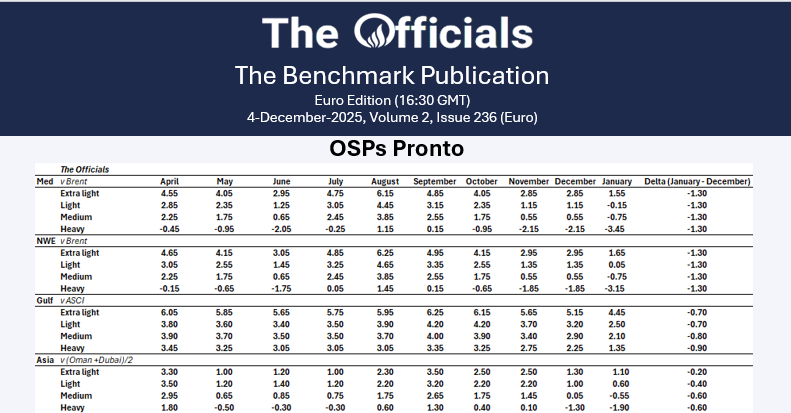

Dated v Brent:

Loading graph...

Edge Updates

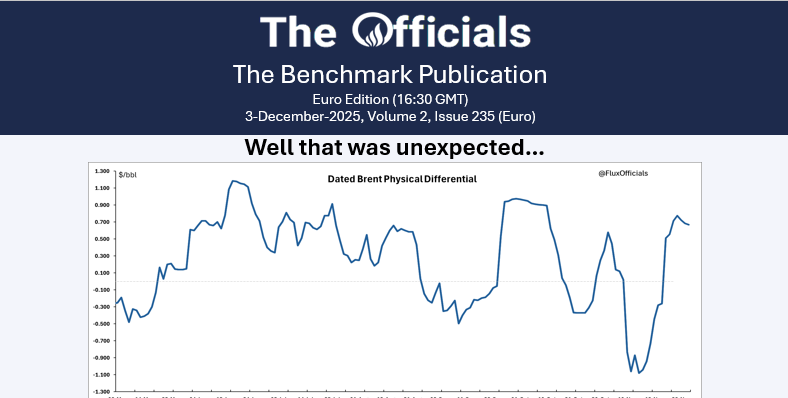

Dated Brent Report: Achieving Homeostasis

The North Sea physical differential climbed around $0.70/bbl this week, a significant shift from the negative diffs at the start of November. However, last week’s buy-side bias **has now turned shakier.** We saw a trade house sell-side of Dec weekly rolls and Dec/Jan’26 DFL last week. This flow dissipated as the physical inched higher, with 28 Nov instead seeing a trade house aggressively bidding 1H Dec into 2H Dec rolls. It appears that the prevailing regime has shifted again this week. We saw a trade house flipping to a sell-side axe in Dec'25 weekly structure on 01 Dec, leading to a sell-off in prices exacerbated by thin liquidity. The Bal-Dec’25 DFL fell from a high of $0.87/bbl on 28 Nov to $0.69/bbl on 01 Dec, where it met support and climbed to $0.75/bbl. The 01-05 Dec three-week roll sold down to $0.70/bbl, with the Bal-Dec/Jan’26 DFL roll standing at $0.22/bbl on 01 Dec. We saw similar sell-side interest on 02 Dec, with selling in the 15-19 Dec CFD and 15-19 Dec vs Cal Jan roll, with only some buying in Bal-week CFD and the 15-19 two-week roll supporting prices. Returning to the physical differential, although we continue to see the usual suspects buying the physical, prompt offers have been increasingly aggressive, casting a doubt on the robustness of this strength. We see relative support from the 8-12 Dec CFD, indicating that we may see some near-term support; however, it will be vital to monitor how sentiment shifts in the coming week.

Dubai Market Report: New Month, Same Range…

We have seen trading volumes remain extremely low in December. This week, the M1 Brent/Dubai remained in its tight range between -$0.90/bbl and -$0.55/bbl, as it has been for most of November, as it moved sandwiched between the 100-day and 200-day moving averages. The bodies on the candles are short and fail to reveal a pattern, but there has been a trend of higher lows d/d this week. On the other hand, the shadows on the candles shifted from being longer underneath the candles to above them. This shows that although there is better buying at the lower end of the range, there is better selling at the upper end. The market is still lacking any concrete directional consensus, with a limited risk appetite clear in the price action. As we approach the end of the year, the current de-risking is reflective of a market averse to further market uncertainty. The forward curve has started to flatten out, with Brent/Dubai contracts sitting between -$0.65 and -$0.35/bbl through most of the 2026 curve. There seems to be little to indicate a breakout without some fundamental changes, or a ceasefire between Russia and Ukraine, although the continued failure of these talks has built in some headline scepticism around the subject. Nevertheless, the current environment suggests a trend toward de-risking.

