Target Price: $67-69/bbl

View: Bullish

Following a weaker end to last week ahead of Sunday’s OPEC+ meeting, we expect the M1 Brent futures to see more support on low volatility and thin liquidity amid APPEC in Singapore this week, expecting prices to end between $67 and $69.

- Key drivers:

- 1. Fading expectations of a ceasefire between Russia and Ukraine

- 2. Saudi OSPs to Asia

- 3. Positioning data supporting more upside than downside

Driver #1: Fading ceasefire expectations between Russia and Ukraine

US President Donald Trump said that he is ready to move to a second phase of sanctioning Russia, days after speaking with European leaders and stressing that Europe must stop purchasing Russian oil. European leaders are expected to travel to Washington early this week to discuss ways to end the war, as per President Trump.

This threat to ramp up sanctions comes amid Russia’s heaviest aerial bombardment on Ukraine since the war began in February 2022, involving at least 810 drones and 13 missiles, killing four people and damaging Ukraine’s main government building in Kyiv for the first time.

Driver #2: Saudi OSPs to Asia

Following OPEC+’s 137kb/d supply hike for October on Sunday, the market has shifted focus to the upcoming Saudi Arabian crude official selling prices (OSPs) to Asia.

M2/M4 Dubai swap structure indicates weaker OSPs (by ~$0.55/bbl m/m), which may encourage a rise in allocations to China, which were relatively muted last month. Moreover, India bought 22.5mb of Saudi Arabian crude for September loading last month, up around 4mb/d m/m. With peak oil demand rising ahead of India’s festival season in October and rising pressure from the US’ crackdown on Russian crude, a lower OSP could incentivise India to up its purchases of Middle Eastern crude.

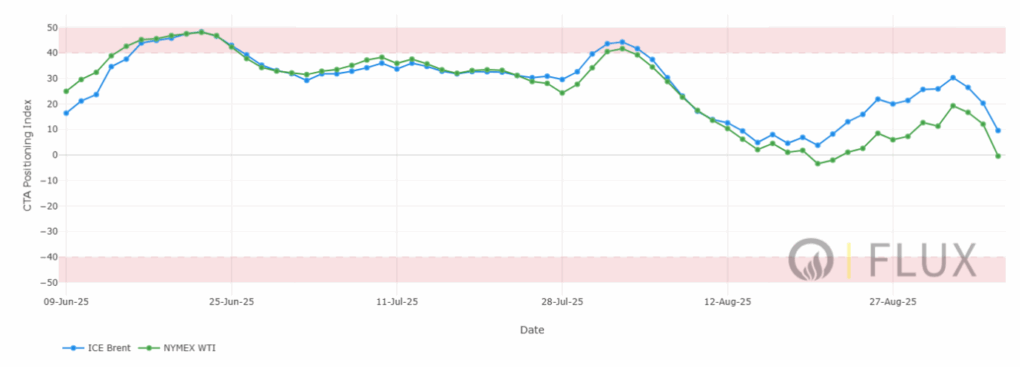

Driver #3: Positioning Data

Finally, Flux Insight’s CTA model shows a substantial decline in CTA net length in Brent and WTI futures, down to -11k and -14k lots on 5 Sep, respectively.

Although net length is projected to decline further on 8 Sep, a normalised view of this positioning (with z-scores between -50 and +50) shows that net length is forecast to revert near its long-term average. Without another bearish catalyst, this level may lead to a more balanced flow amid this week’s low liquidity backdrop.