The Officials: The Liquidity Report 1.35

In the week ending 3 October 2025, exchange traded futures volumes rose w/w across all contracts in the front three tenors, except the December and January WTI futures.

In the week ending 3 October 2025, exchange traded futures volumes rose w/w across all contracts in the front three tenors, except the December and January WTI futures.

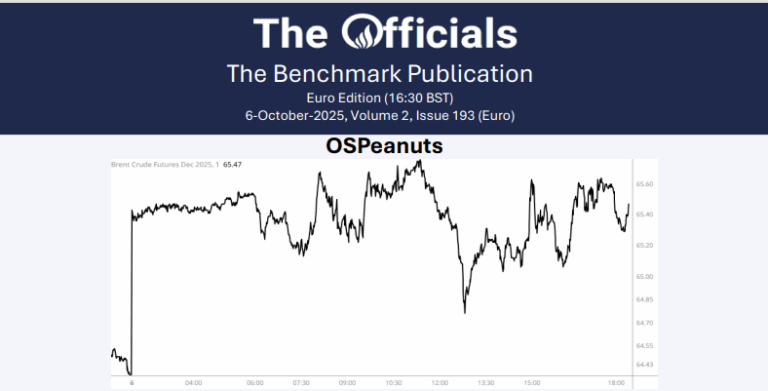

Brent found its feet in the Asian session, fluctuating in the mid-$65 range. It got choppier when Europe woke up on a grey, sunless morning but reached the close at $65.64/bbl.

The Dec’25 Brent futures contract dipped this morning from $65.83/bbl at 07:35 BST to $65.16/bbl at 10:00 BST (time of writing). In the news, China is set to add 11 new oil reserve sites in 2025 and 2026, with a total capacity of about 169mb. This choice has been stated by public sources as a method of protecting supply security. Elsewhere, Shell has said that it is expecting a $600m hit in Q3 after it abandoned a biofuel project in Rotterdam, citing that the project was scrapped because it would not have been competitive. In Nigeria, the chief executive of the Nigerian National Petroleum Company reported that the 3-day national strike at the Dangote refinery has caused production losses of 600kb. In other news, Brazil state-run oil firm Petrobras has signed a $1.8bn contract for Boaventura refining project. This includes the building of 2 units to produce diesel S-1 and jet fuel. In Freeport, Texas, a fire broke out at Dow’s chemical plant; Dow reported no employee injury, but facility damage has yet to be assessed. Finally, at time of writing, the front month Dec/Jan’26 and 6-month Dec/Jun’26 spreads are at $0.39/bbl and $0.72/bbl, respectively.

Another day, same headline. Gold, S&P500, Nasdaq & Bitcoin make new all-time highs, maybe, just maybe the Fed doesn’t need the 102bp cuts priced by the OIS over the next 12 months, but beware rising yields is what killed to 2022 rally. Adding fuel to the fire we’re getting some wile equity predictions for 2026 including the chance that the S&P500 reaches 9,000 (currently 6,740). Meanwhile in the real world we have weak German data this morning, and China increasing its strategic oil reserve facilities.

GERMANY AUG. FACTORY ORDERS FALL 0.8% M/M; EST. +1.2% – BBG

GERMANY AUG. FACTORY ORDERS RISE 1.5% Y/Y; EST. +3.1%

CHINA PLANS 11 NEW STRATEGIC OIL RESERVE FACILITIES BY 2026

AMD closes +23.7% on news of a deal with OpenAI setting it on a path to challenge Nvidia. In response Nvidia falls -1.1%. Yet Nvidia represents 5.04% of the MSCI All Country World Index. The MSCI ACWI Index captures ~85% of global equity markets, including large and mid-cap stocks. Nvidia’s weight now significantly surpasses Japan’s 4.78% share, the world’s 3rd-largest stock market. By comparison, China, the UK, and Canada account for 3.33%, 3.23%, and 2.92%, respectively.

Gold futures officially closed above $4,000 as The People’s Bank of China has reported that its gold reserves rose by 1 tonne in September – now 11 consecutive months that its gold holding have increased. Gold reserves now total 2,304 tonnes, 24 tonnes higher than at the end of 2024.