Brent v Dubai:

Loading graph...

Latest News

Edge Updates

Dated Brent Report: Achieving Homeostasis

The North Sea physical differential climbed around $0.70/bbl this week, a significant shift from the negative diffs at the start of November. However, last week’s buy-side bias **has now turned shakier.** We saw a trade house sell-side of Dec weekly rolls and Dec/Jan’26 DFL last week. This flow dissipated as the physical inched higher, with 28 Nov instead seeing a trade house aggressively bidding 1H Dec into 2H Dec rolls. It appears that the prevailing regime has shifted again this week. We saw a trade house flipping to a sell-side axe in Dec'25 weekly structure on 01 Dec, leading to a sell-off in prices exacerbated by thin liquidity. The Bal-Dec’25 DFL fell from a high of $0.87/bbl on 28 Nov to $0.69/bbl on 01 Dec, where it met support and climbed to $0.75/bbl. The 01-05 Dec three-week roll sold down to $0.70/bbl, with the Bal-Dec/Jan’26 DFL roll standing at $0.22/bbl on 01 Dec. We saw similar sell-side interest on 02 Dec, with selling in the 15-19 Dec CFD and 15-19 Dec vs Cal Jan roll, with only some buying in Bal-week CFD and the 15-19 two-week roll supporting prices. Returning to the physical differential, although we continue to see the usual suspects buying the physical, prompt offers have been increasingly aggressive, casting a doubt on the robustness of this strength. We see relative support from the 8-12 Dec CFD, indicating that we may see some near-term support; however, it will be vital to monitor how sentiment shifts in the coming week.

Dubai Market Report: New Month, Same Range…

We have seen trading volumes remain extremely low in December. This week, the M1 Brent/Dubai remained in its tight range between -$0.90/bbl and -$0.55/bbl, as it has been for most of November, as it moved sandwiched between the 100-day and 200-day moving averages. The bodies on the candles are short and fail to reveal a pattern, but there has been a trend of higher lows d/d this week. On the other hand, the shadows on the candles shifted from being longer underneath the candles to above them. This shows that although there is better buying at the lower end of the range, there is better selling at the upper end. The market is still lacking any concrete directional consensus, with a limited risk appetite clear in the price action. As we approach the end of the year, the current de-risking is reflective of a market averse to further market uncertainty. The forward curve has started to flatten out, with Brent/Dubai contracts sitting between -$0.65 and -$0.35/bbl through most of the 2026 curve. There seems to be little to indicate a breakout without some fundamental changes, or a ceasefire between Russia and Ukraine, although the continued failure of these talks has built in some headline scepticism around the subject. Nevertheless, the current environment suggests a trend toward de-risking.

Free Dashboards

Free Onyx Insights

Oil insights with Harry Tchilinguirian | Russian Roulette

Free Onyx Officials

No reports found

The Officials with Jorge Montepeque: Gong Xi Fa Cai! Long

Upcoming events

EIA STEO

in 2d

FOMC Meeting

in 2d

Fujairah Inventories

in 3d

Fujairah Inventories

in 3d

API Stats Release

in 3d

Dec25 ICE Gasoil Expiry

in 4d

Latest News

{kind=link}

{kind=link}

{kind=link}

Most Popular

European Window: Brent Eases to $63.60/bbl

3d ago

The Feb’26 Brent futures contract failed to maintain strength above the $64.00/bbl handle this afternoon, easing from $64.08/bbl at 15:30 GMT to $63.60/bbl at 16:30 GMT (time of writing). In the news, local Russian emergency centres have reported a fire at Russia's Azov Sea port of Temryuk, due to a Ukrainian drone attack. The fire occurred at the Maktren-Nafta LPG transhipment terminal, which handles LPG exports from Russian and Kazakh producers. According to Reuters, between January and October 2025, the terminal handled roughly 220kt of LPG. Elsewhere, according to The Officials sources, Kuwait’s Al Zour refinery will be in maintenance ...

COT Deep Dive – Sing 0.5% Crack

3d ago

In this edition, we take a look at the Jan'26 Sing 0.5% crack.

Trader Meeting Notes: Volatility, Where Art Thou?

4d ago

M1 Brent futures fell into yet another lull, with the 50-day moving average still acting like a brick wall for more than two months now. On the products side, CTA net positioning in ICE gasoil and CME heating oil has flipped to net short, based on Flux Insight's CTA model, while positioning in RBOB, Brent, and WTI futures has just been consolidating in the negatives all week. Risk appetite has been eroding into year-end, with open interest in ICE gasoil futures declining for a third consecutive week. On top of that, we seem to be stuck at an impasse on ...

