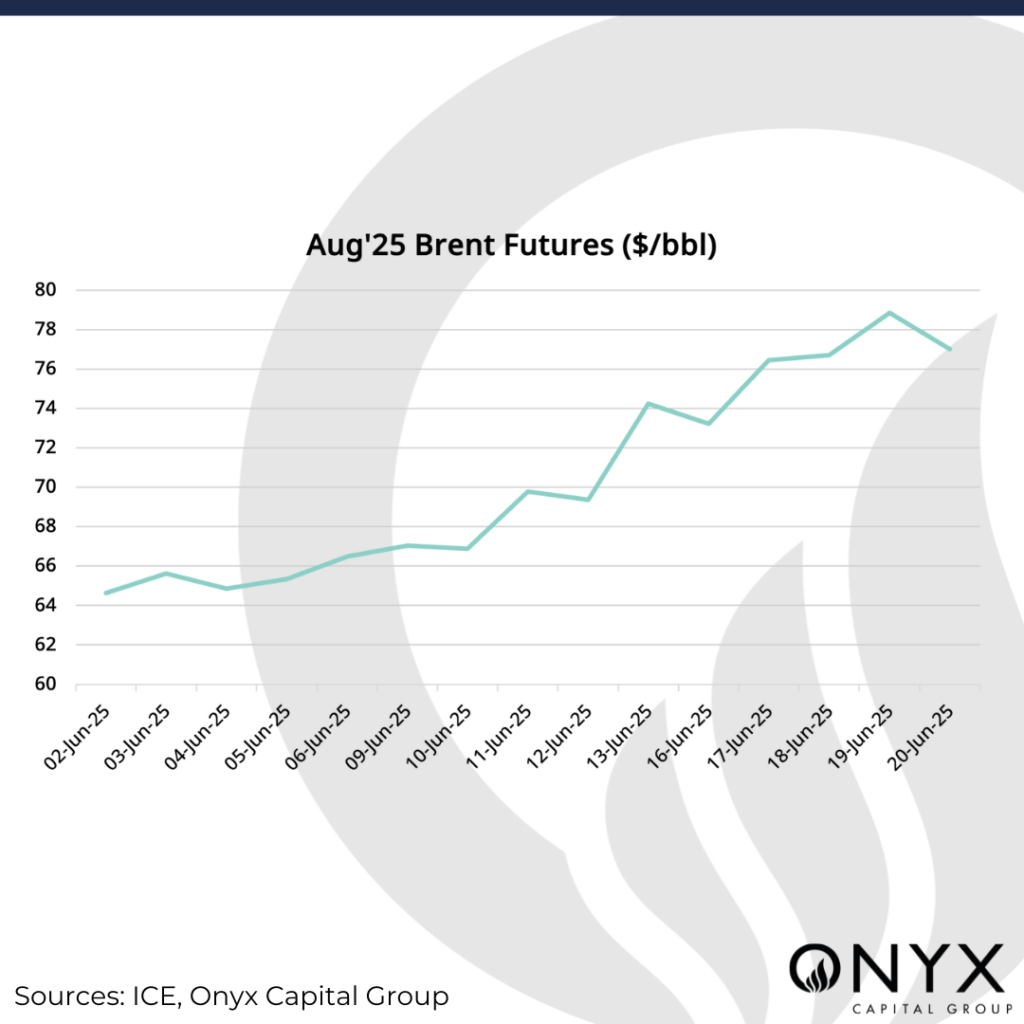

Brent crude futures rose by 11% over the past week, reaching 5-month highs as the Iran-Israel conflict worsened, with the market pricing in a higher geopolitical risk premium. In the latest escalation, strikes from the US on Iranian nuclear sites over the weekend mark the first time that the US has directly attacked Iranian territory, adding another layer of volatility and risk premiums. The market’s primary focus is the Iran-Israel war and subsequent concerns of supply disruptions. We anticipate Aug’25 Brent crude prices to remain in the high 70s by the end of the week, between $75-80/bbl. We highlight the following factors in this week’s forecast:

- Potential Iranian Retaliation

- Strait of Hormuz

- Speculative Positioning

The market is bracing for Iran’s potential retaliation, which will likely dictate the next course of action for oil prices. Direct US involvement has raised the risk of a stronger response by Tehran through targeting regional energy infrastructure, shipping in the Strait of Hormuz, and US assets in the region. Any retaliation could invite further reaction by the belligerents, risking further US involvement in the conflict and a higher risk premium. Gulf States quickly condemned the US strikes, urging all sides to de-escalate and return to diplomacy. Many of these oil-rich countries host major US assets and bases and fear any potential spillover of the war. It is possible, but unlikely, that Iran agrees to resume negotiations and restrict its nuclear program. The Iranian government is walking a careful tightrope between domestic pressure and geopolitical realities, seeking an outcome that preserves stability while deterring further attacks. Nonetheless, we believe the continuation of hostile rhetoric between both sides and the raised possibility of deeper US involvement will likely keep oil prices elevated in the near term.

