Dated v Brent:

Loading graph...

Edge Updates

Dated Brent Report – Rolling Down

The geopolitical risk premium may have faded, but the continued rally in Brent structure highlights the market's resilience. Futures spreads have been on a steady upward trend since the beginning of May, with Sep/Oct Brent strongly backwardated above $1/bbl (time of writing). The market has fundamental strength, with strong refinery margins that are a driver of crude demand. Resurgent distillate strength took the market by storm, but something has to give. Product cracks would eventually correct lower on account of higher production. At the same time, hot temperatures across Europe and heat-related disruption would force refiners to cut their run rates, tempering crude demand. Nonetheless, Forties saw buying from Chinese players (Petroineos and Unipec) in the physical window, taking advantage of momentary Dated weakness and Dubai strength to fix arbs into Asia potentially.

Dated Brent Report – Brent Synchronisation

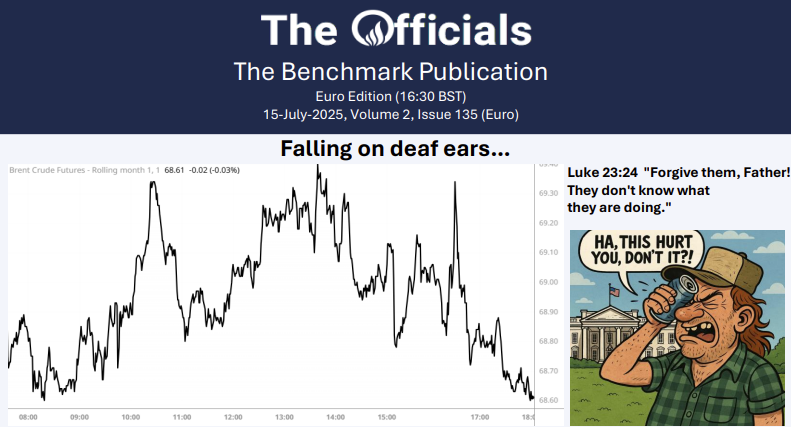

It was quite the turnaround in Brent this week. Markets did a quick 180 as Middle East tensions de-escalated following Iran's telegraphed attack at a US military base in Qatar, in retaliation for American strikes against its nuclear sites. The geopolitical risk premium popped like a balloon. Bullish momentum was already waning before that, given the market's muted reaction on Monday's open, alongside the presence of Eni and Shell in the physical window, selling Forties. So synchronised were the directions of Brent futures and Dated. The futures rally on 13 June magnified the squeeze on deliverable supplies in Cushing, tightening the market and buoying Total's bids in the North Sea physical. DFLs were sent to the stratosphere, with Jul'25 touching $2/bbl. But as the old adage goes, what goes up must come down. Since the geopolitical risk deflation on 23 June, Brent spreads and DFLs are back to square one, before the geopolitical rally. The forward curve is implying weaker, especially the prompt week of 30-04 July. Glencore joined in on the selling party on 24 June, offering Midland, while BP put a Midland cargo into chains, the first of the month. We expect this trend to continue, but the fate of the prompt rolls will depend on how much the physical weakens, forming a basis for our dual trade idea. The front (July rolls) are slightly oversold, while the back (August rolls) is more overbought. Even at lower levels, there is a lack of buying, apart from refiner bids. As Dated weakens, it may be more difficult to fix arbs from the US to Europe, especially amid higher freight rates. Demand outlets would need to come from Chinese players lifting Forties, which is currently setting the curve. Stronger refinery margins may provide renewed support, especially as we've observed hedge selling flows of cracks with the refinery margins forward curve shifting noticeably higher. However, the market is more risk-off, given the elevated, headline-driven volatility recently. Despite our cautiously bearish views, renewed geopolitical headlines could see another upside breakout and volatility spike. Open interest is above average in Jun'25 contracts, but is trending in line with the 5-year average in Jul'25, underscoring the relatively subdued interest by the market. The question now becomes, how low does Dated Brent go? Prices have retraced below pre-event rally levels, but remain high on a notional basis. There is room to go longer, but are we approaching a consolidation?

Brent v Dubai:

Loading graph...

