 and $63/bbl, with a strong resistance level at the 50-day moving average (blue line on the chart below). Despite the bullish optics of a prolonged war between Ukraine and Russia, momentum has yet to be strong enough to break above the 50-day MA successfully. We expect this trend to continue this week and anticipate prices to slip lower, targeting $61-63/bbl as our price target.

- G7 countries mull over a full maritime services ban for Russian exports

- FOMC Meeting

- Positioning at neutral

G7 countries mull over a full maritime services ban for Russian exports

While the oil market was bracing for a long-awaited Ukraine-Russia ceasefire only a fortnight ago, that outlook has since blurred after last week’s lack of progress in Washington-Moscow talks. The Group of Seven countries and the European Union are reportedly considering replacing the current price cap on Russian oil exports with a full ban on maritime services to further squeeze the Kremlin’s oil revenue, according to a Reuters report dated December 5.

Russia exports over a third of its oil, mainly to India and China, via Western shipping and tankers; such a ban would push it further toward shadow fleets and may feature in the EU’s next sanctions package, expected in early 2026. During his visit to New Delhi last week, Russian President Vladimir Putin said Moscow stands ready to provide “uninterrupted shipments” of fuel to India and, while claiming to pursue a “peaceful solution,” warned that Ukraine must withdraw from Donbas or face its seizure. With a ceasefire being the main downside risk to oil, we see prices finding a floor at the low $60s handle in this will-they/won’t-they environment.

FOMC Meeting in Focus

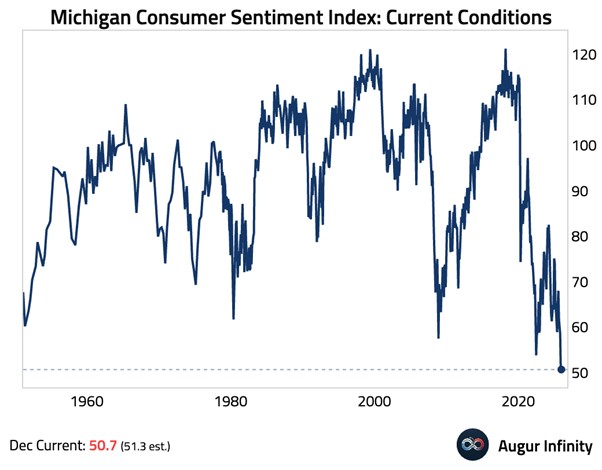

The December University of Michigan consumer sentiment index rose slightly m/m. However, its current conditions index sits at an all-time low (chart below, Augur Infinity), labelling this the worst perception of the US economy since the Great Depression in the 1930s. Although this may weigh on oil demand from the world’s largest economy, the Fed is now poised to cut the federal funds rate by 25 basis points in its meeting on 09-10 Dec. Core inflation, as measured by the Fed’s preferred Personal Consumption Expenditures (PCE) price index, cooled slightly more than expected.

Additionally, the labour market continues to cool down, with US weekly jobless claims falling to a more than three-year low in the week ending 29 Nov and the private ADP employment report showing a job cut of 32,000 in Nov 2025, the most significant decline in payrolls since March 2023. Given this, focus will instead be on any dissent among Fed members, along with comments by Chair Powell. A more dovish outlook by the Fed would support risk assets such as oil.

Trendless Technicals

The murky geopolitics of the widening conflict between Russia and Ukraine, and the worrying increase in tensions between the US and Venezuela, cloud the picture fundamentally. Thus, moving to the technical view, M1 Brent futures lacks a solid trend, although it remains bound by a downtrend line from the end of September (white dashed line), which indicates a clear pattern of lower highs. There is an incredibly weak trend in the market, with volatility trending sideways and the daily candles showing small intraday ranges. Momentum is bearish, and growing as per MACD, showing an increasingly negative histogram and the stochastics having a bearish crossover.

However, these are not very strong signals with the MACD and signal line very close together, while the stochastics indicator has seen many crossovers, which undermines its validity as a sell signal. Technically, there is little to point to a breakout in either direction, with the trendline and 50-day moving average proving strong resistance in the past month or two. It seems like the downtrend is intact, if very weak.