The Strait of Hormuz, through which a quarter of the world’s seaborne oil trade passes, has been in the spotlight. The Houthis in Yemen have vowed to support Iran following the US strikes. While oil flows through the Straits of Hormuz and Bab-el-Mandeb remain uninterrupted, freight and vessel rates are surging as heightened risks prompt some shipowners to temporarily halt vessel offerings. According to banks, including JP Morgan and Goldman Sachs, even a partial disruption to the Straits could send crude prices above $100/bbl. Crucially, Iran’s Kharg Terminal remains operational and untouched, even as Israel has already hit several Iranian oil and gas facilities. It was reported that Iran’s parliament has approved a plan to close the Strait, but the final decision lies with the Supreme National Security Council. The closure of the Strait does not refer to a physical closure, but rather targeted efforts from Iran or the Houthis on Western vessels to discourage flows, leading to prohibitively high insurance costs, and impairing transit flows. Given recent escalations, the expanded scope of Iranian retaliation has increased the tail risk of a potential blockade of the Strait of Hormuz, however unlikely that scenario may still be.

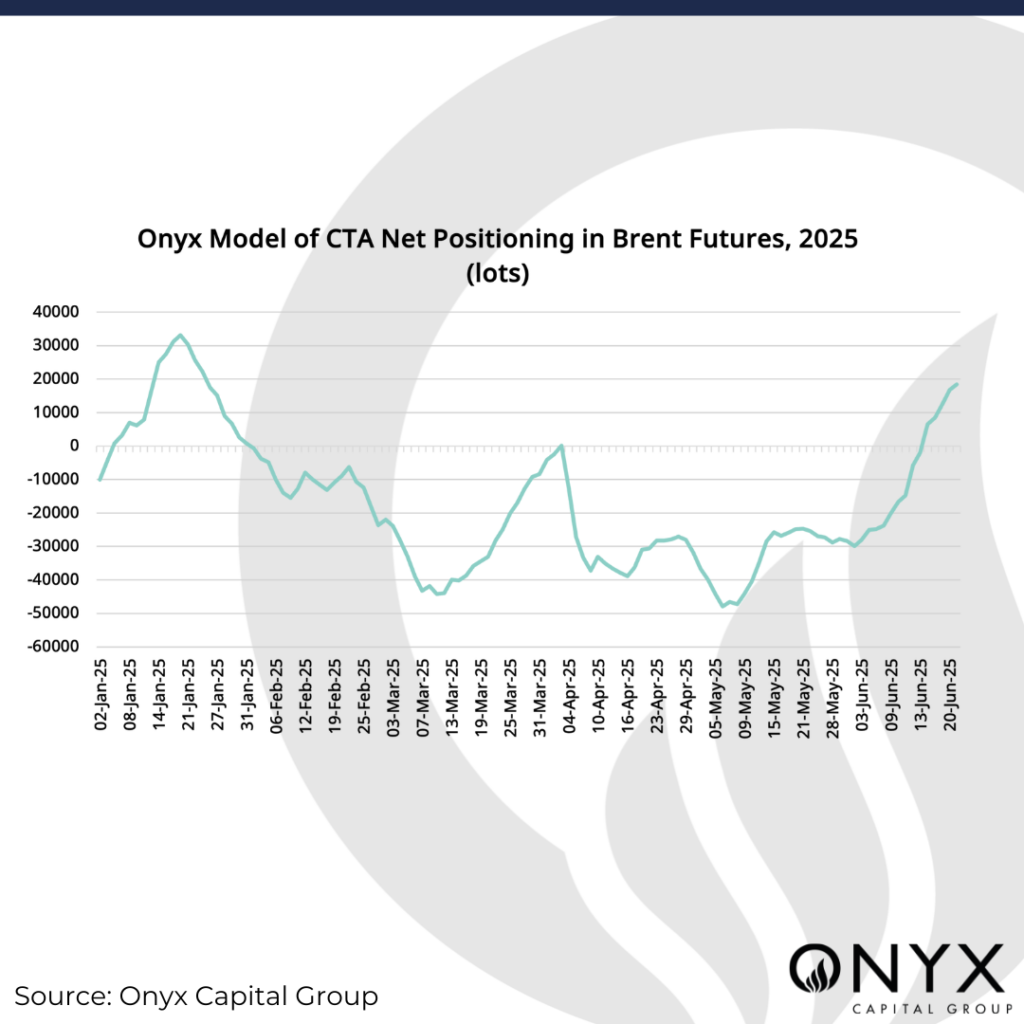

Market positioning remains an important factor in assessing the magnitude of future price moves. In response to Israel’s surprise attack on Iran on 13 June, money managers continue to boost their net length in Brent futures. ICE COT data for the week ending 17 June indicates a sixth consecutive week of increases in bullish positions. Overall speculative positioning remains historically bearish (32nd percentile for all weeks since 2013), leaving room for additional short covering should further bullish catalysts emerge. Meanwhile, in line with price action, CTA positioning in oil futures benchmarks has surged, with net length in Brent futures at its highest since January 2025. Saturated long positions may indicate a contrarian CTA sell-side signal and cap further gains. This suggests that any additional upside from geopolitical risk may come from non-CTA participants.