European Window: Brent Rises to $63.50/bbl

4d ago

The Feb’26 Brent futures contract rose this afternoon, from $62.57/bbl at 14:40 GMT to $63.50/bbl at 16:50 GMT. In the news, the Trump administration has approved transactions with Lukoil gas stations outside Russia, issuing a narrow waiver to the sanctions imposed by the US in October. According to a US Treasury Department post, these transactions are authorised until 26 April 2026. Elsewhere, Reuters reported that oil exports from Russia’s Novorossiysk and the CPC terminal were roughly 1mt behind schedule in November, due to storms and recent drone attacks that disrupted loading operations. Scheduled loadings of Urals, Siberian Light, and KEBCO ...

COT Report: Winter Hibernation

5d ago

See all the updates across the barrel in this week’s Onyx Commitment of Traders report, as well as six contracts to watch. Click on the relevant button below to access your COT report.

European Window: Brent Falls to $62.68/bbl

5d ago

The Feb’26 Brent futures contract initially rose from $62.77/bbl at 14:10 GMT to $63.29/bbl at 16:00 GMT, before falling to $62.68/bbl at 17:00 GMT (time of writing). In the news, Reuters has reported that remote-controlled Ukrainian explosives have struck the Druzhba oil pipeline in Russia's central Tambov region. This is the fifth Ukrainian attack on the pipeline this year, which supplies Russian oil to Hungary and Slovakia; oil supplies are reportedly running through the Druzhba as usual. Meanwhile, Hungarian Foreign Minister Peter Szijjarto has said that the country will challenge a European Union decision to phase out Russian energy sources ...

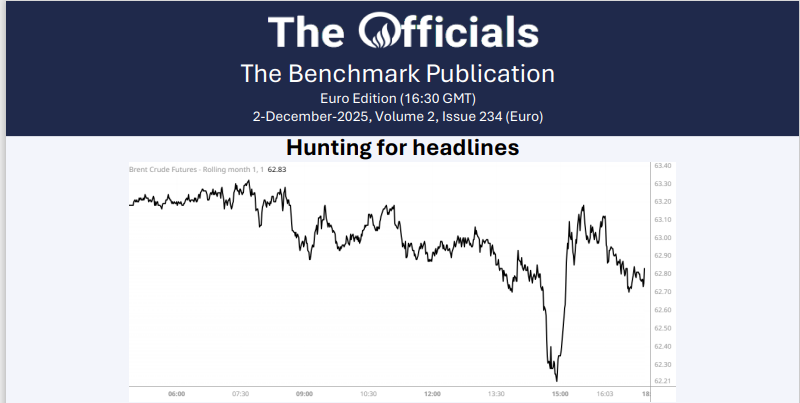

European Window: Brent Recovers to $62.83/bbl

6d ago

The Feb’26 Brent futures contract failed to maintain strength above $63/bbl this afternoon, declining from $63.06/bbl at 13:00 GMT to $62.21/bbl at 14:55 GMT. Prices then recovered to $62.83/bbl at 16:30 GMT (time of writing). In the news, Besiktas Shipping, a Turkish owner of an oil tanker that was damaged near Senegal's coast last week after four external explosions, announced that it is suspending all shipping operations related to Russian interests. Citing safety concerns, the company said it would halt operations with Russia immediately. Elsewhere, the Caspian Pipeline Consortium (CPC) aims to complete all repairs on its SPM-3 at its ...

Events

Dec 9, 2025

17:00 UTC+0

EIA STEO

in 2d

19:00 UTC+0:00

FOMC Meeting

in 2d

Dec 10, 2025

08:00 UTC+0:00

Fujairah Inventories

in 3d

Fujairah Inventories

in 3d

21:30 UTC+0:00

API Stats Release

in 3d

Dec 11, 2025

12:00 UTC+0:00

Dec25 ICE Gasoil Expiry

in 4d

13:00 UTC+0:00

OPEC OMR

in 4d

OPEC OMR

in 4d

15:15 UTC+0:00

ARA Product Inventories

in 4d

ARA Product Inventories

in 4d

Dec 17, 2025

08:00 UTC+0:00

Fujairah Inventories

in 10d

Fujairah Inventories

in 10d

21:30 UTC+0:00

API Stats Release

in 10d

Dec 18, 2025

15:15 UTC+0:00

ARA Product Inventories

in 11d

Dec 19, 2025

19:30 UTC+0:00

Jan26 WTI Expiry

in 12d

Dec 24, 2025

08:00 UTC+0:00

Fujairah Inventories

in 17d