Latest News

Edge Updates

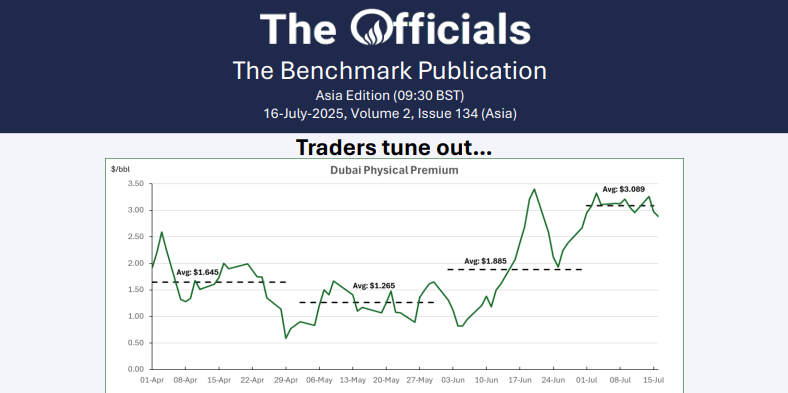

Dubai Market Report – Summer Lull

While the Bal-Jul’25 Brent/Dubai briefly ticked up from -$1.20/bbl on 1 Jul to -$0.65/bbl on 3 Jul, the contract sold off to a low of -$1.46/bbl on 15 Jul. Similarly, the Aug’25 Brent/Dubai weakened from -$0.09/bbl on 3 Jul to -$0.45/bbl on 10 Jul

Dubai Market Report – Back to the Status Quo

The Dubai market has largely returned to normality as geopolitical risk unwinds. As per usual, the Strait of Hormuz didn't close this time, although there was noticeably more market anxiety. The forward curve is being heavily pressured, with Brent/Dubai boxes aggressively selling off. On the first day of July pricing, the Jul'25 Brent/Dubai fell below -$1/bbl, while the Jul/Aug'25 box came off to -$0.95/bbl, which marks an extreme contango structure. Aug'25 is following suit and was the next contract to fall below flat. Another notable drop was Q4'25/Q1'26, which fell from $0.05 to -$0.15/bbl. The market has largely disregarded the prospect of OPEC+ supply hikes, interpreting it as existing overproduction being formalised. The combination of the market buying Cal26 and selling front boxes would have put participants comfortably in the money. Here, trade houses and majors were the main players. Previously, we noted that refinery sell side hedging flows in Cal26 had distorted Brent/Dubai. Now that these flows have subsided, this distortion has left a vacuum conducive to a mean reversion. There is greater conviction in the downside for Brent/Dubai boxes as these flows are more speculative, whereas refinery flows are more price-agnostic.

Free Dashboards

Free Onyx Officials

Rewriting the oil rules: Murban Mess

Upcoming events

Aug25 WTI Expiry

in 6d

Fujairah Inventories

in 7d

API Stats Release

in 7d

API Stats Release

in 7d

ARA Product Inventories

in 8d

ARA Product Inventories

in 9h

Aug25 WTI Expiry

in 6d

Fujairah Inventories

in 7d

API Stats Release

in 7d

API Stats Release

in 7d

ARA Product Inventories

in 8d

ARA Product Inventories

in 9h

Aug25 WTI Expiry

in 6d

Fujairah Inventories

in 7d

API Stats Release

in 7d

API Stats Release

in 7d

Latest News

COT Report: Sweet Spot

12h ago

LPG Report: Building a Bear

13h ago

US EIA Weekly Report

14h ago

The Officials: Traders tune out…

18h ago

{kind=link}

Most Popular

European Window: Brent Supported At $68/bbl

11h ago

The Sep’25 Brent crude futures briefly fell below $68/bbl but was supported above that level on Wednesday afternoon, trading at $68.22/bbl at 17:30 BST (time of writing). EIA stats indicated a 3.9mb draw in crude inventories in the week ending 11 July, against API indications of 800kb build. Commercial stocks are still 8% below the 5-year average for this time of the year. India’s oil imports from Russia rose marginally in 1H25, at 1.75mb/d, with Reliance and Nayara Energy making almost half the purchases. Egypt’s diesel and gasoil imports reached a record 370kb/d in the first half of July, 65% ...

COT Report: Sweet Spot

12h ago

See all the updates across the barrel in this week’s Onyx Commitment of Traders report, as well as six contracts to watch. Click on the relevant button below to access your COT report.