At silver’s historic peaks, the silver/gold ratio hit 5.8% (1980) and 3.0% (2011). Today? Just 1.2%. (Chart 1, @yuriymatso)

Trilogy Metals stock, TMQ, surges over +210% after the US government announces it will be taking a 10% stake in the company.

The trump administration now holds strategic equity positions including:

• 10% stake in Intel ($INTC)

• 15% stake in MP materials ($MP)

• 10% stake in Lithium Americas ($lac)

• 10% stake in Trilogy Metals ($TMC)

• a “golden share” in U.S. Steel corporation and has floated taking equity in major defence contractors as part of its national industrial policy.

Goldman raises its “Dec2026 gold price forecast to $4,900/oz (vs. $4,300 prior) because the inflows driving the 17% rally since August 26th – Western ETF inflows and likely central bank buying – are sticky in our pricing framework”……….. a very brave call, LOL, even I could do that!!

Paul Tudor Jones said today on CNBC right now feels a lot like 1999 and that he thinks we could be heading for a blow off top……. While YARDENI LIFTS S&P 500 TARGET TO 7,000 ON ECONOMIC STRENGTH Yardeni Research raised its year-end S&P 500 target to 7,000, citing a resilient U.S. economy and improved sentiment after Trump’s trade resolution……. And even more bullish EVERCORE: S&P 500 COULD HIT 9,000 BY 2026 IN ‘BUBBLE’ SCENARIO… Evercore ISI’s Julian Emanuel says the S&P 500 could reach 9,000 by 2026 under a bubble scenario, up from the firm’s base target of 7,750.

You probably don’t own enough copper stocks (Charet 1, @minenergybiz)

UK September Halifax house prices -0.3% vs +0.2% m/m expected

Data today – NY Fed Inflation Expectations data

In September, as the conflict between Russia and Ukraine has been raging for three and a half years, a resolution continues to elude. There continues to be no strong voice for peace, although US President Trump’s position on the conflict has completely reversed at the end of the month, which was shocking but remains met with scepticism. Assessing the extent of damage to Russia’s refineries is challenging, as officials are unlikely to disclose details, and available footage doesn’t clearly show which units were affected. The ongoing wave of attacks has significantly impacted the gasoil market, with roughly 800 kb/d of loadings now at risk as terminals come under fire. In response to domestic supply issues, Russia has imposed a partial diesel export ban through the end of the year, boosting bullish sentiment. However, since the restriction mainly targets resellers rather than producers, the actual export impact is expected to be limited to around 40 kb/d. This has also increased pressure on US exports, and the middle distillate market has been reactive to the EIA stats each week. The Oct’25 ICE gasoil crack rose above $28.00/bbl on 26 Sep in response to the ban. This has softened to $24.30/bbl at the time of writing on 06 Oct, as the market digested the news and EIA stats for the week to 26 Sep showed a quite strong export value of 1.38kb/d, and buying in the gasoil E/W from physical players suggests movement of product to Europe. Levels are quite strong, overall, with the rolling M1 crack almost $5.00/bbl above their pre-war value for this time of year and technical indicators pointing to increasing bearish momentum.

Busy times. OPEC over the weekend, Saudi OSPs on Monday, and allocations later in the week. See for more in the report!

Another week brings another selection of new trade ideas from Flux Insights. This week, we look at trades in Gasoline and Naphtha….

Looking at Flux Insight’s CTA positioning, Brent reached highs of 3.6k lots on 29 Sep before Brent positioning flipped short the following day, falling by nearly 30k lots to -26k lots on 6 Oct. From an index position, in middle distillates, positioning remained in the overbought territory for most of the week ending 30 Sep but trended downward, albeit by a much slower rate than crude. ICE gasoil reached 15k lots on 29 Sep before reversing to -3.9k lots on 6 Oct; Heating Oil peaked at 11.8k lots on 29 Sep and reversed to -5.5k lots on 6 Oct. RBOB futures were pressured with positioning remaining the most bearish, falling to -32.2k lots, nearing oversold territory from an index perspective.

