U.S. equities wobbled again yesterday but both S&P500 & Nasdaq bounced from the 10th October closing lows. We’ll see how the market reacts to Nvidia earning tonight with the options market pricing a 7.5% share price move. Note the employment data yesterday also came out weaker than expected, and crypto assets continue their downtrend (don’t HODL with laser eyes and diamond hands, instead manage risk!).

Also note the Fear and Greed index is pointing to extreme fear, with the S&P500 off just 4.6% from its peak! 😊 (Chart 1, CNN Business) Note we typically see year end buying of equities particularly the last 2 weeks of December.

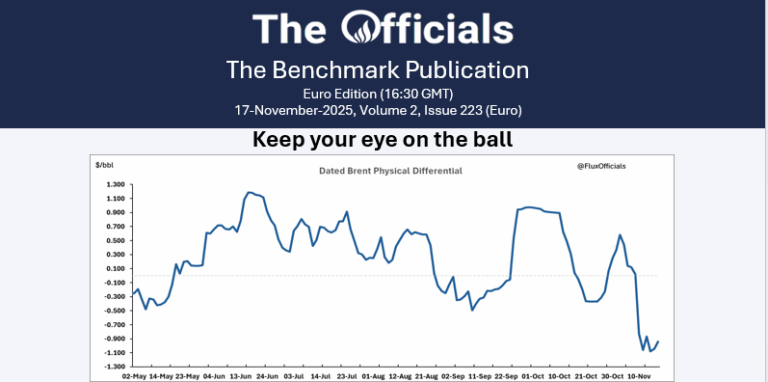

]

U.S. jobless claims rise 232,000; est. 223,000; prev. 219,000

Japan’s 40Y Government Bond Yield surges to 3.697%, its highest level in history, as markets prepare for more stimulus. This will awaken growing debt fears but also start to attract Japanese investment in US back to the mainland.

FED’S WALLER JUST SAID: – DECEMBER RATE CUT WOULD PROVIDE EXTRA LABOR-MARKET INSURANCE….. OIS pricing for December 10th meeting is back at 50% chance of a 25bp cut.

Bank of America fund manager survey perfectly captures the mood. Net 20% of respondents think companies are spending too much money on investment. Not just highest ever, but also the first time this number has ever been positive in the history of the survey. (Chart 2, BofA Global Fund Manager Survey)

Billionaire investor Peter Thiel fully exited Nvidia $NVD in Q3, selling all ~537k shares that were nearly 40% of his fund, per his latest 13F. Thiel Macro has cut US equity holdings from about $212m to $74m and is now basically parked in Tesla, Microsoft and Apple. Source: Wall Street Engine

This is quite the statement from a FTSE 250 CEO at Sirius… “We will not invest a penny in the UK in any meaningful form until June after the May elections.” Political doubts make UK property uninvestible,

The Financial Times has reported that Oracle’s $300 billion OpenAI deal is already underwater, now worth MINUS 74 billion, and stock down 36% from the highs. (Chart , @_investinq)

14 days since Burry publicly went bearish on AI… PLTR: -17.4% NVDA: -9.8%

FWIW (Chart 4, @_Investinq)

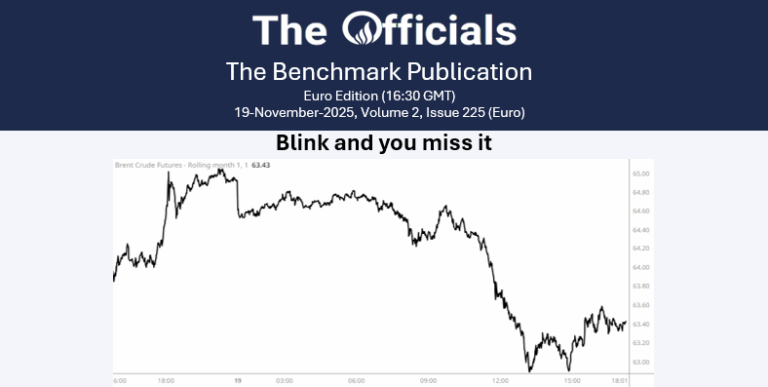

Data today – UK & EZ inflation, Fed minutes, Nvidia earnings