Dubai Market Report – Summer Lull

2d ago

While the Bal-Jul’25 Brent/Dubai briefly ticked up from -$1.20/bbl on 1 Jul to -$0.65/bbl on 3 Jul, the contract sold off to a low of -$1.46/bbl on 15 Jul. Similarly, the Aug’25 Brent/Dubai weakened from -$0.09/bbl on 3 Jul to -$0.45/bbl on 10 Jul

European Window: Brent Falls to $68.80/bbl

2d ago

The Sep’25 Brent futures contract fell to $68.78/bbl at 15:11 BST, before rallying up ot $69.31 at 16:31 BST. Prices have since fallen back to $68.80/bbl at 17:25 BST (time of writing). In the news, Iraq has signed a preliminary deal with US company HKN Energy to develop the Himreen oilfield in northern Iraq, with plans to increase production to 60kb/d from the current 20kb/d to 25kb/d. This announcement coincides with HKN Energy reporting an explosion that halted production at the Sarsang oilfield in the Kurdistan region. In other news, the European Commission has promised to address Slovakia’s concerns about ...

Dated Brent Supplementary Report – Forties Destination: China

2d ago

The Dated Brent physical differential saw a choppy week, falling to $0.38/bbl on 10 July before rising to $0.71/bbl by 14 July. Phillips 66 and Chevron were offering Midland, while Mercuria joined Total on the buy side. Petroineos returned after a brief hiatus, lifting P66's offer for a 4-8 Aug Midland cargo at +$1.80/bbl. There is an intent from the market to keep the physical supported, given that the strength in refinery margins keeps a floor on demand. However, the upside is limited given the influx of Midland cargos and offers.

European Window: Brent Under $70.00/bbl

3d ago

Sep’25 Brent futures were under pressure this afternoon from $71.35/bbl at 13:30 BST to $69.55/bbl at 17:25 BST (time of writing). Although Trump warned of possible 100% secondary tariffs on Russia if a ceasefire isn’t achieved within 50 days, the lack of immediate action put pressure on prices. The Euro recovered to around 1.1689 against the US Dollar USD after hitting a two-week low of 1.1654 earlier. The pair had slipped after Trump threatened 30% tariffs on European imports from 1 Aug, but a softer USD and hopes of talks helped it rebound. Meanwhile, the US Dollar Index held flat ...

Brent Forecast: 14th July 2025

3d ago

The Sep’25 Brent crude futures climbed higher last week, closing above $70/bbl and opening higher on Monday morning, reaching $71/bbl. Prices are at their highest level since the late June sell-off. We expect prices to remain elevated this week, with Brent to close between $70 and $73/bbl. The key factors this week are as follows: Geopolitics returns to the forefront this week amid President Trump’s announcements on tariffs and his shifting policy rhetoric towards Ukraine. Trump has delivered a litany of letters to some of the US’s biggest trading partners, the latest being directed towards Mexico and the EU, threatening ...

Refinery Margins Report

3d ago

- In the week ending 11 July, refinery margins declined slightly across all tenors, except for Q1’26 for Asian refineries, which increased by 0.13. - On a month-on-month basis, all margins have increased, with M1 in Europe and the US showing the largest rises of 2.33 and 2.96, respectively. - Despite M2 and M3 being slightly higher than M1 on the Asian refinery forward curve, the rest of the curve remains in contango. The higher M2/M3 margins are driven by stronger M2 levels across the cracks, with MOPJ, kerosene, gasoil, and 380 Dubai cracks priced higher over the past month. ...

Events

Jul 17, 2025

15:15

ARA Product Inventories

in 9h

Jul 22, 2025

18:30

Aug25 WTI Expiry

in 6d

Jul 23, 2025

08:00

Fujairah Inventories

in 7d

21:30

API Stats Release

in 7d

API Stats Release

in 7d

Jul 24, 2025

15:15

ARA Product Inventories

in 8d

Jul 29, 2025

19:00

FOMC Meeting

in 13d

Jul 30, 2025

08:00

Fujairah Inventories

in 14d

21:30

API Stats Release

in 14d

API Stats Release

in 14d

Jul 31, 2025

15:15

ARA Product Inventories

in 15d

18:30

Sep25 Brent Expiry

in 15d

Aug 6, 2025

08:00

Fujairah Inventories

in 21d

21:30

API Stats Release

in 21d

API Stats Release

in 21d

Aug 7, 2025

15:15

ARA Product Inventories

in 22d