Money managers have been risk off in the week ending 30 Sep, trimming their ICE Brent futures long positions (-7mb, -2.23%) for a second week in a row; for this week they added 2.7mb (+2.35%) to their short positions. Money managers have decreased their net positionings, perhaps due to increasing OPEC+ supply announcements. Like money managers, swap positions trimmed longs by 21mb (-4.90%) and added 5mb (+9.41%) to their shorts, the largest percentage increase since Jun 2025. In contrast, producers/merchants added to their longs (+17mb, +1.58%), flipping their positioning from the week prior, while simultaneously liquidating shorts (-27mb, -1.87%) for the second consecutive week. Open interest decreased in the week ending 30 Sep, by 4mb (-0.15%), likely indicating longs taking profit.

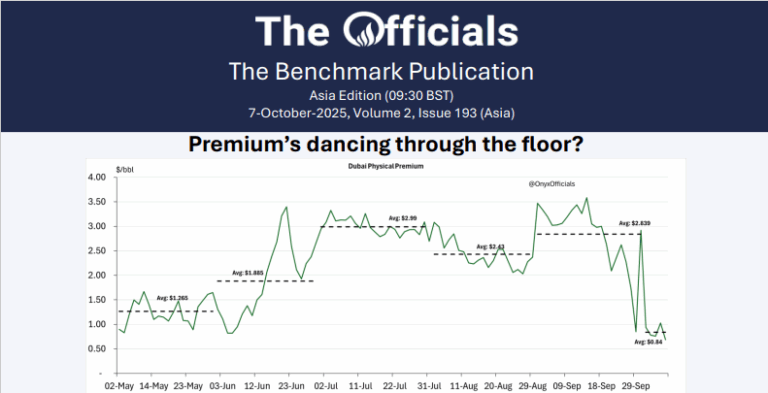

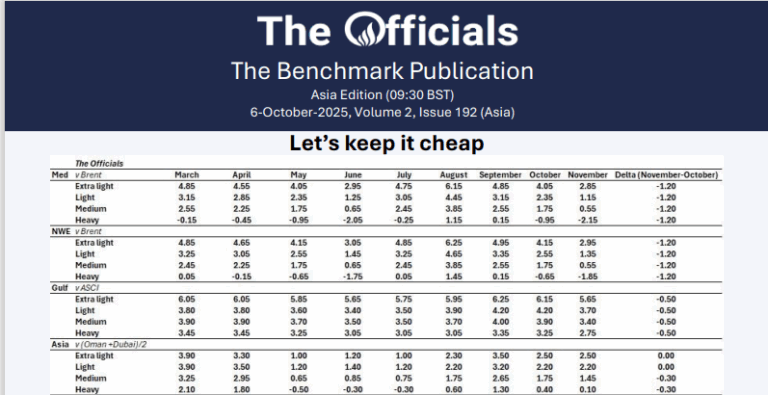

They don’t like to be predictable! The Saudis kept November OSPs for Extra Light and Light to Asia flat from October, at the average of Dubai and Oman +$2.50 and +$2.20, respectively. Medium and Heavy were each cut by 30c.

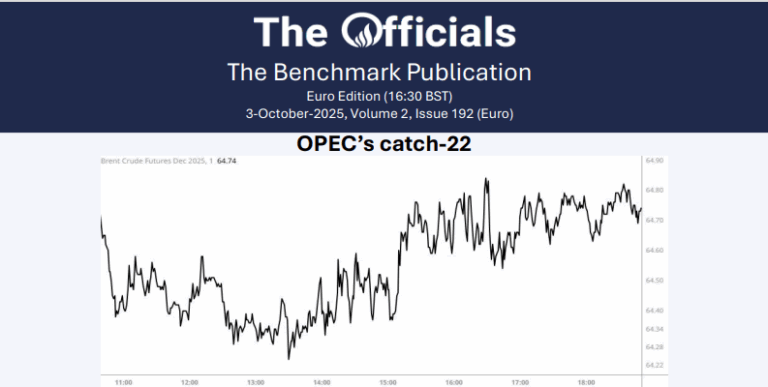

The Dec’25 Brent futures contract gapped up by roughly $1 from Friday’s close ($64.37/bbl), trading within the 60c range between $64.35/bbl and $65.63/bbl before rising to $65.65/bbl at 10:40 BST (time of writing). In the news, OPEC+ has announced a modest 137kb/d output increase to be implemented in November. Reuters reported tensions between Russia and Saudi Arabia as the former pushed for modest increases while the latter lobbied for a more aggressive hike. In other news, the Russia defence ministry has claimed to have destroyed 251 Ukrainian drones overnight on Sunday. A fire was reported by RBK-Ukraine media at an oil depot in Fedosia on the Crimean coast, where a fuel tank exploded as a result of the attack; Reuters has been unable to independently verify these claims. Elsewhere, the National Oil Corporation of Libya has said that Italy’s Eni has begun drilling operations offshore after a 5-year break due to the COVID-19 pandemic. Further, a senior company executive of India’s Sahara Group has been cited saying that the conglomerate plans to be producing 350kb/d of crude oil daily in Africa by 2030. Finally, at time of writing, the front-month Dec/Jan’26 and 6-month Dec/Jun’26 spreads are at $0.45/bbl and $0.90 bbl, respectively.

More stimulus!!!…. Sanae Takaichi is the new Japanese Prime Minister, Japan’s first-ever female leader and she’s coming in swinging with huge stimulus plans. The Nikkei surges 4.75%, Yen falls -1.8% and the Yen curve steepens aggressively with 2-year yields down 4bp while 30-year rallies 13bp. Precious metals love stimulus too with gold and silver both 1% higher, new all-time highs for gold and silver homing in on $50. Bitcoin also makes new record highs touching $125.7k and the US dollar also rallies another 0.5% and seems to be trending higher having bottomed at 93.30.

With no payrolls data on Friday the Goldman Sachs big data payroll tracker shows a rebound for September. Goldman: “Our updated job growth tracker which combines the signal from still-available Big Data measures of job growth, measures of layoffs, and surveys of households and businesses, rebounded to 80k/month in September after falling to a trough around 0k in April and May.” (Chart 1, Goldman Sachs)

Data this week:

1. NY Fed Inflation Expectations data – Tuesday

2. Fed Meeting Minutes – Wednesday

3. Fed Chair Powell Speaks – Thursday

4. MI Consumer Sentiment data – Friday

5. MI Consumer Expectations data – Friday

OPEC needs to be careful this weekend, as its positioning at the meeting could easily spook a market already nervous about being long and a coming price war. Be prepared in case of a misjudgement and the loud sound of a toilet flushing on Monday morning as flat price plunges. Who could add 500 kb/d anyway? We’re scratching our heads trying to figure it out; most members are flat out already! Only KSA has any real spare capacity – it’s not OPEC, it’s Saudi!

This report reviews weekly oil inventory data from the US EIA’s Weekly Petroleum Status Report, Global Insights’ ARA Independent Storage and International Enterprise’s Singapore product storage

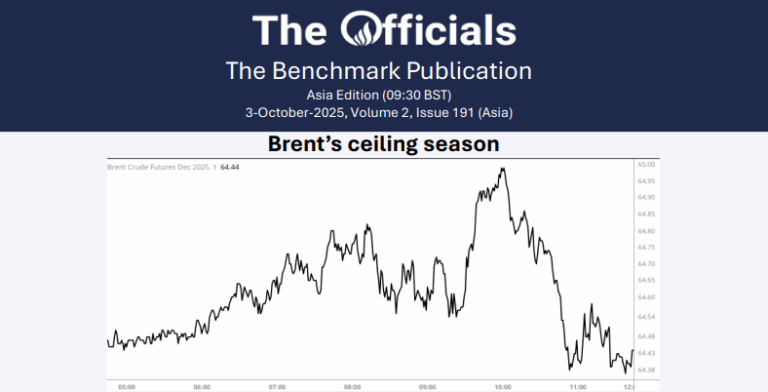

Does it want $65 or not? Brent bounced back off the $64 level and briefly looked like it wanted to get above $65 again at 10:00 BST, before dropping back. Was the bearishness flushed away yesterday? Well, Brent is stronger than it was at the end of yesterday’s trading, but still looks rather deflated. Spreads and flat price are going funky – read about the impact of the El Segundo fire on the next page!